Stock Analysis

Why did AST SpaceMobile (ASTS) stock drop ~15% on July 16, 2026? The $1B convertible, and the capped call behind it

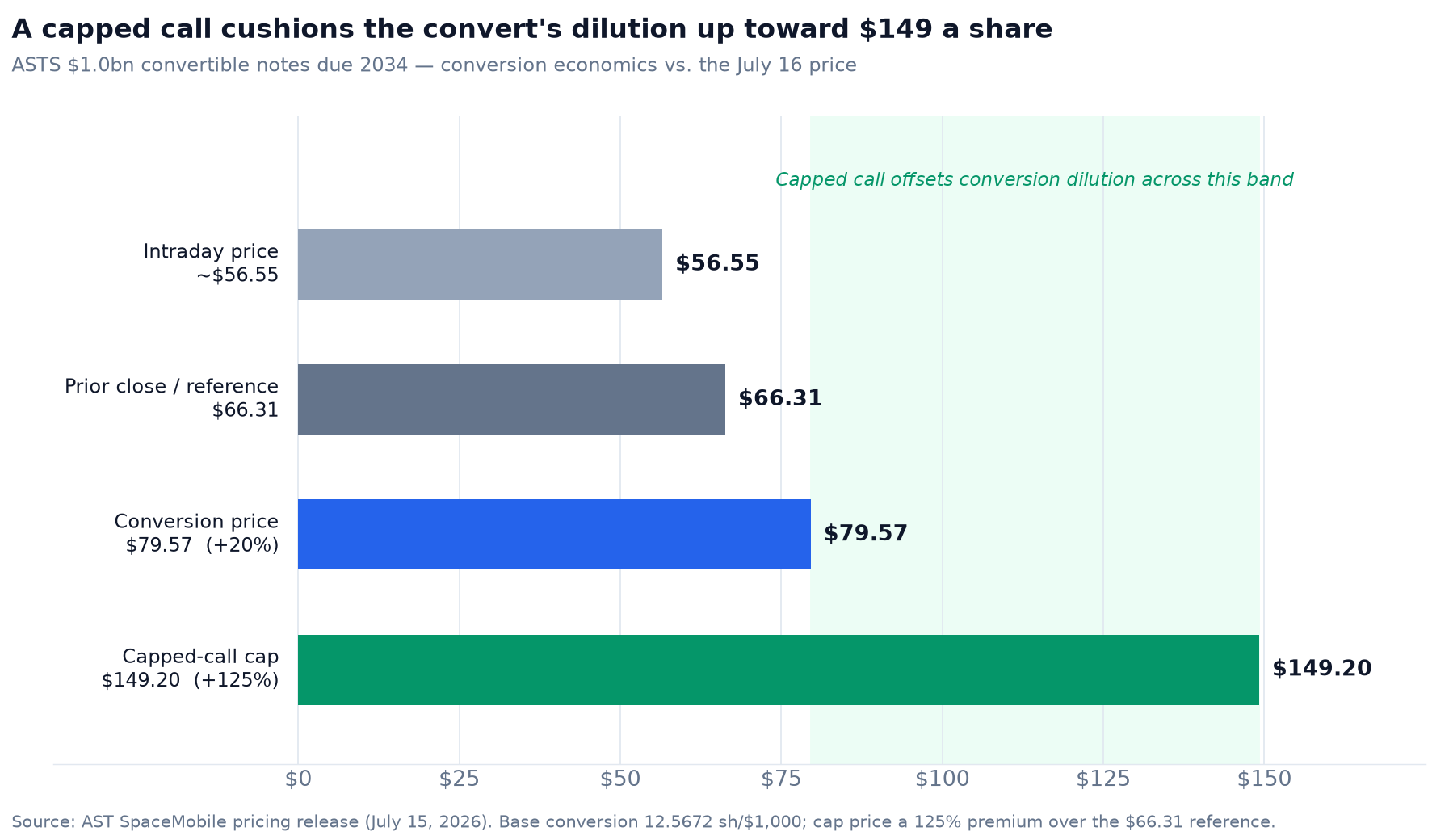

AST SpaceMobile dropped about 14.7% intraday after pricing a $1.0 billion convertible notes offering. The 'dilution' headline skips the capped call that offsets conversion dilution up to a $149.20 cap. The more likely drivers were convertible-arb hedging, the signal of another raise, and a space-sector sell-off.

Summary

AST SpaceMobile (NASDAQ: ASTS) was trading around $56.55 late Thursday morning, July 16, 2026, down about $9.76, or 14.72%, from Wednesday's $66.31 close, with the session still open [1][2]. The trigger is not in doubt: the company announced the deal Wednesday and, after the close, priced a $1.0 billion offering of convertible senior notes due 2034; the stock gapped down overnight and extended the fall into Thursday [4][6][7].

The one-word explanation making the rounds is "dilution" [15]. That word is doing too much work. The notes convert at $79.57, and they were sold with a capped call whose cap price is $149.20 — a 125% premium over the reference — designed to offset the dilution from conversion up to that level [4]. What is more likely pressing on the tape are drivers the headline understates: mechanical convertible-arbitrage hedging into a stock already 24% short on its float, the signal of a company raising a further $1 billion on top of $2.7 billion of cash, and a broad space-sector sell-off the same day. The exact split between these cannot be proven, but each is documented.

| Evidence level | What can be said |

|---|---|

| Documented | ASTS priced $1.0bn of convertible notes after Wednesday's close; the stock opened sharply lower Thursday [4][7]. |

| Mechanically plausible | Convertible buyers may have short-sold ASTS to hedge; a heavily-shorted, launch-exposed name sold off alongside its space peers. |

| Not measurable from public data | How much of the ~15% fall came from arb hedging, the financing signal, sector weakness or ordinary selling — the split cannot be quantified. |

The sequence — why the move landed today

- Wed, Jul 15 (morning): ASTS announces its intent to offer $1.0bn of convertible senior notes [6].

- Wed, Jul 15 (close): shares close at $66.31 — the figure the deal uses as its reference price [2][4].

- Wed, Jul 15 (after hours): the notes price — 1.625% coupon, $79.57 conversion, a $149.20 capped-call cap [4].

- Thu, Jul 16: the stock gaps down and trades ~15% lower, near $56.55 by late morning [2].

What changed

| Metric | Value | As of / source |

|---|---|---|

| Intraday price | ~$56.55 | Jul 16 2026, ~11:02 a.m. ET — StockAnalysis [2] |

| Prior close (Jul 15) | $66.31 | Also the offering's reference price [2][4] |

| Intraday change | −$9.76 / −14.72% | Vs prior close; session ongoing [2] |

| Intraday range | $56.13 – $61.50 (open $59.20) | Jul 16 2026 — StockAnalysis [2] |

| 52-week range | $36.08 – $133.86 | StockAnalysis [2] |

| Volume by ~11:02 a.m. | 22.7M sh | Already above the full 20-day average of ~18.97M [2][3] |

| Short interest | 64.72M sh | 16.67% of shares out; 24.33% of float [3] |

| Market cap | ~$21.7–21.9bn | Shares out 388.1M (+51.4% y/y) [3] |

Two things stand out before the story even begins. First, volume: by late morning ASTS had already traded more shares than it averages in a full session, so participation and turnover were unusually high — though heavy volume measures activity, not conviction, and can equally reflect forced sales, dealer hedging or arbitrage [2][3]. Second, positioning: short interest running near a quarter of the float means a large short base was already in place — which matters for how a convertible lands.

The deal, and the dilution that is not there yet

The terms are specific. ASTS priced $1.0 billion of 1.625% convertible senior notes due February 1, 2034, with a 13-day option for initial purchasers to add $150 million [4]. The base conversion price is $79.57, a 20% premium over Wednesday's $66.31 close (a conversion rate of 12.5672 shares per $1,000 note). Net proceeds are about $983.6 million, and the company spent $96.9 million of that buying capped call transactions whose cap price is $149.20, a 125% premium, structured to offset the dilution from conversion up to that level [4].

That structure matters. At the conversion price the notes represent roughly 12.6 million shares, about 3.2% of the 388 million outstanding, and only if converted in the money — and the capped call is designed to offset that dilution up to the $149.20 cap, subject to how ASTS elects to settle conversions in cash, shares or a combination [3][4]. So the reflexive "they just diluted me 15%" reading does not describe what happened on paper. The dilution the tape fears is an out-of-the-money conversion feature, heavily hedged — not a share issuance at today's price. This is the same instrument that hit Fermi (FRMI) a week earlier [14] — but the market's reaction to a convertible is rarely about the arithmetic of conversion.

| Proceeds & dilution bridge | Base offering | With $150M option |

|---|---|---|

| Principal | $1.000bn | $1.150bn |

| Gross shares initially underlying | 12.57M | 14.45M |

| — as % of 388.12M outstanding | 3.24% | 3.72% |

| Net proceeds | ~$983.6M | ~$1,131.2M |

| Initial capped-call cost | −$96.9M | −$96.9M+ |

| Net proceeds after capped call | ~$886.7M | n/a (extra cost not yet set) |

The share figures are the notes' gross initially underlying shares — the maximum before any capped-call offset and only on conversion — not realised dilution. Source: AST SpaceMobile pricing release [4]; share count from StockAnalysis [3].

What is actually pressuring the stock

Three forces, in rough order of immediacy. First, convertible arbitrage. The institutional buyers of a convertible typically hedge it by short-selling the underlying stock to neutralise the equity delta; that hedging flow arrives precisely at issuance and is mechanical, not a view on the company. Landing on a name where short interest is already 24.33% of the float [3], the marginal supply meets an already-crowded, high-beta name — which may help explain a move larger than the raw dilution math alone would justify.

Second, the signal. ASTS held $2.72 billion of cash and restricted cash at June 30 and is raising roughly another billion anyway [5]. Management is candid about why: the proceeds beyond the capped call fund "additional access to orbit" through partnerships and potential acquisitions to vertically integrate and reduce reliance on third-party launch providers [5][8]. That is a rational long-term move for a company whose BlueBird constellation — about 45 satellites — is now targeted for early 2027 [5], and which is in discussions on a Japanese low-Earth-orbit project with Rakuten whose expected total value runs up to about ¥148 billion (roughly $1 billion) — a figure that is the project's scale, not committed financing or ASTS's own proceeds, and one the filing says is not assured [5]. But a fresh raise before the commercial cellular-broadband service is generating material revenue reads, in the short term, as capital intensity and timeline risk, not confidence.

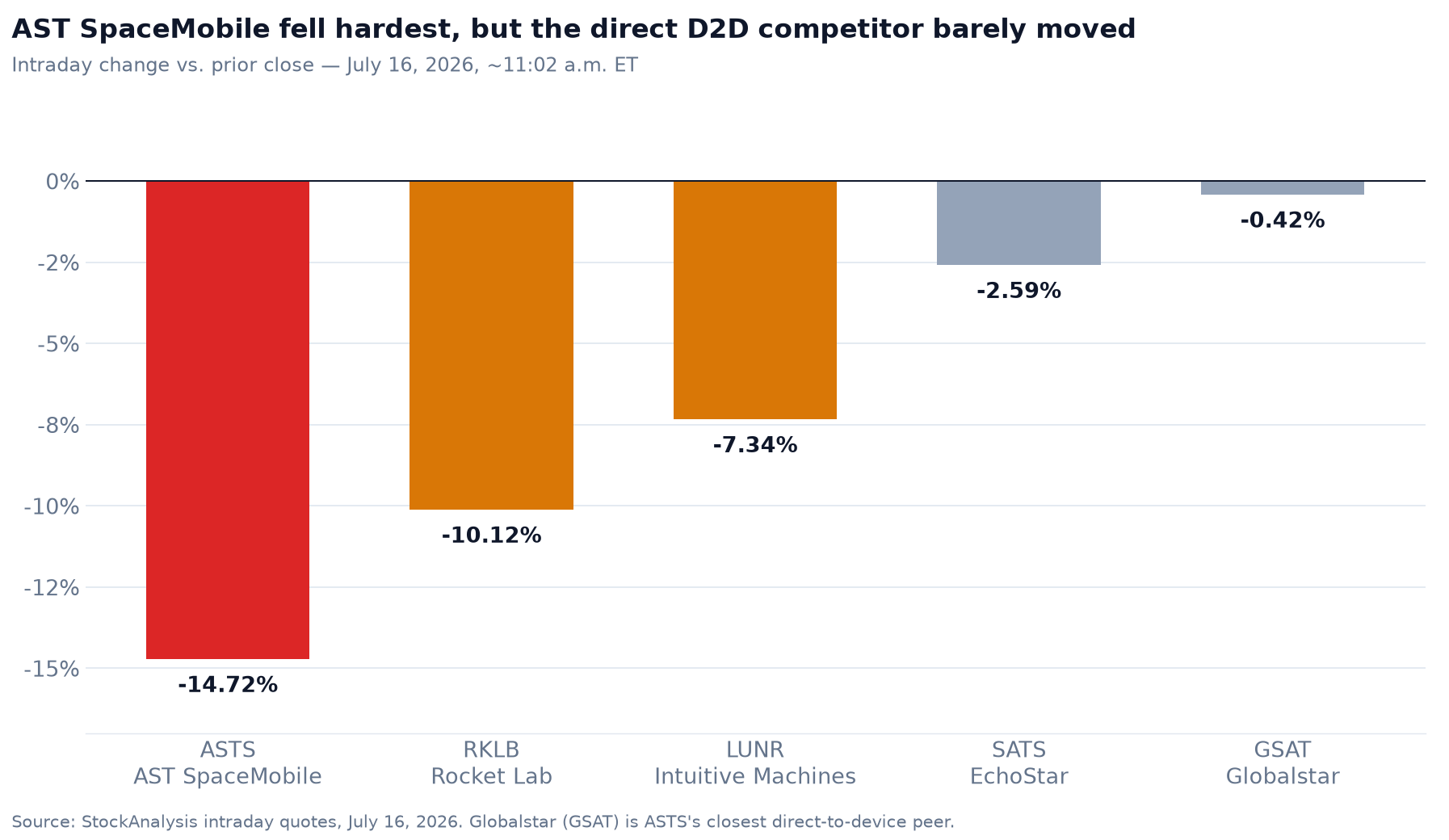

Third, the sector. This was not an ASTS-only day for space. Rocket Lab fell 10.12% and Intuitive Machines (LUNR) 7.34% in the same session on a broad risk-off tied to an oil-price spike [9][10]. The tell is the control case: Globalstar — ASTS's closest direct-to-device competitor — was essentially flat at −0.42%, and EchoStar fell only 2.59% [11][12]. The direct-to-device theme did not sell off; ASTS and the launch-dependent names did.

Analyst view

Read the move as three layers stacked, not one. A broad space sell-off took several points off every launch-exposed name; convertible-arb hedging into a heavily-shorted float took several more off ASTS specifically; and a sentiment reaction to "another billion raised before the service scales" did the rest. What the drop is not is a 15% economic dilution today — the notes convert at $79.57 and the capped call is designed to offset that dilution up to a $149.20 cap, both well above the current price. The scale of the reaction is itself the clue: at −$9.76 across 388.1 million shares, the day's move erased roughly $3.8 billion of equity value — nearly four times the $1.0 billion raised [2][3]. That does not prove an overreaction; it shows the market priced in far more than mechanical share-count dilution. The heavy volume shows unusually high participation, but turnover and information are different things: a mechanical hedging flow can move a stock hard without anyone forming a new view of the business.

The genuine question the raise surfaces is timeline, not solvency. With $2.7 billion already on hand plus ~$984 million net incoming, funding is not the risk; execution is — whether ~45 BlueBird satellites actually fly in early 2027, and whether the Rakuten JV and any launch-provider deal firm up. Those are the things the next few quarters answer; a convertible pricing does not.

What this means for value

ASTS is effectively pre-earnings — it books only nascent revenue, and none yet from the commercial SpaceMobile cellular-broadband service — so a P/E frame does not apply; the scenario prices below are the author's own, loosely anchored to analysts' published target distribution and to milestone outcomes, not to an earnings multiple. As of mid-July the consensus rating is Hold with an average target of $79.78 across 10 analysts (range $41.20 to $108) — a snapshot whose inputs include actions from May and June, not all of them post-deal. Piper Sandler initiated at Buy with a $100 target on July 15, the same calendar day as the raise, though there is no timestamp establishing the note followed the after-hours pricing [13]. The probabilities are the author's illustrative estimates, not forecasts, and sum to 100%.

| Scenario | Price | Probability | Key driver |

|---|---|---|---|

| Bull | ~$120 | 25% | BlueBird flies on the early-2027 schedule, the Rakuten JV finalises, the funding overhang clears; toward the Street high of $108 and the $149.20 cap where the convert itself becomes moot [13] |

| Base | ~$80 | 45% | Execution roughly on plan, dilution overhang lingers; near the $79.78 consensus target and the $79.57 base conversion price [4][13] |

| Bear | ~$45 | 30% | Launch slips again, cash burn and capital intensity dominate, convert-arb and heavy short interest keep a lid on it; toward the Street low of $41.20 [3][13] |

| Probability-weighted value ≈ $79.50 — the ~$56.55 intraday price sits about 29% below that blend (equivalently, the blend implies about 41% upside from the price). | |||

Under these illustrative assumptions — the author's own probabilities and outcomes, not the Street's, and note the bull case sits above the Street's $108 high — Thursday's intraday price sits below the blend. Read that as the market discounting execution risk more heavily than this middling scenario mix does. That gap is not a verdict. It is the price of genuine uncertainty about satellites that have not launched and a joint venture that is not signed; whether it is opportunity or warranted skepticism depends entirely on execution the market cannot yet see. Treat the ~$79.50 figure as the midpoint of a wide $45–$120 distribution driven by launch timing and funding perception, not a target.

What to watch

- Settlement and any greenshoe exercise (around July 20) — whether initial purchasers take the extra $150 million, and how the convertible-arb short flow unwinds once hedges are set [4].

- BlueBird launch cadence into early 2027 — the ~45-satellite campaign is the single biggest swing factor between the bull and bear cases [5].

- The Rakuten / J-LEO joint venture and any launch-provider acquisition — the "access to orbit" the raise is explicitly meant to fund; a signed deal would reframe the raise as offense, not defense [5].

- Short interest and the convert-arb unwind — a quarter of the float is short, but days-to-cover is a moderate ~3.4 (short interest ÷ the 20-day average volume, and a settlement-date snapshot), so this is amplification, not an obvious squeeze setup; watch whether the arb short established at issuance is later covered [3].

Frequently asked questions

Why did AST SpaceMobile (ASTS) stock fall on July 16, 2026?

After Wednesday's close, ASTS priced a $1.0 billion offering of convertible senior notes due 2034, and the stock gapped down, trading about 14.7% lower near $56.55 intraday on Thursday. The likely drivers were less about raw dilution than convertible-arbitrage short-hedging into a heavily-shorted float, the signal of raising a further $1 billion on top of $2.7 billion of cash, and a broad space-sector sell-off the same day — though the exact split between them cannot be proven.

Does the $1 billion convertible actually dilute ASTS shareholders by 15%?

No. The notes carry a conversion price of $79.57 — a 20% premium — representing roughly 12.6 million shares, about 3.2% of shares outstanding, and only if converted in the money. Crucially, ASTS also bought a capped call designed to offset the conversion premium above the notes' principal, up to a cap of $149.20 — reducing the dilution a conversion would otherwise cause — though the outcome depends on how ASTS settles conversions, in cash, shares or a combination.

What is a capped call and why does it matter here?

A capped call is a hedge a company buys alongside a convertible to offset the dilution from conversion, up to a cap price. ASTS spent $96.9 million of the proceeds to set that cap at $149.20, a 125% premium over the $66.31 reference. It is designed to offset dilution between the $79.57 conversion price and the $149.20 cap, subject to settlement method — which is why the reflexive 'they diluted me 15%' reading does not match the deal's structure.

Was the drop specific to ASTS or a whole-sector move?

Both. Space names sold off broadly on July 16 — Rocket Lab fell about 10% and Intuitive Machines about 7% on an oil-price-driven risk-off. But ASTS's closest direct-to-device competitor, Globalstar, was essentially flat (−0.42%), which is consistent with an ASTS-specific component — its capital raise and heavy short positioning — on top of the sector move, rather than a direct-to-device theme selling off.

What are analysts saying about ASTS?

The consensus rating is Hold with an average price target of $79.78 across 10 analysts, in a wide $41.20–$108 range — a snapshot whose inputs include actions from May and June, not all post-deal. Piper Sandler initiated at Buy with a $100 target on July 15, the same calendar day as the offering, though not necessarily after its pricing. Under the author's own illustrative scenarios (bull $120 / base $80 / bear $45), the ~$56.55 intraday price sat about 29% below a ~$79.50 blend. These figures are descriptive, not investment advice.