Stock Analysis

STRL Stock: Sterling Infrastructure's AI Data Center Backlog Is Driving 2026 Growth

Sterling Infrastructure grew Q1 2026 revenue 92% on data center demand, with a visible work pool near $6.5 billion and guidance for ~51% growth this year.

Summary

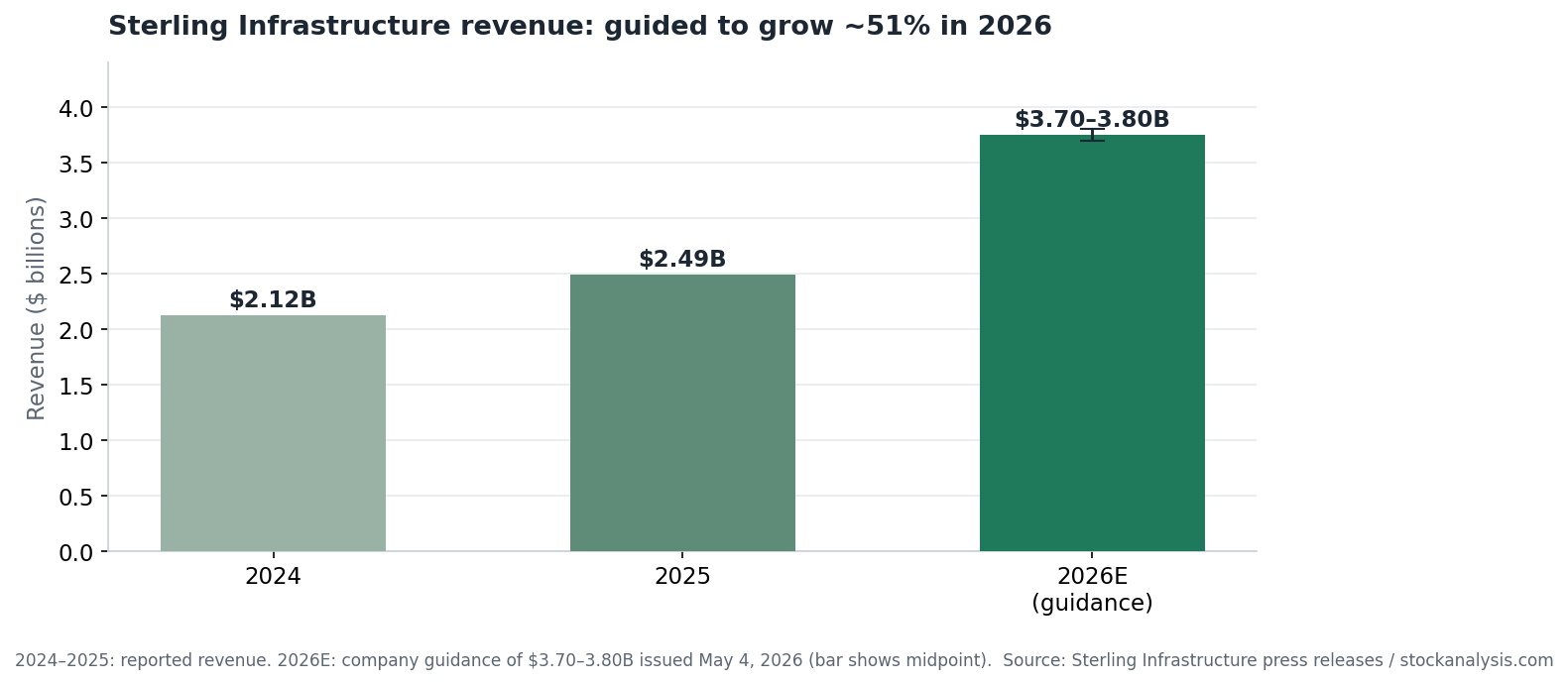

Sterling Infrastructure (NASDAQ: STRL) doesn't train models or sell chips. It moves dirt, pours concrete and, since late 2025, wires the buildings for the companies that do. The Texas-based contractor reported first-quarter 2026 revenue of $825.7 million, up 92% from a year earlier, and adjusted diluted EPS of $3.59, up 120% [1]. Management raised full-year guidance to $3.70–3.80 billion in revenue, about 51% growth at the midpoint, with adjusted EPS of $18.40 to $19.05 [1][2].

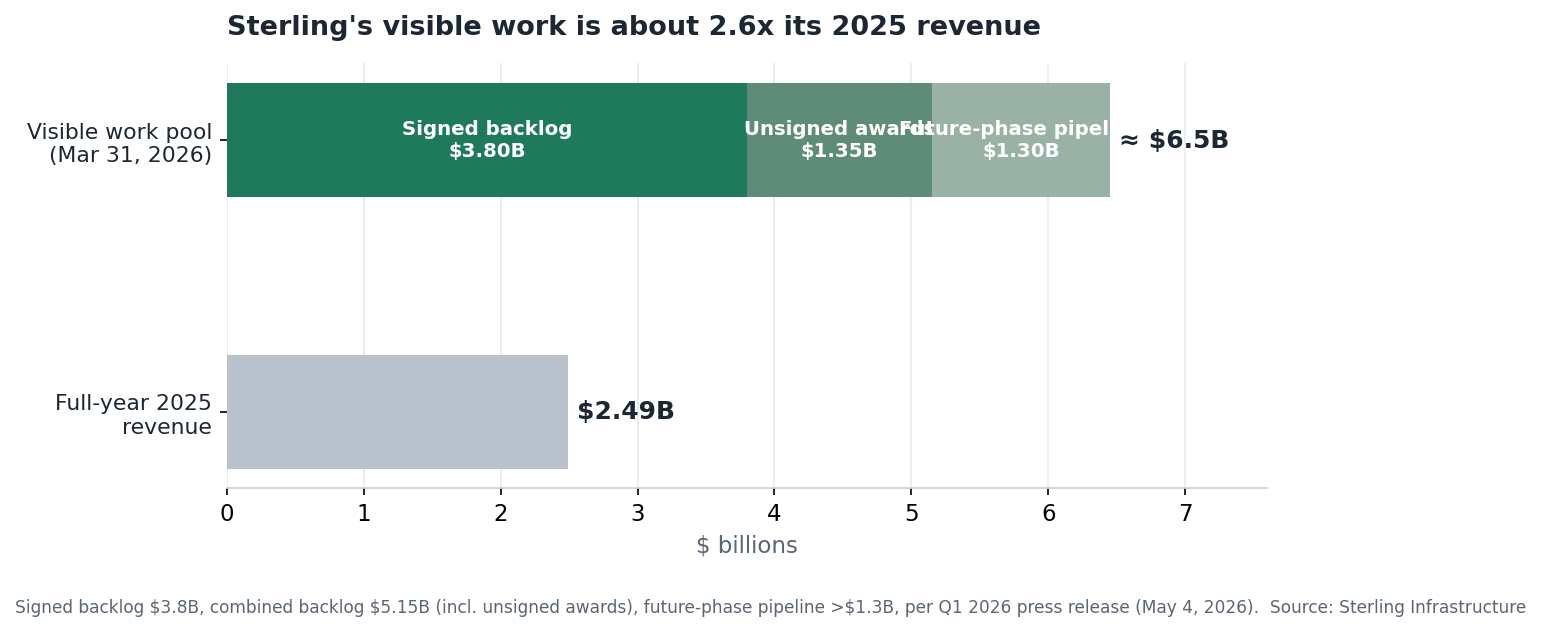

Behind those numbers sits a pool of visible work approaching $6.5 billion: signed backlog, unsigned awards and high-probability future phases of projects already underway [1]. Sterling's entire 2025 revenue was $2.49 billion [3]. That ratio, more than anything else, is why the stock keeps showing up in AI infrastructure screens.

What changed

The E-Infrastructure Solutions segment, which handles site development and electrical work for data centers, semiconductor plants and large manufacturing sites, has become the whole story. Segment revenue grew 174% in the first quarter, including organic growth above 100%, with data centers again the primary driver [1][4]. That was an acceleration, not a blip: the same segment grew 58% in the third quarter of 2025 [5].

The backlog moved even faster than revenue. Signed backlog reached $3.8 billion at March 31, up 78% from a year earlier. Combined backlog, which adds unsigned awards, hit $5.15 billion, up 131%, and high-probability future-phase work exceeds another $1.3 billion [1]. Book-to-burn ratios were 2.1x on signed backlog and 3.5x on combined backlog, meaning new work arrived at more than twice the pace Sterling executed it [1].

M&A shaped the quarter as much as organic wins. CEC Facilities Group, the electrical contractor Sterling bought in the third quarter of 2025 [5], contributed $156.1 million of revenue and has grown its own combined backlog by $1.2 billion since year-end after several large Texas project wins [1][4]. In June, Sterling added Stone Ridge Contracting, an Idaho site-development firm that extends the segment into the Pacific Northwest [3]. The company also won the first phase of a multiphase semiconductor fabrication campus, a joint-venture job worth more than $500 million that runs into late 2027 or early 2028, on a campus expected to be built out over decades [4].

Why it matters

Sterling is one of the cleaner picks-and-shovels expressions of AI capital spending on the market. It carries no model risk and no chip-cycle exposure; its asset is a book of signed contracts. The CEC deal changes the economics of each of those contracts, because Sterling can now sell site work and electrical work on the same project. Management expects that combination to add 300 to 500 basis points of margin over time and to compress project timelines, which is exactly what hyperscalers pay premiums for [4].

The risks concentrate in the same place as the growth. E-Infrastructure is now the engine, and it depends on the spending plans of a handful of very large customers; a pause or reprioritization at one of them would shorten Sterling's vaunted visibility quickly [6]. The stock has rerated as well. Shares trade far above their historical earnings multiples, and the Street's Strong Buy consensus with an average target near $941 rests on the same capex assumptions the whole story depends on [3]. Investors are no longer paying construction-company prices for this construction company.

What to watch

Second-quarter earnings arrive August 10, 2026 [2]. Between now and then, quarterly capex guidance from the largest data center builders is the real tell; those budgets lead future site-development awards. Inside Sterling's own reports and SEC filings, watch book-to-burn (a slide below 1x would be the first crack in the story), the pace of CEC margin integration, and follow-on phases of the semiconductor campus [4]. Management has also flagged capacity constraints in electricians and project managers as an execution risk [2]. Building Solutions remains the soft spot while residential demand stays weak [5]; it's small enough not to break the story, but it shows what this portfolio looks like without a boom behind it.

Is Sterling Infrastructure an AI stock?

Not in the usual sense: Sterling is a construction contractor, not a technology company, but its largest segment builds the sites and electrical systems that AI data centers run on, so its results now rise and fall with AI capital spending. E-Infrastructure Solutions grew revenue 174% in the first quarter of 2026, with data centers the primary driver, alongside semiconductor and large manufacturing work [1][4]. That makes STRL an AI infrastructure beneficiary rather than an AI company; it gets paid per project, in contracts, whatever any individual model or chip does.

Why did STRL stock jump after Q1 2026 earnings?

- Shares rose nearly 38% in the session after the May 5 report [3].

- First-quarter revenue of $825.7 million came in far above the roughly $592 million consensus [3].

- Full-year 2026 guidance was raised about 20% at the midpoint, to $3.70–3.80 billion in revenue and $18.40–19.05 in adjusted EPS [2].

- Analysts chased the print: Stifel lifted its target to $884 from $490, KeyBanc went to $922, and Oppenheimer initiated coverage at $950 [3].

Sterling's Q1 2026 by the numbers

| Metric | Q1 2026 | Change vs. Q1 2025 |

|---|---|---|

| Revenue | $825.7M | +92% |

| Net income | $96.0M | +143% |

| Adjusted diluted EPS | $3.59 | +120% |

| Adjusted EBITDA | $166.6M | +107% |

| E-Infrastructure revenue growth | +174% | — |

| Signed backlog (Mar 31) | $3.80B | +78% |

| Combined backlog (Mar 31) | $5.15B | +131% |

| Operating cash flow | $165.6M | — |

All comparisons are to the prior-year quarter as reported by the company on May 4, 2026 [1]. Backlog figures are point-in-time balances at March 31, 2026 versus March 31, 2025.

What could move STRL stock next?

- August 10, 2026 — second-quarter results, the next test of the raised guidance [2].

- July–August 2026 — hyperscaler capital-expenditure updates during earnings season, the leading indicator for site-development awards.

- Awards on later phases of the multiphase semiconductor campus, whose first $500 million-plus phase runs into late 2027 [4].

- Progress on the 300–500 basis points of margin expansion management expects from combining CEC's electrical work with site development [4].

- Further tuck-in acquisitions after Stone Ridge extended the segment into the Pacific Northwest in June [3].

Sterling Infrastructure stock FAQ

What does Sterling Infrastructure (STRL) do?

Sterling Infrastructure is a U.S. contractor with three segments: E-Infrastructure Solutions (site development and electrical work for data centers, semiconductor plants, manufacturing and distribution centers), Transportation Solutions (highways, bridges, airports and rail), and Building Solutions (residential and commercial concrete foundations). It is headquartered in The Woodlands, Texas.

Who is Sterling Infrastructure's CEO?

Joe Cutillo is Sterling Infrastructure's chief executive officer. Under his leadership the company shifted away from low-bid highway work toward large, higher-margin mission-critical projects such as data centers.

How big is Sterling Infrastructure's backlog in 2026?

At March 31, 2026, signed backlog was $3.8 billion (up 78% year over year) and combined backlog, which adds unsigned awards, was $5.15 billion (up 131%). Including more than $1.3 billion of high-probability future-phase work, the company's total visible pool of work approaches $6.5 billion.

What is Sterling Infrastructure's revenue guidance for 2026?

The company guides to 2026 revenue of $3.70-3.80 billion, roughly 51% growth at the midpoint, with adjusted diluted EPS of $18.40-$19.05, as raised on May 4, 2026.

Is Sterling Infrastructure profitable?

Yes. In the first quarter of 2026 Sterling reported net income of $96.0 million ($3.09 per diluted share) and generated $165.6 million of operating cash flow, ending the quarter in a net cash position.