Stock Analysis

Why did Intuitive Surgical (ISRG) stock plunge ~13% on July 17, 2026 — despite a Q2 earnings beat?

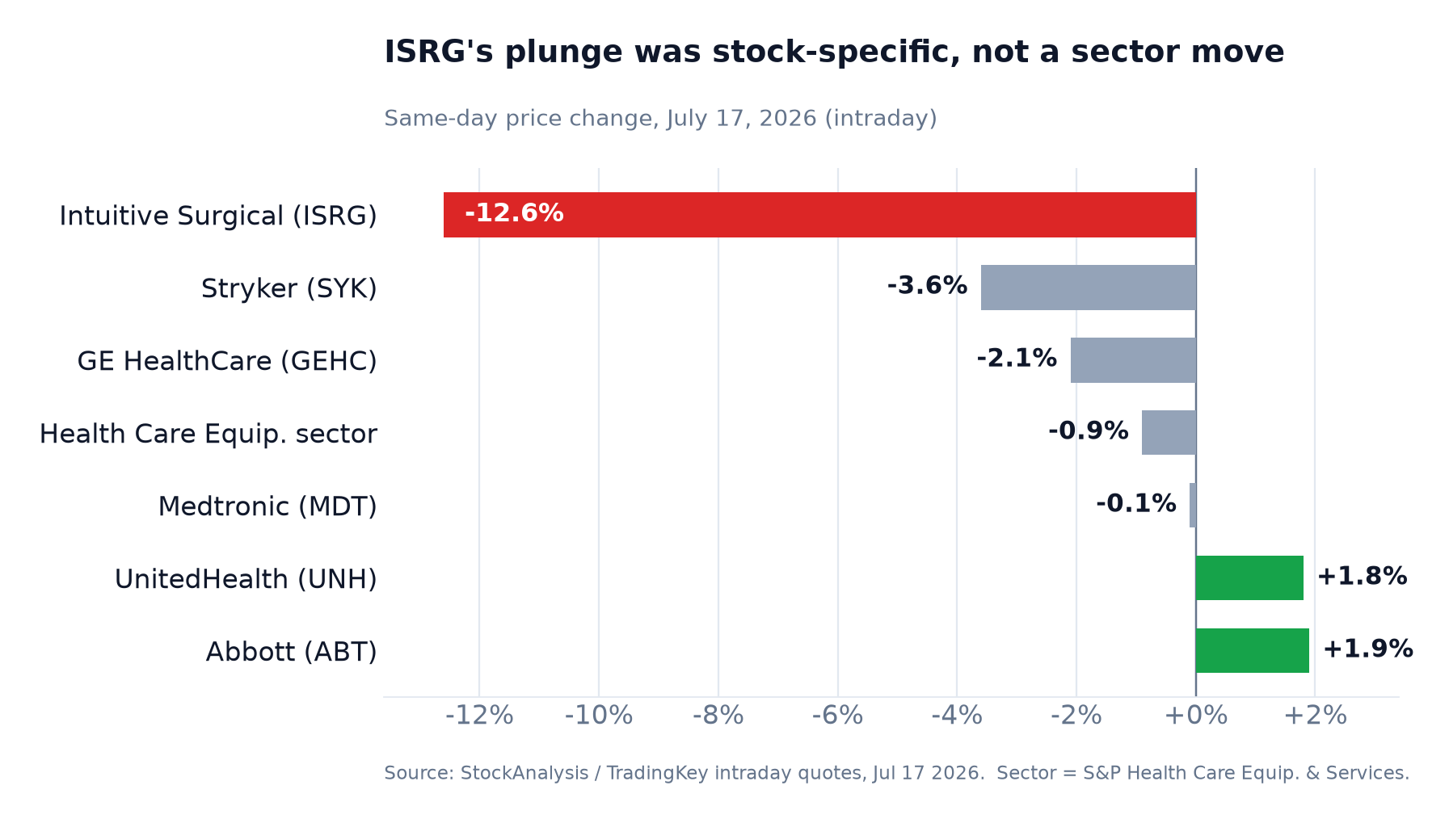

Intuitive Surgical dropped about 13% intraday to a fresh 52-week low the morning after beating Q2 estimates. The catalyst was the outlook, not the quarter: full-year da Vinci procedure-growth guidance of 13.5–15.5% implies a second-half deceleration, with moderating U.S. demand and an ACA coverage headwind. A ~40x multiple left no room for it, and six firms cut targets within hours — while the rest of medtech barely moved.

Summary

Intuitive Surgical (NASDAQ: ISRG) was trading around $351.66 early Friday afternoon, July 17, 2026, down about $50.67, or 12.6%, from Thursday's $402.33 close, with the session still open [1][2]. The move set a fresh 52-week low. The oddity is that it came the morning after a good quarter: reporting after Thursday's close, Intuitive beat on both lines — adjusted EPS of $2.80 against roughly $2.50 expected, and revenue of $2.89 billion, up 19% year over year [3][4]. The stock fell hard anyway.

This is a beat-and-drop driven by the outlook, not the quarter. Management guided full-year 2026 da Vinci procedure growth to 13.5%–15.5% — a range whose midpoint implies the second half decelerates from the first — and flagged moderating U.S. procedure growth, softness in deferrable "benign" cases, and the expiry of enhanced Affordable Care Act subsidies as a demand headwind [5]. On a stock that had already fallen roughly 30% year to date and made fresh lows the prior week, a premium multiple left no room for a guide-down, and Wall Street responded with a barrage of price-target cuts [7]. Crucially, this was company-specific: the broader medical-device group barely moved the same day.

| Evidence level | What can be said |

|---|---|

| Documented | ISRG beat Q2 estimates but guided FY26 da Vinci procedure growth to 13.5%–15.5%, implying an H2 slowdown; the stock fell ~12.6% to a 52-week low the next session and drew a wave of target cuts [3][5][7]. |

| Mechanically plausible | A ~40× earnings multiple on a name already down ~30% YTD de-rated when growth guidance confirmed a deceleration rather than a re-acceleration. |

| Not measurable from public data | How much of the drop is the guidance itself versus multiple compression versus forced de-risking by momentum holders — the split cannot be quantified from the tape. |

What changed

| Metric | Value | As of / source |

|---|---|---|

| Intraday price | ~$351.66 | Jul 17 2026, ~1:00 p.m. ET — StockAnalysis [2] (BestStocks feed: $351.80 at ~12:01 p.m. [1]) |

| Prior close (Jul 16) | $402.33 | StockAnalysis [2] |

| Intraday change | −$50.67 / −12.6% | Vs prior close; session ongoing [1][2] |

| Day's range | $349.90 – $367.74 | The low is a fresh 52-week low [2] |

| 52-week range | $349.90 – $603.88 | Today's plunge reset the low; ~42% below the high [2] |

| Volume by ~1:00 p.m. | ~6.77M sh | ~2.5× the ~2.67M 30-day average with roughly half the session left; BestStocks flagged turnover "very high" (~2.6× by noon) [1][2] |

| Market cap | ~$124.5bn | 354.16M shares; P/E ~40×, forward P/E ~31× [2] |

Two things frame the move. First, participation was heavy but not a blow-off: by early afternoon Intuitive had traded roughly 6.8 million shares — about 2.5× its ~2.7 million-share 30-day average with about half the session still to run, i.e. a genuinely high-volume down day, consistent with real repositioning rather than a thin, low-conviction slide [1][2]. Second, the drop set a new 52-week low and extended a de-rating that began well before this print — the stock entered the day already down about 30% for the year and had touched fresh lows on July 14 after pre-earnings target cuts — TD Cowen, for one, had already trimmed to $520 from $585 on valuation ahead of the print [8][9][12]. This was a guide-down onto an already-weak chart, not a bolt from the blue.

The quarter was fine — the outlook was the problem

On the numbers Intuitive delivered. Q2 adjusted EPS of $2.80 beat the ~$2.50 consensus by about 12%, and revenue of $2.89 billion rose 19% year over year, ahead of the ~$2.82 billion Street estimate [3][4]. The operating detail was strong too: worldwide procedures grew ~16% (da Vinci ~15%, Ion ~36%), the company placed 468 da Vinci systems — up from 395 a year ago, including 246 of the newer da Vinci 5 versus 180 — and the installed base pushed toward 13,000 systems [4].

What spooked the market sat in the outlook. Intuitive guided full-year 2026 da Vinci procedure growth to 13.5%–15.5%, with commentary pointing to the middle of that range [5]. Because the first half ran near the top of it (~15.3%), the guide implies a second-half deceleration to roughly the high-13% area — and for a company whose entire valuation rests on durable, compounding procedure volume, a decelerating growth rate matters more than a single quarter's beat. Management attributed the moderation to slower U.S. procedure growth (around 12% year over year), with particular softness in deferrable "benign" categories that patients appear to be putting off, and it flagged the expiry of enhanced ACA subsidies as a coverage headwind that could damp elective, robotic-assisted demand [5][1]. A recent Class II recall of certain da Vinci components added a smaller, secondary layer of pressure [1]. None of that is existential — but against a ~40× earnings multiple, "growth is slowing and coverage is a risk" is exactly the sentence that compresses a premium.

Analyst view

The most defensible reading is that this is a multiple de-rating triggered by a growth-rate guide-down, not a broken business. The quarter beat; systems placements and the da Vinci 5 ramp were healthy; the installed base keeps compounding. But Intuitive is priced as a secular compounder, and the market will not pay ~40× trailing earnings for a name whose second-half procedure growth is guided to slow while U.S. demand moderates and an ACA coverage headwind looms. The heavy volume — about 2.5× average with half the session to go — says this was real repositioning, not a thin drift, and the breadth of the target cuts (six firms in a day, plus Citi pulling it from its catalyst watch) says the sell-side is resetting its growth algorithm, not just its price decks [2][7].

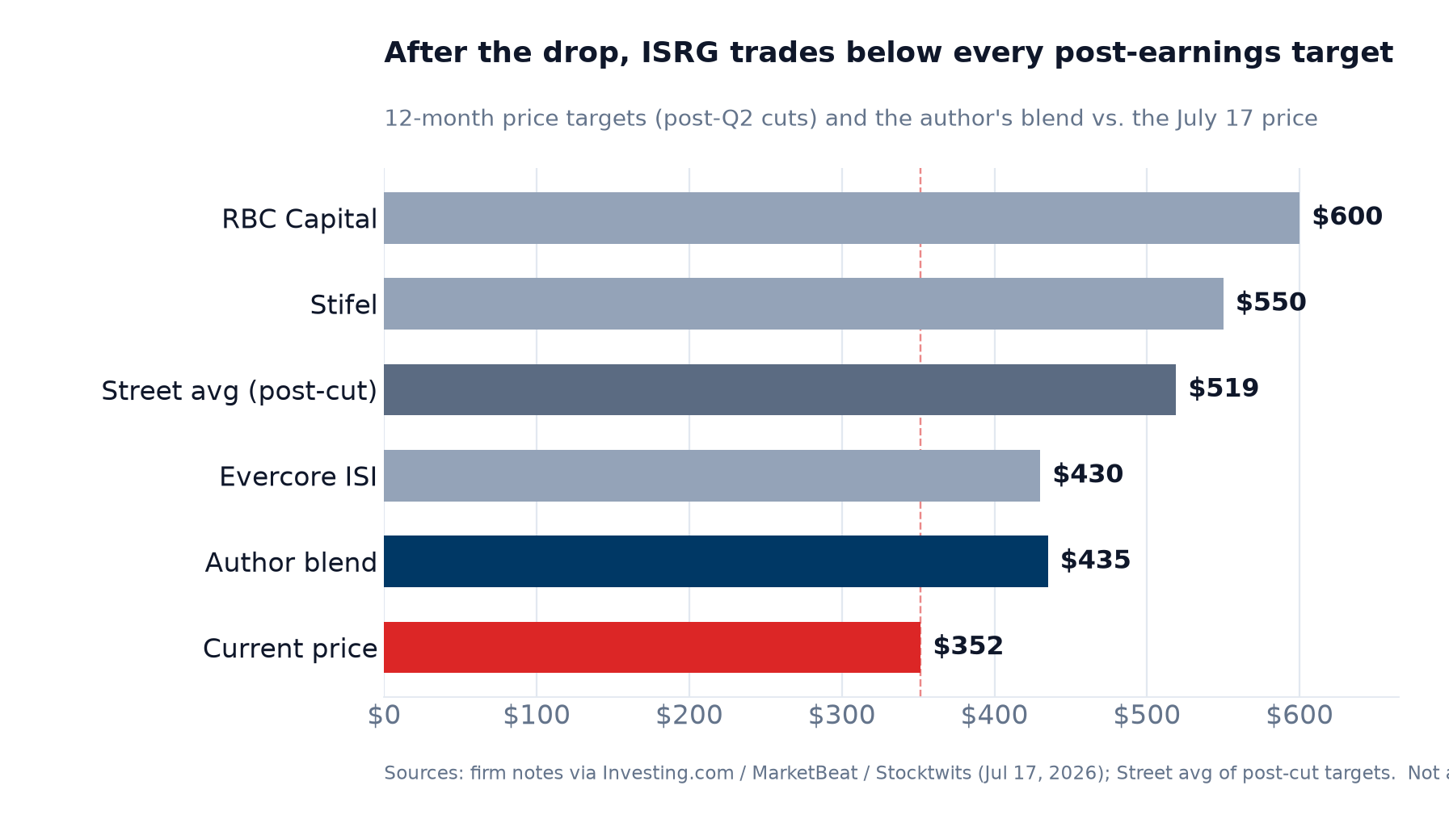

What this means for value: after the drop, ISRG at ~$352 trades below every published post-earnings target — from Evercore's freshly-cut $430 up to RBC's $600 — and roughly 32% under the ~$519 average of those reduced targets [7][10]. On the Street's numbers that looks like upside. On the author's more cautious probability-weighted blend (~$435, below), the stock sits about 19% under a reasonable fair value but only modestly above the bear case — which is another way of saying the tape is now pricing the H2 deceleration as closer to structural than transient. Which side is right turns on whether U.S. procedure growth stabilises and the ACA/benign-deferral drag proves temporary — questions the next two quarters, not this one, will settle.

It was Intuitive's problem, not medtech's

The single most useful context is the peer tape on the same day. If this were a sector event, its neighbours would have moved with it. They did not. On July 17 the S&P Health Care Equipment & Services group fell only about 0.9%, and several large healthcare names actually rose — UnitedHealth +1.8%, Abbott +1.9% [6]. Among device peers with elective-procedure exposure, Stryker slipped about 3.6% and GE HealthCare about 2.1%, while Medtronic was essentially flat at −0.1% — modest sympathy moves, nothing like Intuitive's double-digit break [6][14][15].

One timing note matters here, because it is easy to get wrong. Med-device stocks did sell off sharply earlier in the week — Stryker, Medtronic, Boston Scientific and GE HealthCare all fell several percent on July 14, after HCA Healthcare flagged softer surgical volumes [11]. That was a genuine sector scare, but it was three sessions earlier and had largely been digested by Friday. Intuitive's July 17 plunge stands on its own guidance, layered on top of a name that the July 14 news — and a string of pre-earnings target cuts — had already left near its lows [9][11].

The barrage of target cuts

Within hours of the report, at least six firms lowered their Intuitive price targets, and Citi pulled the stock from its "Upside 90-Day Catalyst Watch" — on top of the pre-earnings cut from TD Cowen noted above [7][12]. Most kept constructive ratings — the cuts were to targets, reflecting a lower growth algorithm rather than a wholesale change of thesis — but the direction was uniform.

| Firm | New target | Old | Rating |

|---|---|---|---|

| RBC Capital [7] | $600 | $650 | Outperform |

| Stifel [13] | $550 | $670 | Buy |

| Bank of America [7] | $520 | $650 | Buy |

| BTIG [7] | $512 | $574 | Buy |

| Mizuho [7] | $500 | $525 | Neutral |

| Evercore ISI [7] | $430 | $480 | In Line |

Even after the cuts, the targets cluster well above the ~$352 price — these six post-earnings targets average about $519, and the lowest, Evercore's $430, still sits ~22% higher [7][10]. The recurring worries in the notes were the same: the U.S. procedure-growth moderation, competitive encroachment from Medtronic's Hugo and Johnson & Johnson's Ottava robotic platforms, and a valuation that had priced in little disappointment [8].

What this means for value

Intuitive still earns a premium multiple for good reason — high margins, a razor-and-blade instrument model, and a compounding installed base — so the debate is about the rate of growth and the multiple the market will pay for it, not solvency. The scenario prices below are the author's own illustrative estimates, anchored to the published post-earnings target distribution (Evercore $430 to RBC $600, ~$519 average) and to how durable the procedure-growth deceleration proves — not derived from a formal DCF. They sum to 100%.

| Scenario | Price | Probability | Key driver |

|---|---|---|---|

| Bull | ~$520 | 25% | The H2 deceleration proves transient; U.S. procedure growth re-accelerates as benign-case deferrals unwind, and the da Vinci 5 / Ion mix lifts pricing — back toward the clustered post-cut Street targets ($500–$600) [4][7] |

| Base | ~$440 | 45% | Procedure growth settles in the low-to-mid teens and Intuitive re-rates from hyper-growth to steady compounder; the forward multiple compresses toward ~28–30× from ~31× — near the middle of the reduced target range [2][5] |

| Bear | ~$360 | 30% | Benign-case deferral and ACA coverage losses persist, Hugo/Ottava competition pressures share and pricing, and the premium multiple keeps compressing — near today's 52-week low and the ~$366 Street low [2][8] |

| Probability-weighted value ≈ $435 — the ~$352 price sits about 19% below it (and only modestly above the bear case), while the price is ~32% below the Street's ~$519 average target. | |||

Read the blend cautiously. At ~$435 it sits above the price, so on these assumptions the sell-off has pushed Intuitive below a reasonable fair value — but the gap to the bear case is small, which is the market's way of saying it is treating the second-half slowdown as more than a one-quarter wobble. The sell-side, clustered near $519 even after cutting, is markedly more optimistic. The distance between those two views — roughly $352 today, $435 on a cautious blend, $519 on the Street — is the whole debate in three numbers, and it resolves on procedure-growth durability, not on this beat. Treat the ~$435 figure as an illustrative probability-weighted value, not a target or a model output. This is the same beat-but-guidance pattern that has punished other quality names this season.

What to watch

- Q3 2026 procedure trends — the first hard read on whether the guided H2 deceleration is materialising or the benign-case deferrals are unwinding; the single biggest swing factor between the scenarios [5].

- U.S. coverage and the ACA subsidy cliff — any data on elective-procedure demand as enhanced subsidies lapse; this is the macro hook management itself flagged [5].

- Competitive traction from Medtronic's Hugo and J&J's Ottava — placement and procedure data from rival robotic platforms, which the bear case leans on [8].

- The da Vinci 5 ramp and instrument pull-through — whether the newer system keeps lifting placements (246 of 468 this quarter) and per-procedure revenue; the mechanism behind the bull case [4].

- Whether the multiple stabilises — at ~31× forward, ISRG is no longer priced for perfection; watch whether it holds near the ~$430–$440 area or keeps de-rating toward the ~$366 Street low [2][10].

Frequently asked questions

Why did Intuitive Surgical (ISRG) stock fall on July 17, 2026?

Intuitive fell about 12.6% to roughly $352 — a fresh 52-week low — the morning after it reported Q2 2026 results. The quarter actually beat: adjusted EPS of $2.80 topped the ~$2.50 consensus and revenue of $2.89 billion rose 19%. The problem was the outlook. Management guided full-year 2026 da Vinci procedure growth to 13.5%–15.5%, a range whose midpoint implies the second half slows from the first, and flagged moderating U.S. procedure growth, softness in deferrable 'benign' cases, and the expiry of enhanced ACA subsidies as a demand headwind. On a stock trading near 40x earnings, that growth-rate guide-down triggered a de-rating and a wave of analyst target cuts.

If Intuitive beat estimates, why did the stock drop so much?

Because the market prices Intuitive as a secular compounder, and a beat on the current quarter matters less than the trajectory of procedure growth — the engine of its valuation. Guidance of 13.5%–15.5% da Vinci procedure growth implies a second-half deceleration (the first half ran near 15.3%), and management pointed to slower U.S. demand and an ACA coverage risk. At about 40x trailing earnings there was no room for a slowdown, so the multiple compressed. It is a classic 'beat-and-drop' where the outlook, not the quarter, drives the reaction.

Was the ISRG drop part of a broader medical-device selloff?

No — it was overwhelmingly company-specific. On July 17 the S&P Health Care Equipment & Services group fell only about 0.9%, and large healthcare names like UnitedHealth (+1.8%) and Abbott (+1.9%) actually rose. Device peers moved modestly (Stryker −3.6%, GE HealthCare −2.1%, Medtronic −0.1%) versus Intuitive's ~12–13% break. A separate sector selloff did hit medtech on July 14 after HCA warned on surgical volumes, but that was three sessions earlier and distinct from Intuitive's guidance-driven move.

What did analysts do to their Intuitive Surgical price targets?

At least six firms cut targets within hours of the report, and Citi removed ISRG from its 'Upside 90-Day Catalyst Watch.' The cuts included RBC to $600 (from $650), Stifel to $550 (from $670), Bank of America to $520 (from $650), BTIG to $512 (from $574), Mizuho to $500 (from $525), and Evercore ISI to $430 (from $480); TD Cowen had already trimmed to $520 (from $585) ahead of the print. Most kept constructive ratings — they lowered targets to reflect a slower growth algorithm. Even after the cuts the targets average about $519, well above the ~$352 price.

Is Intuitive Surgical stock cheap after the drop?

It depends on your view of procedure growth. At ~$352 the stock trades below every post-earnings target (Evercore's $430 low to RBC's $600) and about 32% under the ~$519 average — so the Street sees upside. On the author's more cautious probability-weighted blend (bull $520 at 25%, base $440 at 45%, bear $360 at 30%, blended ~$435), the price sits roughly 19% below fair value but only modestly above the bear case, implying the market is treating the second-half deceleration as more structural than temporary. These figures are illustrative descriptive analysis, not investment advice.