Stock Analysis

Why Did Fermi (FRMI) Stock Drop 15%? The $375M Convertible Notes Dilution Explained

FRMI fell about 15% on July 10 after pricing an upsized $375M convertible notes offering — dilution the market saw coming, on a pre-revenue AI-power developer already fighting over control and down 83% from its high.

Summary

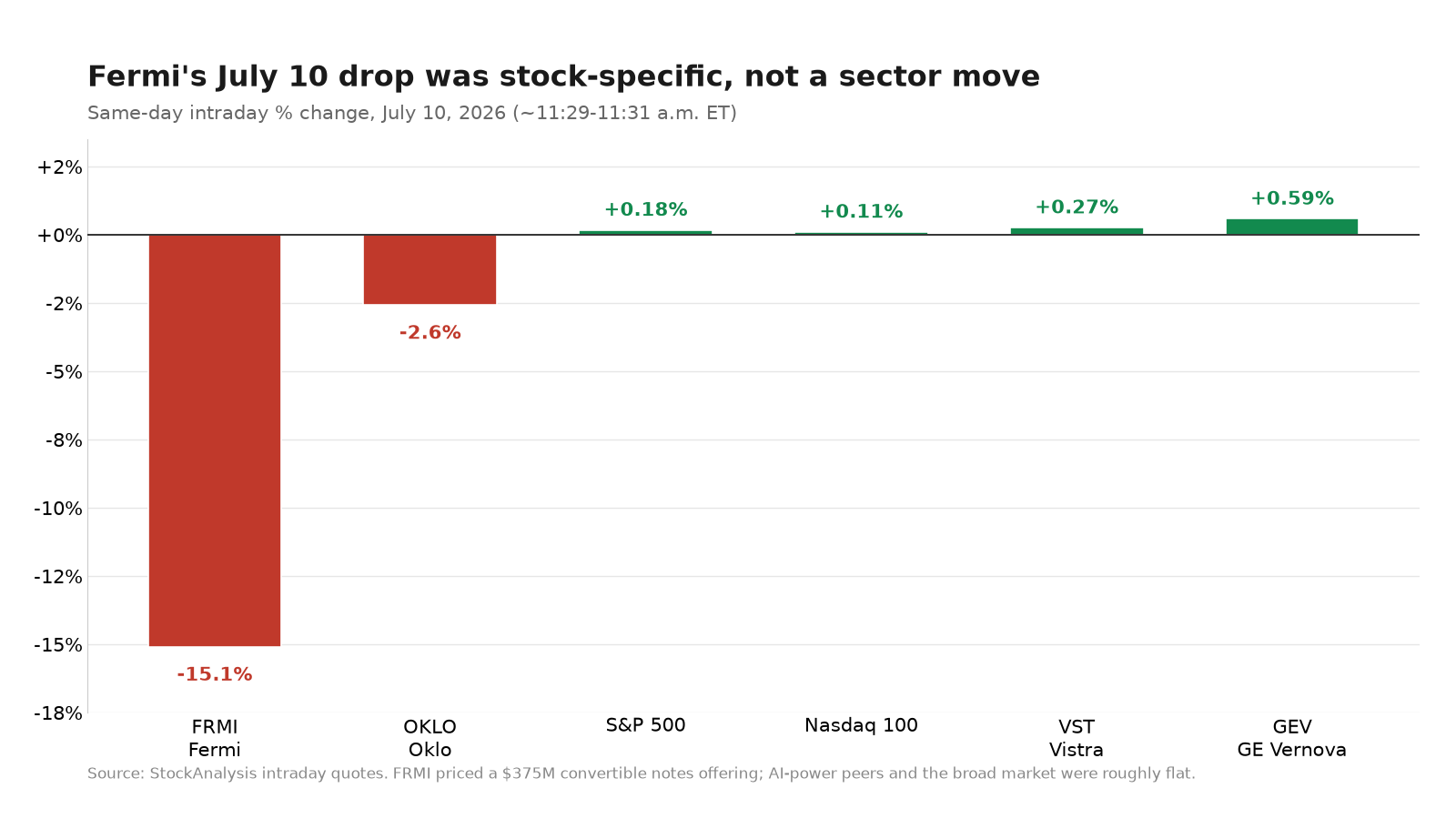

Fermi Inc. (NASDAQ: FRMI) fell about 15% on Friday, July 10, 2026, trading near $6.22 against Thursday's $7.32 close and touching an intraday low of $5.88 — the biggest decline on BestStocks' change feed for the session [1][2]. The trigger was a financing, not an operating miss: after Thursday's close the Amarillo-based AI-power developer launched — and, late that night, priced — an upsized $375 million offering of 5.00% convertible senior notes due 2031, with an option for another $56.25 million [4][5]. Convertibles are dilution the market can see coming, and this one lands on a pre-revenue balance sheet that has already burned through investor patience — the stock is down roughly 83% from its post-IPO high of $36.99 [2]. The move stood out as stock-specific — the clearest new catalyst was the note pricing, and AI-power peers barely budged on the day, with Oklo (OKLO) off 2.6%, Vistra (VST) up 0.3%, and GE Vernova (GEV) up 0.6% while the S&P 500 sat about 0.2% higher [8][9].

What changed

The mechanics of the deal are what spooked equity holders. The notes carry a 5.00% coupon and mature in 2031, with an initial conversion rate of 105.0862 shares per $1,000 — a conversion price of about $9.52, a 30% premium to Thursday's $7.32 close [4][6]. Fermi expects net proceeds near $362.25 million, or about $416.81 million if the purchasers' option is exercised in full, earmarked for general corporate purposes as it builds out its behind-the-meter power campus [4]. To blunt the dilution, the company bought capped call transactions that lift the effective conversion price to $14.64 — double Thursday's close — using roughly $30 million to $34.5 million of the proceeds [6]. They are designed to reduce — not eliminate — dilution up to that $14.64 cap, and Fermi can settle conversions in cash, shares, or a combination. In practice, a company issuing $375 million of convertible debt when its equity is already down more than 80% reads to the market as a company that needs cash and is willing to take on leverage and future share issuance to get it.

What turned an ordinary convertible into a 15% down day was the fine print filed alongside it. Fermi's preliminary offering memorandum, dated July 9, disclosed that the company is in "preliminary discussions with seven potential tenants and twelve potential joint venture partners," and warned plainly that such deals "may result in the issuance of capital stock of the Company in material amounts, which would be dilutive to stockholders" [7]. It also confirmed the company is "in advanced discussions with a potential candidate for our Chief Executive Officer" and laid out an unresolved control fight: Fermi terminated founder and former CEO Toby Neugebauer for cause on April 30, and on July 2 Neugebauer amended a lawsuit to add board member and former Energy Secretary Governor Rick Perry as a defendant, seeking to invalidate a bylaw amendment that requires a 70% supermajority to reshape the board [7]. So the convertible arrived stapled to fresh disclosure of more potential dilution, a leadership vacuum, and litigation over who controls the company.

The backdrop makes the reaction easier to read. Fermi is a pre-revenue developer building "Project Matador," a behind-the-meter campus in Amarillo, Texas that aims to stitch together natural gas, new nuclear, solar, storage, and grid power to feed hyperscale AI, targeting up to 1.5 gigawatts of power by 2027 and 2 GW by 2028, scaling to as much as 17 GW at full build-out (roughly 11 GW of gas and 6 GW of nuclear) [15]. It is a capital-intensive, milestone-driven story with no revenue yet, a first-quarter 2026 net loss of about $189 million (much of it non-cash stock compensation) [14], and a cash balance that had fallen to about $92 million by June 30 — including $29.2 million of restricted cash — from roughly $207 million three months earlier [15]. That profile leaves the equity acutely sensitive to anything that adds shares or debt, which is exactly what a convertible does.

Why it matters

Fermi is a clean case study in how the market finances speculative AI-infrastructure buildouts. The AI-power trade has been one of the strongest of the past two years, and names with real assets and cash flow — Vistra, Constellation, GE Vernova — have been rewarded. Fermi is the other end of that spectrum: a developer selling a vision of gigawatts that mostly do not exist yet, funding the gap with dilutive paper. Friday's move is the market marking the difference between owning power and promising it [8]. When a pre-revenue issuer taps the convert market, the read-through is rarely sector-wide; it is a statement about that specific balance sheet, which is why peers did not follow FRMI down.

It also matters as a governance story. The offering memorandum did not just price a bond — it confirmed, in the company's own words, that Fermi is fighting its founder in court, running without a permanent CEO, and openly contemplating further equity issuance to close tenant and joint-venture deals [7]. Each of those is a discount factor on its own. Stacked together and disclosed on the same morning that the company asked the market for $375 million, they explain why a routine financing became one of the day's worst single-stock moves.

What to watch

First, the CEO appointment: the memo says a candidate is in advanced discussions, and a credible, permanent leader would remove one of the largest overhangs [7]. Second, the Neugebauer litigation — any ruling on the 70% supermajority bylaw could decide who controls the board and reset the equity story in either direction [7]. Third, tenant and joint-venture signings: a marquee hyperscaler lease would validate the campus and, ideally, come without a large equity issuance; a deal that leans on new shares would confirm the dilution the memo warned about [7]. Fourth, the option on the notes — whether initial purchasers exercise the extra $56.25 million tranche will show how much appetite there was for the paper [4]. Finally, the next earnings report — aggregators estimate August 13, 2026, though Fermi has not confirmed the date — where management will have to show progress toward its 2027 first-power targets and update the roughly $92 million cash position the convertible just supplemented [1][15].

Why did FRMI stock drop on July 10, 2026?

Fermi (FRMI) fell about 15%, from a $7.32 prior close to roughly $6.22, after it priced an upsized $375 million offering of 5.00% convertible senior notes due 2031, with an option for another $56.25 million [2][4]. Convertible debt implies future share issuance, and the deal landed on a pre-revenue company already down more than 80% from its post-IPO high. The accompanying offering memorandum also disclosed potential further equity dilution from pending tenant and joint-venture talks, an unfilled CEO seat, and active litigation with founder Toby Neugebauer — magnifying the sell-off [7].

Does the convertible notes deal dilute Fermi shareholders?

Potentially, but not immediately. The notes convert at about $9.52 per share (a 30% premium to the $7.32 close), and Fermi bought capped call transactions that raise the effective conversion price to $14.64, meaning no economic dilution accrues unless the stock roughly doubles [4][6]. The bigger dilution worry is separate: the offering memorandum warned that pending tenant and joint-venture deals "may result in the issuance of capital stock of the Company in material amounts" [7].

The July 10 move in numbers

| Measure | Value | Note |

|---|---|---|

| FRMI prior close, Thu Jul 9 | $7.32 | Pre-pricing reference close [2] |

| FRMI intraday, Fri Jul 10 (StockAnalysis) | $6.22 | -15.10%, -$1.11; ~11:29 a.m. ET [2] |

| Day's range | $5.88 – $6.42 | StockAnalysis, ~11:29 a.m. ET Jul 10 [2] |

| Volume vs. average | ~38.6M by ~11:29 a.m. ET vs. 19.6M 20-day avg | ~2.0x a full day's average, before noon [2][3] |

| 52-week range | $4.47 – $36.99 | ~83% below the high [2] |

| Market capitalization | ~$3.96 billion | Jul 10, 2026 [2] |

| Shares out / short interest | 637.6M / 34.8M (~5.5% of shares out; ~10.8% of float) | StockAnalysis; float varies by provider [2][3] |

| Next earnings (est.) | Aug 13, 2026 | Aggregator estimate; not company-confirmed [1] |

What are the terms of Fermi's convertible notes?

| Term | Detail |

|---|---|

| Principal | $375M (upsized from $350M), plus $56.25M purchasers' option (up to ~$431.25M) [4][5] |

| Coupon / maturity | 5.00% senior, due 2031 [4] |

| Conversion | 105.0862 shares per $1,000 → ~$9.52 (30% premium to $7.32) [4][6] |

| Capped call | Lifts effective conversion price to $14.64 (100% premium); ~$30–34.5M of proceeds [6] |

| Net proceeds | ~$362.25M (~$416.81M if option exercised); general corporate purposes [4] |

How did AI-power peers move the same day?

| Stock / index | Jul 10 intraday move | Note |

|---|---|---|

| FRMI — Fermi | -15.1% | Priced $375M convertible notes [2] |

| OKLO — Oklo | -2.6% | SMR developer; modest slip [8] |

| VST — Vistra | +0.3% | Incumbent power generator [8] |

| GEV — GE Vernova | +0.6% | Grid & turbine supplier [8] |

| S&P 500 / Nasdaq 100 | +0.2% / +0.1% | Broad market roughly flat [9] |

FRMI valuation scenarios: bull, base, bear

The scenarios below are the author's hypothetical, illustrative estimates — not forecasts, analyst consensus, or investment advice. The probabilities are judgment calls, and each price range is anchored to the cited inputs: recent Street targets, the conversion and capped-call reference prices, and the 52-week range. They are meant to frame the risk, not to price it precisely.

| Scenario | Price | Prob. | Key drivers |

|---|---|---|---|

| Bull | ~$14–17 | 20% | Marquee hyperscaler lease signed without heavy dilution, governance fight resolved, on track toward the 2027 first-power target; aligns with Stifel's $17 and the $14.64 capped-call ceiling [11] |

| Base | ~$8–10 | 45% | Convertible buys runway, pre-revenue optionality intact, but dilution overhang and litigation cap the multiple; roughly the $9.52 conversion price / Cantor's $8 [12] |

| Bear | ~$4–5 | 35% | Further dilutive equity or preferred raises at depressed prices (as the memo flags), an adverse control ruling, or project/CEO-transition slippage; toward the $4.47 52-week low / UBS caution [7][13] |

Blending those gives a probability-weighted fair value near $8.5–$9, modestly above Friday's ~$6.22 — implying the convertible-day drop may have slightly overshot, while the wide, bimodal spread underlines how much rides on the governance and tenant outcomes rather than on the financing itself [2][10].

Is FRMI stock a buy after the drop?

This piece does not make recommendations. The bear case is straightforward: a pre-revenue developer with no permanent CEO, an active control fight, and an explicit warning of more dilution ahead just added leverage, and the freshest analyst targets ($6–$17) already sit near or below the stock [7][13]. The bull case is that the capped call limits real dilution, the convertible adds roughly $330 million of fresh liquidity toward first power, and the flattering ~$22 consensus and the campus's up-to-17 GW ambition leave upside if Fermi signs a real tenant [6][10][15]. High short interest and a shattered chart make near-term moves volatile in both directions [3].

What is Fermi (FRMI) and Project Matador?

Fermi Inc. is an Amarillo, Texas developer of behind-the-meter power for AI and advanced computing, co-founded by former Energy Secretary and Texas Governor Rick Perry. Its flagship "Project Matador" campus aims to combine natural gas, new nuclear, solar, battery storage, and grid power to serve hyperscalers facing interconnection delays, targeting up to 1.5 GW by 2027 and 2 GW by 2028, scaling to as much as 17 GW at full build-out [15]. The company intends to elect real estate investment trust (REIT) status, went public on October 1, 2025, and remains pre-revenue with a first-quarter 2026 net loss near $189 million [2][14].

Fermi (FRMI) stock FAQ

Why did Fermi (FRMI) stock drop on July 10, 2026?

FRMI fell about 15%, from a $7.32 prior close to roughly $6.22, after it priced an upsized $375 million offering of 5.00% convertible senior notes due 2031, with an option for another $56.25 million. Convertible debt signals future share issuance, and the deal landed on a pre-revenue AI-power developer already down more than 80% from its post-IPO high. The accompanying offering memorandum also disclosed potential further equity dilution, an unfilled CEO seat, and active litigation with founder Toby Neugebauer.

What are the terms of Fermi's convertible notes?

Fermi priced $375 million of 5.00% convertible senior notes due 2031 (upsized from $350 million), plus a $56.25 million purchasers' option. The initial conversion rate is 105.0862 shares per $1,000, an about $9.52 conversion price and a 30% premium to the $7.32 close. Capped call transactions raise the effective conversion price to $14.64. Net proceeds are expected near $362.25 million for general corporate purposes.

Does the deal dilute existing shareholders?

Not immediately. The notes convert at about $9.52, and the capped call pushes the effective conversion price to $14.64, so no economic dilution accrues unless the stock roughly doubles. The larger dilution concern is separate: the offering memorandum warned that pending tenant and joint-venture talks may result in issuing capital stock 'in material amounts,' which would dilute stockholders.

Was the drop specific to Fermi or sector-wide?

It was stock-specific. On the same session, AI-power peers barely moved — Oklo was down about 2.6%, Vistra up 0.3%, and GE Vernova up 0.6% — while the S&P 500 was up about 0.2%. That divergence shows the market was reacting to Fermi's financing and governance, not to the AI-power theme.

What is Fermi (FRMI) and Project Matador?

Fermi is an Amarillo, Texas developer of behind-the-meter power for AI computing, co-founded by former Energy Secretary Rick Perry. Its 'Project Matador' campus aims to combine natural gas, new nuclear, solar, storage, and grid power to serve hyperscalers, targeting up to 1.5 GW by 2027 and 2 GW by 2028, scaling to as much as 17 GW at full build-out. It went public on October 1, 2025 and remains pre-revenue, with a first-quarter 2026 net loss near $189 million and about $92 million of cash at June 30, 2026.

What is the analyst price target for FRMI?

MarketBeat shows a 'Moderate Buy' consensus with an average target near $22.44, but that blend is skewed by stale, pre-collapse initiations in the $27–$37 range. The freshest marks are far lower: Stifel cut to $17 from $29 in June, Cantor Fitzgerald sits at $8, and UBS moved to Neutral at $6 in May — a cluster near or below the current price.

When does Fermi report earnings next?

Aggregators estimate Fermi's next earnings around August 13, 2026, though the company has not confirmed the date. That report will be watched for progress toward its 2027 first-power targets and for an update on the roughly $92 million cash position that the convertible notes just supplemented.