Stock Analysis

Why Did IBM (IBM) Stock Crash ~26% on July 14, 2026?

IBM fell ~26% to about $215 on July 14 after unexpectedly releasing preliminary Q2 revenue of $17.2B versus ~$17.86B consensus — on pace to exceed its 23.7% Black Monday 1987 record. CEO Arvind Krishna said "we faltered," citing deals that failed to close on time and a late-June client capex shift into supply-constrained servers, storage and memory. The rest of the tape was consistent: selected hardware names rose while the software ETF turned positive by noon.

Summary

IBM (NYSE: IBM) collapsed on Tuesday, July 14, 2026, falling about 25.8% to roughly $215.29 — down nearly $75 from Monday's $290.23 close — as of 11:56 a.m. ET, with the session still open [1][2]. The catalyst came directly from IBM, which unexpectedly released selected preliminary second-quarter results before the open — issued as a letter to investors and filed with the SEC on Form 8-K — ahead of its scheduled July 22 report: revenue of $17.2 billion against a consensus near $17.86 billion, and operating (non-GAAP) EPS of $2.93 versus about $3.01 [4][5][6]. Chief executive Arvind Krishna's letter did not hedge: "this quarter we faltered" [4]. At that intraday level IBM was on pace for its worst closing-day decline on record, exceeding the 23.7% drop of October 19, 1987 — though the session had not closed, and only the closing print settles a record [6][7]. In one sentence: the market is pricing more than a quarterly miss — it is pricing a possible reset to IBM's Software growth, its execution credibility and its full-year outlook, while the peer tape offers only provisional support for management's broader capex-rotation explanation. The rest of this piece tests that claim.

What changed

IBM's explanation is unusually specific, and it points outward as much as inward. Three forces stack up in the company's own account.

| Driver | What IBM said | Segment effect |

|---|---|---|

| Capex reprioritization (the new news) | "In the last few weeks of June, we saw clients shift their quarterly capex spend toward servers, storage, and memory purchases to secure supply-constrained infrastructure ahead of expected price increases." IBM anticipated some supply-chain impact but "did not anticipate the magnitude" [4] | Infrastructure revenue −7% [4] |

| Z / Transaction Processing shortfall | IBM said it would be "wrapping on the launch of z17" in the quarter — lapping the launch period — and had guided Infrastructure to decline low-single digits for the year from this quarter. "What played out was worse than our expectations," driven by Z and "the associated software stack, primarily in Transaction Processing" [4] | Software +5% — growth, but a marked deceleration; BofA called it "well below the company's double-digit growth outlook" [4][9] |

| Execution and deal slippage | "We did not adapt and move quickly enough, and numerous large deals failed to close on the timelines we expected, driving the majority of our shortfall." Clients were also "distracted with rapidly-evolving, industry-wide cybersecurity concerns" [4] | Consulting flat (+1% at constant currency) [4] |

The capex explanation is the central claim of the day. IBM is not saying enterprise demand evaporated. It says some clients reprioritized quarterly capital spending toward servers, storage and memory — spending that may be associated in part with AI-infrastructure investment — and that the shift landed in the last few weeks of the quarter, which is why it caught the company late. Enterprise IT budgets can be constrained within a single quarter, so accelerated infrastructure purchases may delay other projects. If that account is right, it should leave some trace on the rest of the tape.

Why it matters

The uncomfortable possibility for software investors is that IBM may be an early reported example of enterprise IT budgets being reprioritized toward supply-constrained infrastructure — on management's account, at least. The AI infrastructure squeeze has largely been a margin story: chips and memory getting more expensive. What IBM describes is closer to a budget story, in which buyers facing supply constraints and expected price increases pull spending forward into hardware and other projects wait. IBM did not say memory alone caused the problem, and one company's quarter does not establish an industry pattern — but it says what gave was large deals that "failed to close on the timelines we expected" [4].

Set against that, IBM's own disclosure contains a genuine rebuttal to the bear case. Operating EPS of $2.93 still grew 5%, and operating pre-tax margin expanded 30 basis points to 19.2% even as the revenue line disappointed [4]. Red Hat growth accelerated sequentially to 11%. Distributed Infrastructure — the servers-and-storage business positioned for the very shift that hurt Z — posted its best performance in reported history, up 37%, exiting the quarter with roughly $500 million of backlog. Far from ending, the z17 program remains at nearly 130% program-to-program against z16, IBM's strongest mainframe cycle on record, with clients representing 85% of installed MIPs maintaining or growing capacity [4]. Year to date, free cash flow is $4.8 billion [4]. On the company's telling this is a timing-and-execution quarter rather than a demand collapse. The revenue shortfall itself was about 3.7% against consensus; the scale of the share-price response reflects the implied forward-growth and execution reset, and the credibility cost of an unscheduled warning, rather than the headline miss alone.

How the move compares

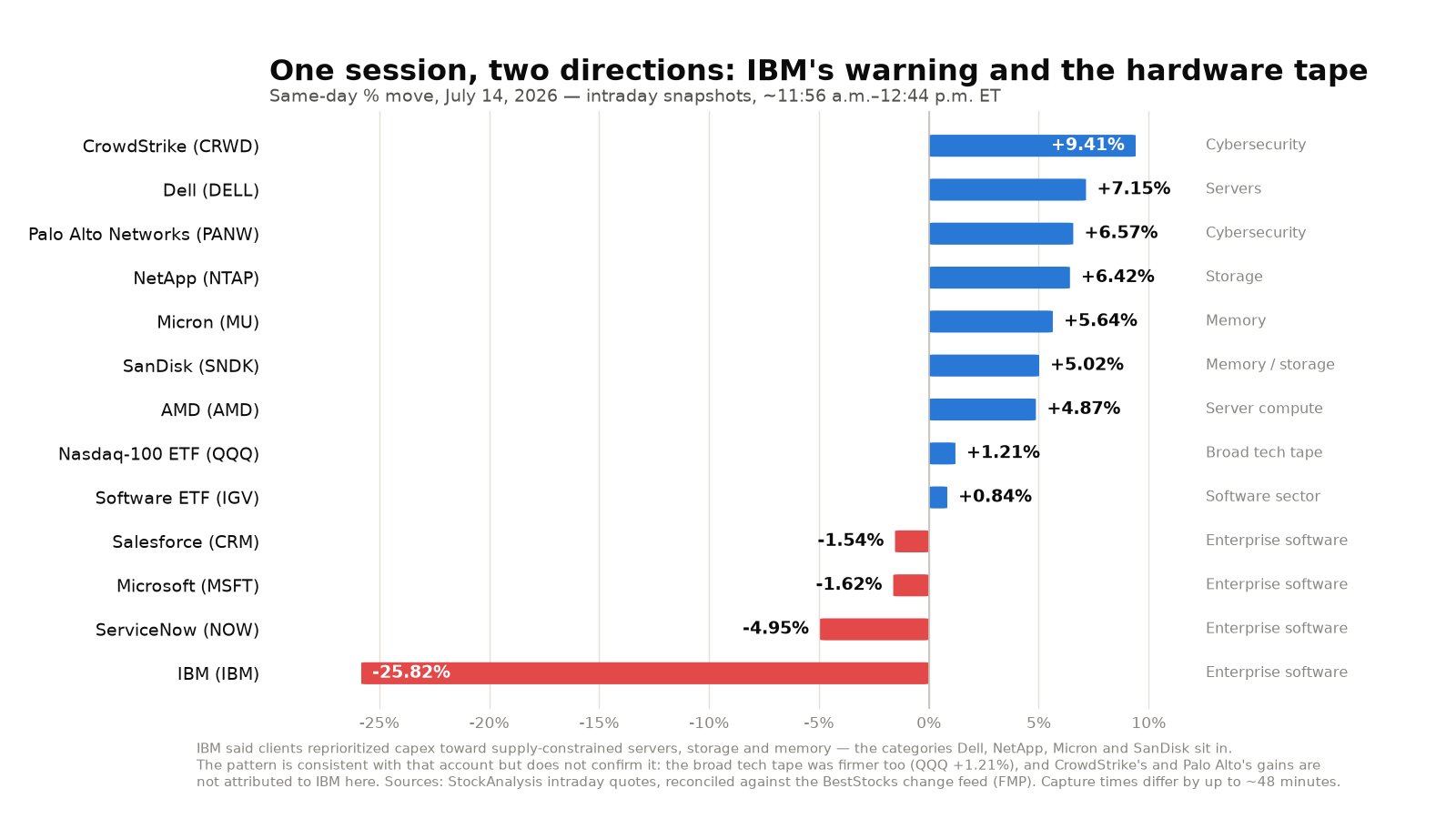

The peer tape is the best available test of IBM's story, and it cuts two ways. The software complex sold off hard at the open — 24/7 Wall St. recorded Microsoft about −3%, ServiceNow about −8% and the software ETF IGV about −4% in early trading, figures that reconcile approximately against those names' prior closes [7]. By midday much of that sympathy move had unwound, while IBM had not recovered.

| Stock / ETF | Early session [7] | Around noon (~12:00 p.m. ET) [12] | Read |

|---|---|---|---|

| IBM — International Business Machines | ~−22% | −25.82% | The source of the news; extended its loss [2] |

| NOW — ServiceNow | ~−8% | −4.95% | Hit hardest in sympathy; recovered ~3 points |

| MSFT — Microsoft | ~−3% | −1.62% | Roughly halved its loss |

| CRM — Salesforce | lower | −1.54% | Modest decline |

| IGV — iShares Expanded Tech-Software ETF | ~−4% ($89.31) | +0.84% ($93.48) | The sector proxy was positive around noon |

The IGV reversal is notable but not dispositive. It suggests investors had partially contained the read-through to the broader software sector by midday, though it does not rule out a broader budget effect: an ETF reflects all of its constituents and their own news, the wider technology tape was firmer regardless — the Nasdaq-100 ETF (QQQ) was up 1.21% at 12:42 p.m. ET [12] — and four hours of trading cannot resolve whether the capex issue is company-specific or industry-wide. What can be said is that the mechanics IBM described are specific to IBM — a mainframe launch it was lapping, the Transaction Processing stack attached to it, and deals its own teams did not close — and that the market's initial contagion reflex faded rather than built. July 22 can still overturn that.

The other side of the tape is where IBM's explanation gets its best circumstantial support. The three categories Krishna named — servers, storage and memory — were, by early afternoon, the day's strongest: Dell (DELL) +7.15%, NetApp (NTAP) +6.42%, Micron (MU) +5.64% and SanDisk (SNDK) +5.02%, with AMD +4.87% on the server-compute side [12] — a continuation of the memory strength we covered in Monday's SanDisk selloff analysis. Those are close to a literal read of the sentence in IBM's letter. The pattern is consistent with management's account, but it is not confirmation: the broad technology tape was firmer regardless, with the Nasdaq-100 ETF (QQQ) up 1.21% while IBM fell [12], so some of that strength is simply the day's beta rather than a dollar-for-dollar transfer out of IBM's contracts.

One more strand is worth handling carefully, because the obvious inference is probably wrong. CrowdStrike (CRWD) rose 9.41% and Palo Alto Networks (PANW) 6.57% [12], and it is tempting to tie a security-sector bid to Krishna's remark that clients were "distracted with rapidly-evolving, industry-wide cybersecurity concerns" [4]. The timeline does not support it. The security complex had been rallying on its own catalysts for weeks before IBM said anything: Palo Alto rose 9% and CrowdStrike 7% on June 29; the group gained again on July 6 after Scotiabank upgraded Okta to Outperform and framed identity vendors as AI beneficiaries; and CrowdStrike then collected target increases from UBS ($235, July 7) and Benchmark ($230, around July 8) [12][13]. Tuesday's move is a continuation of a documented, analyst-driven trend, so the fact that these names moved as a basket is what that trend predicts rather than evidence of an IBM effect. We found no same-day reporting establishing a link, and we do not assert one — though IBM's remark may have added to an existing bid, which is not something a single session can separate out.

Why did IBM (IBM) stock crash on July 14, 2026?

IBM fell about 26% to roughly $215 because the company itself released weak preliminary second-quarter results before the market opened — an unscheduled, self-inflicted catalyst ahead of its July 22 report [4]. Revenue came in at $17.2 billion against consensus near $17.86 billion, and operating EPS at $2.93 versus about $3.01 [6]. CEO Arvind Krishna told investors "this quarter we faltered," attributing the majority of the shortfall to large deals that failed to close on the expected timelines, and citing a late-June shift in client capital spending toward supply-constrained servers, storage and memory, plus a Z mainframe and Transaction Processing software shortfall as IBM lapped the z17 launch [4]. At its intraday low the decline was on pace to exceed IBM's 23.7% drop of October 19, 1987 and rank as its worst closing-day decline on record, though the session had not closed [6][7]. Full results and a discussion of full-year expectations are due July 22 [4].

IBM analyst price targets: where the Street stands

Timing matters more than usual here, so the table separates actions taken before the warning from responses to it. Percentage gaps are measured against the ~$215.29 midday price on July 14.

| Firm | Date | Rating | Target (old → new) | Gap to ~$215.29 |

|---|---|---|---|---|

| Evercore ISI (response) | Jul 14 | Outperform (reiterated) | $310 [10] | +44.0% |

| Bank of America (response) | Jul 14 | Buy (maintained) | $330 → $280 [9] | +30.1% |

| HSBC (action dated the day before) | Jul 13 | Hold → Reduce | $231 → $191 [8] | −11.3% |

| Consensus (24 analysts) | Jul 14 | Buy | ~$293.46 average; range $191–$390 [11] | +36.3% |

Two caveats do a lot of work in that table. First, the $293.46 consensus is likely to be stale: it sits about 1.1% above Monday's close, and many of its component targets predate the warning, so it should not be treated as a clean post-warning valuation [11]. Second, HSBC's downgrade is not a response to the miss, despite surfacing in the same news cycle: analyst Abhishek Shukla downgraded IBM on Monday — per a report published Tuesday morning — arguing IBM's 22.0x CY27 earnings multiple was stretched against a 16.9x sector median, and that investors could replicate IBM's business mix by buying a "synthetic IBM" basket of SAP, Accenture, HP and IonQ for $287.56, against IBM's own $290.23 price [8]. It was a valuation call that happened to land one day early. Among the target and rating actions verified here, two were clearly issued in response to the warning, and both stayed bullish: BofA kept a Buy while cutting to $280 and now values IBM at 20x CY27 EV/free cash flow (from 21x), explicitly expecting IBM to lower full-year expectations, "particularly in software" [9]; Evercore ISI reiterated Outperform and a $310 target following the negative pre-announcement [10]. Others commented the same day without a verified target change, and several marks that aggregators list under July 14 are older: Morgan Stanley's $293 and Oppenheimer's $350 were earnings previews written before the warning, and Stifel's $290 dates to April 8 [11].

The July 14 move in numbers

| Measure | Value | As of / source |

|---|---|---|

| IBM price (midday) | ~$215.29 | −$74.94, ≈−25.82%; Jul 14, 11:56 a.m. ET — StockAnalysis [2] |

| Cross-check | $214.44 | ≈−26.11%; Jul 14, 11:30 a.m. ET — BestStocks change feed (FMP) [1] |

| Prior close, Mon Jul 13 | $290.23 | Reference close; both sources agree [1][2] |

| Intraday range | $213.22 – $229.92 | Session ongoing; Jul 14, 11:56 a.m. ET [2] |

| Volume (midday) | 38,538,132 shares | ≈4.2x the ~9.2M 20-day average, before noon [2][3] |

| 52-week range | $212.34 – $332.46 | Trading within ~1.4% of the 52-week low [2] |

| Market cap | ~$202.35B | 939.89M shares outstanding × $215.29 [2][3] |

| Beta (5-year) | 0.67 | Lower historical volatility than the market [3] |

| Short interest | 34.28M shares | Latest reported; 3.65% of shares outstanding [3] |

| Q2 revenue (preliminary) | $17.2B, +1% | vs ~$17.86B consensus — a ~3.7% miss [4][6] |

| Q2 operating EPS (preliminary) | $2.93, +5% | vs ~$3.01 consensus; GAAP $2.27, −2% [4] |

IBM stressed that these are preliminary figures: it is "still working to close" the quarter and final results "could be slightly different" [4].

IBM fair-value scenarios after the crash

The scenarios below are the author's hypothetical, illustrative estimates — editorial weights anchored to cited Street targets, not a DCF or a consensus model. Two inputs are our own assumptions rather than published figures: the ~$13.19 CY27 EPS derived from HSBC's stated 22.0x multiple at IBM's $290.23 price, and the decision to use HSBC's cited 16.9x sector median as the base-case multiple. HSBC identified 16.9x as the sector median; it did not describe that as IBM's fair multiple.

| Scenario | Price | Prob. | Valuation basis | Key drivers |

|---|---|---|---|---|

| Bull | ~$280 | 30% | Target-anchored — BofA's post-warning $280 [9] | The quarter proves to be timing rather than demand: deals that missed the quarter-end deadline subsequently close, z17 holds near 130% program-to-program, Red Hat's 11% acceleration and Distributed Infrastructure's +37% carry the mix, and the July 22 reset is modest |

| Base | ~$223 | 45% | Multiple-based — 16.9x × ~$13.19 CY27 EPS; both inputs author-derived [8][11] | Software resets to mid-single-digit growth and the full-year outlook comes down on July 22; IBM holds roughly the sector median on an unrevised CY27 estimate |

| Bear | ~$191 | 25% | Target-anchored — HSBC's pre-warning sum-of-the-parts $191 [8] | The capex reprioritization proves structural rather than a late-June quirk; Transaction Processing keeps eroding, and a deeper cut lands July 22 |

Probability-weighting those cases (0.30×$280 + 0.45×$223 + 0.25×$191) gives a probability-weighted scenario price — an illustrative midpoint, not a valuation-model output — of about $232, roughly 8% above the ~$215.29 midday price. The blend is not especially sensitive to the weights: shifting five percentage points from the bear case to the bull case moves it only about $4, to roughly $237. It is sensitive to the EPS input, however — trimming the CY27 estimate 5% before applying the same 16.9x would pull the base case to about $212 and the blend to roughly $227, only about 5.5% above the midday price. The more durable observation is how narrow the bull-bear spread is — $191 to $280, a range of about 41% of the current price. On an unrevised, author-derived CY27 estimate, IBM's midday price was near the 16.9x sector median HSBC cited, and free cash flow of $4.8 billion year to date is a matter of record; the debate is not about survival but about whether one quarter's missed deals become next year's lost share.

Was this an IBM problem or a software-sector problem?

On the morning's evidence, primarily an IBM problem — though the question is genuinely open until July 22. The case for "IBM-specific" rests on the mechanics IBM described, which are its own: a z17 launch it was lapping, the Transaction Processing software stack attached to it, and deals its teams did not close on time, which Krishna explicitly owned rather than blaming on the environment [4]. The peer tape is supporting evidence, not proof: software names sold off at the open and then largely recovered, with the IGV software ETF positive by around noon while IBM stayed down roughly 26% [12]. That suggests the immediate contagion was contained, but an ETF's move reflects many constituents and a firmer broader tape, so it cannot settle the question. The case for "something broader" rests on the capex claim itself: if enterprise buyers really are diverting budget into supply-constrained memory and servers ahead of price increases, that is not a dynamic unique to IBM's customer list, and the strength in selected hardware names is at least consistent with it. The distinction decides whether IBM's drawdown is an isolated re-rating or an early data point in a trend — and no single session can resolve it.

What would prove this reading wrong

Each of the interpretations above is falsifiable, and July 22 is the first real test. Stating the disconfirming evidence in advance is the only honest way to publish a same-day explanation.

| Interpretation | What would weaken it |

|---|---|

| IBM-specific — this was execution, not the industry | Other enterprise vendors report the same late-quarter capex displacement in their own results. If the pattern repeats at peers, "IBM faltered" becomes "the budget moved" |

| Timing — the deals slipped rather than vanished | The deals that missed the quarter-end deadline do not close in the second half. IBM said they failed to close on the expected timelines; it did not say they were safe [4] |

| Valuation — the de-rating has largely happened | CY27 EPS estimates fall substantially more than the 5% our sensitivity assumes, which would lift the effective multiple and pull the scenario blend toward the current price |

| Contained — the software read-through faded for good reason | IGV and the major SaaS names resume falling into their own prints, which would suggest the noon recovery was a firmer broad tape rather than a considered verdict [12] |

What IBM investors should watch next

First and above all, July 22: IBM reports full second-quarter results and holds its call at 5:00 p.m. ET, where it said it will "discuss our full-year expectations" — the guidance reset is the real event, and BofA already expects a cut, particularly in software [4][9]. Note IBM's caveat that it is "still working to close" the quarter and that final results "could be slightly different" [4]. Second, whether the deals that missed the quarter-end deadline subsequently close: IBM said they failed to close on the expected timelines, not that they are safely deferred, so the H2 signings commentary is what tests the timing thesis. Third, Software's growth rate: +5% is the number that decides the multiple; Red Hat's 11% acceleration is the offsetting evidence [4]. Fourth, the target reset: the ~$293 consensus contains many pre-warning marks and is likely to fall — where it lands relative to the $232 blended scenario price will show where the Street really sits [11]. Fifth, the memory-price cycle: if supply constraints ease, the capex reprioritization IBM describes should reverse, which would be a tailwind for its Software line and a headwind for the names that rallied on Tuesday — see our SanDisk memory-selloff analysis and our Ultra Clean (UCTT) semiconductor-rally explainer for that side of the trade. Finally, whether the sympathy move stays contained: if ServiceNow, Salesforce and Oracle resume falling into their own prints, the market will have decided IBM was the messenger rather than the message. More market-mover breakdowns are in the BestStocks research hub.

IBM (IBM) stock-crash FAQ

Why did IBM stock crash on July 14, 2026?

IBM unexpectedly released weak preliminary second-quarter results before the open, ahead of its scheduled July 22 report: revenue of $17.2 billion against consensus near $17.86 billion, and operating EPS of $2.93 versus about $3.01. CEO Arvind Krishna said "this quarter we faltered," attributing most of the shortfall to large deals that failed to close on the expected timelines, alongside a late-June shift in client capital spending toward supply-constrained servers, storage and memory, and a Z mainframe and Transaction Processing shortfall as IBM lapped the z17 launch. The stock fell about 26% to roughly $215.

Is this IBM's worst day ever?

It depends on the close. IBM's prior record one-day decline was 23.7% on October 19, 1987 (Black Monday). At about -26% intraday on July 14 the move was on pace to exceed that and rank as IBM's worst closing-day decline on record, but the session was still open at the time of writing, and only the closing figure settles a record. Coverage differed accordingly as the intraday percentage moved: outlets measuring roughly -22% to -24% called it the worst day since 1987, while others called it the worst ever.

Did IBM cut its full-year guidance?

No — not yet. IBM's July 14 letter released only selected preliminary second-quarter figures and deferred the outlook, saying the company would "discuss our full-year expectations" on its regularly scheduled July 22, 2026 call at 5:00 p.m. ET. IBM also cautioned that it is still closing its books and that final results could be slightly different. BofA said it expects IBM to lower full-year expectations, particularly in software, but as of July 14 that had not happened.

Was the HSBC downgrade the reason IBM stock fell?

No. HSBC's downgrade of IBM to Reduce from Hold, with its target cut to $191 from $231, was an action dated Monday, July 13 — the day before the warning — on valuation grounds, arguing IBM's 22.0x CY27 earnings multiple was stretched versus a 16.9x sector median. The report carrying it was published Tuesday morning, which is why it surfaced in the same news cycle and is easy to mistake for a reaction, but the trigger was IBM's own preliminary Q2 release. The verified same-day responses were BofA cutting its target to $280 from $330 while keeping a Buy, and Evercore ISI reiterating Outperform with a $310 target.

Did IBM's warning drag down other software stocks?

Briefly, then less so. Software names sold off at the open — Microsoft about -3%, ServiceNow about -8% and the IGV software ETF about -4% — but by midday much of that had unwound, with IGV positive at +0.84% while IBM stayed down roughly 26%. Selected hardware and semiconductor names were higher: SanDisk +5.02%, Lam Research +4.89% and AMD +4.87%. That suggests the immediate read-through to software was contained, though a four-hour price observation cannot rule out a broader budget effect.

What is the analyst price target for IBM after the drop?

The published consensus was about $293.46 across 24 analysts with a Buy rating and a $191-$390 range, but that figure is likely stale — it sits about 1.1% above Monday's close, and many component targets predate the warning. The two verified post-warning marks are BofA at $280 (Buy, cut from $330) and Evercore ISI at $310 (Outperform, reiterated), while HSBC's $191, from an action dated the prior day, is the Street's low.