Stock Analysis

Why Did Ionis (IONS) Stock Crash 24%? The Eplontersen ATTR-CM Trial Failure Explained

IONS plunged about 24% on July 9 after the Phase 3 CARDIO-TTRansform trial of eplontersen (Wainua) missed its ATTR-CM endpoint — splitting the field as stabilizer rival BridgeBio jumped 16%.

Summary

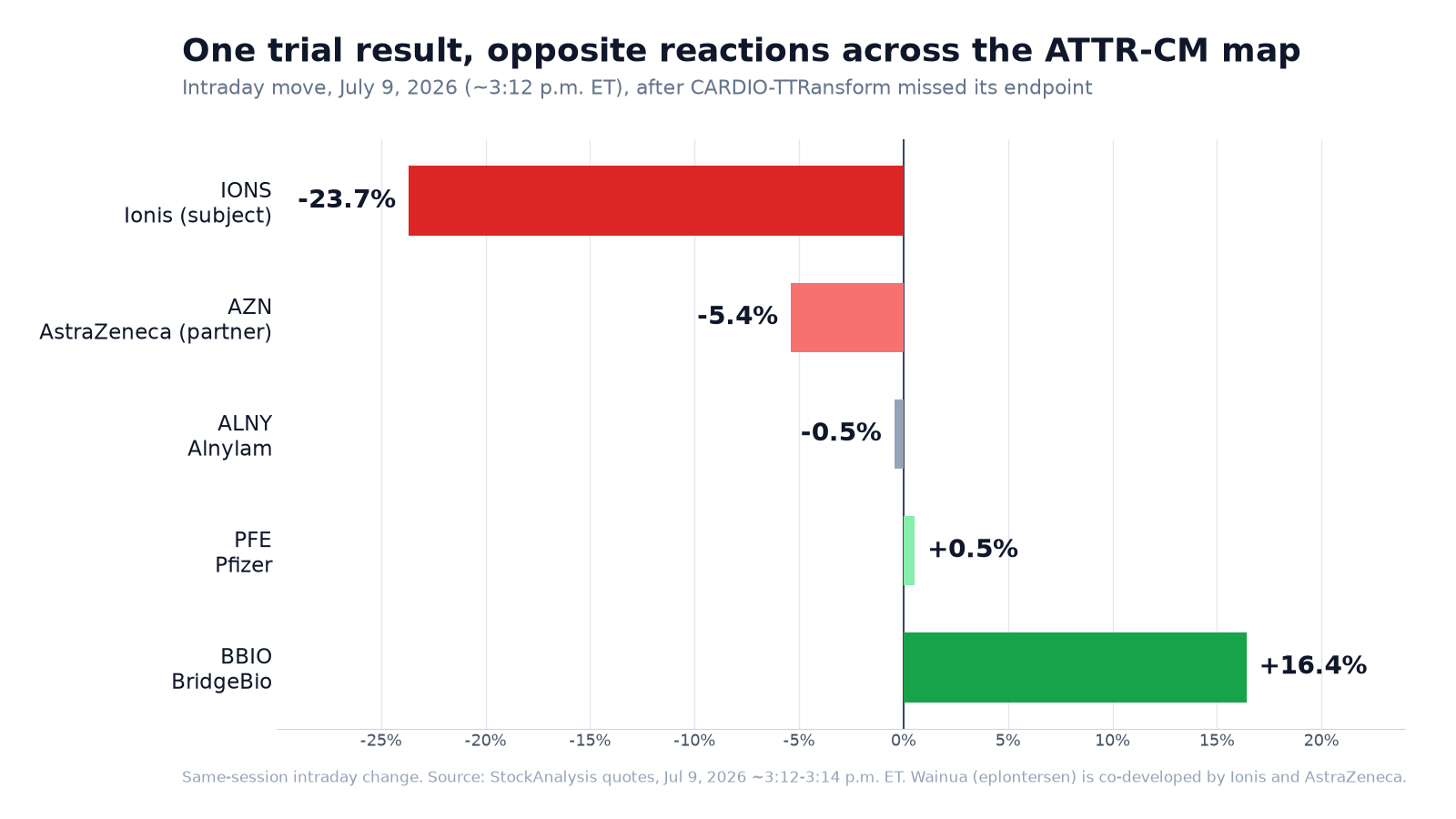

Ionis Pharmaceuticals (NASDAQ: IONS) plunged about 24% on Thursday, July 9, 2026, trading near $64.45 against Wednesday's $84.46 close — a roughly $20 drop that put it on pace for its largest single-day fall in more than five years and made it the biggest decliner on BestStocks' change feed for the session [1][2]. The catalyst was unambiguous and binary: before the open, Ionis and partner AstraZeneca said the Phase 3 CARDIO-TTRansform trial of eplontersen (marketed as Wainua) failed to meet its primary endpoint in transthyretin-mediated amyloid cardiomyopathy (ATTR-CM) [4][5]. The move came on extreme volume — several times the stock's daily average — supporting the view that this was a meaningful repricing rather than routine noise [1][3]. But the most revealing part was how the rest of the field reacted: the read-through favored the drugs already approved for ATTR-CM. TTR-stabilizer play BridgeBio (BBIO) jumped about 16% and incumbent stabilizer Pfizer (PFE) ticked up, while Alnylam (ALNY) — the one rival silencer, already carrying its own positive cardiomyopathy data — had a more volatile, mixed session and ended the afternoon roughly flat [7].

What changed

Everything hinged on one dataset. CARDIO-TTRansform enrolled about 1,432 patients across 130 sites in 20 countries — the largest ATTR-CM trial run to date — and followed them for up to 140 weeks [4][8]. Its primary endpoint was a composite of cardiovascular mortality and recurrent cardiovascular clinical events through Week 140; adding Wainua to standard of care did not deliver a statistically significant benefit versus placebo [4][5]. That is the headline that erased a quarter of Ionis's market value and knocked partner AstraZeneca's U.S.-listed shares down about 5% — its London-listed stock fell more sharply earlier in the session, and the smaller percentage reflects ATTR-CM being one program inside a far larger company [7].

The detail underneath is more nuanced than the headline, and it explains the split-screen reaction. A prespecified subgroup showed a nominally significant benefit for eplontersen used as monotherapy — but in patients already on a TTR stabilizer at baseline, no treatment effect was observed [5][6]. In other words, the drug did what it is designed to do biologically — it produced large, sustained reductions in transthyretin, and several secondary, imaging, and biomarker measures favored it — yet on top of a modern standard of care dominated by stabilizers, it could not clear the bar on hard clinical outcomes [4][5]. Analysts, including Jefferies, pointed to a structural reason: background stabilizer therapy was heavy in both arms — a majority of patients were already on a TTR stabilizer such as tafamidis at baseline, and more started one during the study — which lifted the placebo group's outcomes and left little room for a silencer added on top to show incremental benefit [5]. Ionis and AstraZeneca will present the full dataset at the European Society of Cardiology Congress in August 2026 [4][9].

That treatment-map split is why competitors rallied while Ionis fell. ATTR-CM care today centers on TTR stabilizers — Pfizer's tafamidis and BridgeBio's acoramidis (Attruby) — that hold the protein together, plus one approved RNA-based silencer, Alnylam's vutrisiran (Amvuttra), that cuts its production. Wainua itself is approved only for hereditary ATTR polyneuropathy (ATTRv-PN); CARDIO-TTRansform was its bid to expand into cardiomyopathy, and this readout did not secure it. A trial showing that a silencer adds little on top of a stabilizer is, by direct implication, bullish for the stabilizer franchises: BridgeBio, the purest listed acoramidis play, rose about 16%, and Pfizer edged higher [7]. Alnylam's reaction was murkier — it is also a silencer, but its vutrisiran already has its own positive cardiomyopathy data, and after an early swing it ended the afternoon roughly flat [7].

Why it matters

ATTR-CM is one of the most valuable and contested markets in cardiology, and CARDIO-TTRansform was supposed to be the trial that pushed silencers into the front line alongside — or ahead of — stabilizers. Instead, it sharpened the mechanism debate in the stabilizers' favor, at least for patients already on one. That is why a single company's trial reset the valuations of an entire therapeutic category in a morning: it is read as evidence about where the standard of care is heading, not just about one drug [5][7]. For BridgeBio and Pfizer, it reinforces the durability of the stabilizer franchises; for Alnylam, it leaves its already-approved vutrisiran positioning intact.

It also matters as a reminder of how binary large-cap biotech can be. A low-beta, profitable-trajectory name like Ionis can shed $3 billion of market value between two closes on a single endpoint miss, because so much of the growth case was concentrated in one late-stage readout [2]. The nuance in the data — a real biological effect undercut by trial design and an evolving standard of care — is exactly the kind of complexity that markets price first and parse later, which is why the full ESC presentation and the analyst resets that follow will matter more than Thursday's tape.

What to watch

First, the full CARDIO-TTRansform dataset at the ESC Congress in August 2026 — specifically the monotherapy subgroup, the influence of heavy background stabilizer use, and any biomarker or imaging signals that could support a narrower label or a follow-on study [4][5]. Second, analyst actions: with the pre-failure consensus now obsolete, watch where firms reset targets and whether any frame the monotherapy signal as salvageable [1]. Third, second-quarter earnings — unconfirmed, with third-party estimates ranging from late July to early August 2026 — where management will have to re-baseline the ATTR-CM opportunity and reaffirm the path to breakeven [1]. Finally, watch the competitive tape: whether BridgeBio and Pfizer hold their gains and whether Alnylam's steadiness persists will show if the market treats the stabilizer read-through as durable or as a one-day reflex [7].

Why did IONS stock drop on July 9, 2026?

Ionis (IONS) fell about 24%, from an $84.46 prior close to roughly $64.45, after it and partner AstraZeneca announced that the Phase 3 CARDIO-TTRansform trial of eplontersen (Wainua) failed to meet its primary endpoint in transthyretin amyloid cardiomyopathy (ATTR-CM) [1][4]. Adding the drug to standard of care did not significantly reduce cardiovascular mortality and recurrent cardiovascular clinical events through Week 140 versus placebo. The move came on extreme volume — several times average — and it dragged AstraZeneca's U.S.-listed shares down about 5% while lifting stabilizer competitors [2][7].

Did the eplontersen trial fail completely?

Not entirely. The overall trial missed its primary cardiovascular-outcomes endpoint, but a prespecified subgroup showed a nominally significant benefit for eplontersen used as monotherapy; the shortfall was concentrated in patients already on a TTR stabilizer [5][6]. The drug still produced large, sustained reductions in transthyretin, and some secondary and imaging measures favored it. Analysts including Jefferies noted that heavy background stabilizer use in both arms — most patients were already on tafamidis or started it during the study — lifted the placebo group's outcomes and narrowed the gap [5].

The July 9 move in numbers

| Measure | Value | Note |

|---|---|---|

| IONS prior close, Wed Jul 8 | $84.46 | Pre-announcement close [1][2] |

| IONS intraday, Thu Jul 9 (StockAnalysis) | $64.45 | -23.69%, -$20.01; ~3:12 p.m. ET [2] |

| IONS intraday, Thu Jul 9 (site feed) | $64.55 | -23.57%; catalyst detected 9:33 a.m. ET [1] |

| Day's range | $64.10 – $70.35 | StockAnalysis, ~3:12 p.m. ET Jul 9 [2] |

| Volume vs. average | ~16.3M by ~3:12 p.m. ET vs. 2.9M 20-day avg | ~5.7x so far; feed pegs ~8.8x full day [2][3] |

| 52-week range | $40.03 – $86.74 | StockAnalysis [2] |

| Market capitalization | ~$10.65 billion | Jul 9, 2026 [2] |

| 5-year beta / short interest | ~0.37 / ~10.8% of float | Low beta; heavily shorted [3] |

| Consensus price target | ~$101–$103 (now stale) | Pre-failure; being cut post-readout [1] |

How did ATTR-CM peers move on the news?

| Stock | Jul 9 intraday move | Role in ATTR-CM |

|---|---|---|

| IONS — Ionis | -23.7% | Eplontersen (silencer) developer [2] |

| AZN — AstraZeneca | -5.4% | Co-developer / commercial partner [7] |

| ALNY — Alnylam | -0.5% | Vutrisiran (approved silencer); volatile, ~flat by mid-afternoon [7] |

| PFE — Pfizer | +0.5% | Tafamidis (incumbent stabilizer) [7] |

| BBIO — BridgeBio | +16.4% | Acoramidis (stabilizer) — biggest winner [7] |

What is CARDIO-TTRansform and ATTR-CM?

ATTR-CM (transthyretin-mediated amyloid cardiomyopathy) is a progressive heart disease caused by misfolded transthyretin protein depositing in the heart. CARDIO-TTRansform was a Phase 3 trial of about 1,432 patients across 130 sites in 20 countries testing whether eplontersen (Wainua) — an antisense drug that silences transthyretin production — could reduce cardiovascular mortality and recurrent cardiovascular clinical events on top of standard care through Week 140 [4][8]. It missed that primary endpoint, though a monotherapy subgroup showed benefit [5].

Is IONS stock a buy after the drop?

This piece does not make recommendations, but the setup has two sides. The bear case is that the market's read-through — BridgeBio up 16% — signals stabilizers keep the standard of care and Wainua's cardiomyopathy expansion is impaired, making the old ~$101–$103 consensus obsolete [1][7]. The bull case rests on the monotherapy subgroup, the clean transthyretin knockdown, heavy background stabilizer use that may have masked benefit, and Ionis's broader base — Spinraza royalties, Wainua's polyneuropathy approval, and a 2028 breakeven target [5][6]. High short interest and vocal retail interest make near-term moves volatile in both directions [3][10].

What could move IONS next?

The full CARDIO-TTRansform dataset at the ESC Congress in August 2026 is the key event, followed by analyst target resets and second-quarter earnings (unconfirmed; third-party estimates range from late July to early August 2026) [1][4]. Watch whether management can re-baseline the ATTR-CM opportunity and reaffirm the path to breakeven, and whether stabilizer peers hold their gains [6][7].

Ionis Pharmaceuticals (IONS) stock FAQ

Why did Ionis (IONS) stock crash on July 9, 2026?

IONS fell about 24%, from an $84.46 prior close to roughly $64.45, after Ionis and partner AstraZeneca announced that the Phase 3 CARDIO-TTRansform trial of eplontersen (Wainua) failed its primary endpoint in ATTR-CM. Adding the drug to standard of care did not significantly reduce cardiovascular mortality and recurrent cardiovascular clinical events through Week 140 versus placebo. The move came on extreme volume — several times its average.

Did the eplontersen (Wainua) trial fail completely?

No. The overall trial missed its primary cardiovascular-outcomes endpoint, but a prespecified subgroup showed a nominally significant benefit for eplontersen as monotherapy; the shortfall was concentrated in patients already on a TTR stabilizer. The drug still produced large reductions in transthyretin, and analysts including Jefferies noted that heavy background stabilizer use in both arms lifted the placebo group's outcomes and narrowed the gap.

Why did BridgeBio and Pfizer stock rise on the news?

The failure implies that adding a TTR silencer on top of a stabilizer adds little for already-stabilized ATTR-CM patients, which is bullish for stabilizer franchises. BridgeBio (acoramidis) jumped about 16% and Pfizer (tafamidis) edged higher. Alnylam, whose vutrisiran already has positive cardiomyopathy data, was roughly flat.

How much of Ionis's value was wiped out?

Ionis shed roughly a quarter of its market value — about $3 billion — between the July 8 close and July 9 intraday, on pace for its largest single-day drop in more than five years, on volume running several times its average. AstraZeneca's U.S.-listed shares fell about 5% — its London-listed stock fell more sharply earlier — a smaller percentage because ATTR-CM is one program within a much larger company.

What is ATTR-CM and how is it treated?

ATTR-CM (transthyretin amyloid cardiomyopathy) is a progressive heart disease caused by misfolded transthyretin protein depositing in the heart. It is treated mainly with TTR stabilizers (Pfizer's tafamidis, BridgeBio's acoramidis) and the approved RNA-based silencer Alnylam's vutrisiran, which reduces transthyretin production. Ionis/AstraZeneca's eplontersen (Wainua) is approved for hereditary ATTR polyneuropathy and was seeking to expand into ATTR-CM through CARDIO-TTRansform.

What is the analyst price target for IONS now?

Pre-failure, consensus targets clustered near $101–$103, but that figure is now stale and is already being cut as post-failure downgrades flow through. Watch for reset targets after the failure and the full data presentation at the ESC Congress in August 2026.

When does Ionis report earnings next?

Second-quarter earnings are not yet confirmed; third-party estimates range from late July to early August 2026. Before that, Ionis and AstraZeneca plan to present the full CARDIO-TTRansform dataset at the European Society of Cardiology Congress in August 2026, which will be the key event for the stock.