Stock Analysis

Why Did Ultra Clean Holdings (UCTT) Stock Jump 10%? A High-Beta Bet on the WFE Rally

UCTT surged about 10% on July 8 — but as the high-beta amplifier of a sector-wide chip-equipment rally on fresh WFE-forecast hikes, not on any company news. Volume ran only modestly above average.

Summary

Ultra Clean Holdings (NASDAQ: UCTT) jumped about 10% intraday on Wednesday, July 8, 2026, trading near $99.87 against Tuesday's $90.78 close — the largest gainer on BestStocks' change feed for the session, a roughly $9.09 move [1][2]. The feed framed the catalyst generically — “rising AI-driven WFE spending” — but there was no company-specific news on the tape and no analyst action on UCTT that day [1][10]. What actually moved the stock was the sector around it. Wafer-fab-equipment (WFE) names rallied broadly after Citi added an “upside catalyst watch” on Taiwan Semiconductor (TSM) ahead of its July 16 report — sending TSMC up about 5.3% — and after a fresh round of WFE-spending forecast hikes from Susquehanna and Bank of America [5][6][7]. UCTT, a high-beta supplier of subsystems to the equipment makers, simply amplified the group move: it rose two-to-four times as much as its own customers [8]. And it did so on volume running only about 1.2x its recent average — elevated, but not the blowout a 10% day might imply [3].

What changed

At the company, nothing. Ultra Clean did not report earnings, announce a contract, or draw an upgrade on July 8; its next scheduled catalyst is second-quarter earnings, estimated for on or around July 27, 2026 [1]. In fact, the most recent rating action on the stock was a bearish one — Weiss Ratings reiterated a “Sell” on June 26 — and a research note that same week counted one downgrade and zero upgrades over the prior month [4][10]. This was a sector move that a high-beta name exaggerated, not a re-rating of Ultra Clean itself.

The sector catalyst was concrete. On July 8, Citi analyst Laura Chen added a 30-day “upside catalyst watch” on TSMC while keeping a Buy rating, arguing the foundry is likely to raise its 2026 outlook at its July 16 analyst meeting on strong AI-chip demand and tight advanced-node and packaging supply; TSMC rose about 5.3% to $457.29 and pulled the equipment complex with it [6]. That landed on top of a WFE-forecast re-rating already underway: on July 6, Susquehanna lifted its wafer-fab-equipment market forecast to about $250 billion by 2028 — a roughly 20% increase — and raised targets across the group, including Advanced Energy (AEIS) to $535 from $430 and Lam Research (LRCX) to $475 from $385 [5]. Bank of America, separately, models semiconductor-equipment growth of roughly 10% and 14% in 2026 and 2027 toward $131 billion and $150 billion, driven by high-bandwidth memory, higher-layer NAND, leading-edge logic, and advanced packaging [7]. Micron's (MU) record-capacity messaging and roughly 800-trillion-won Korean fab plans from Samsung and SK Hynix round out the demand backdrop [7].

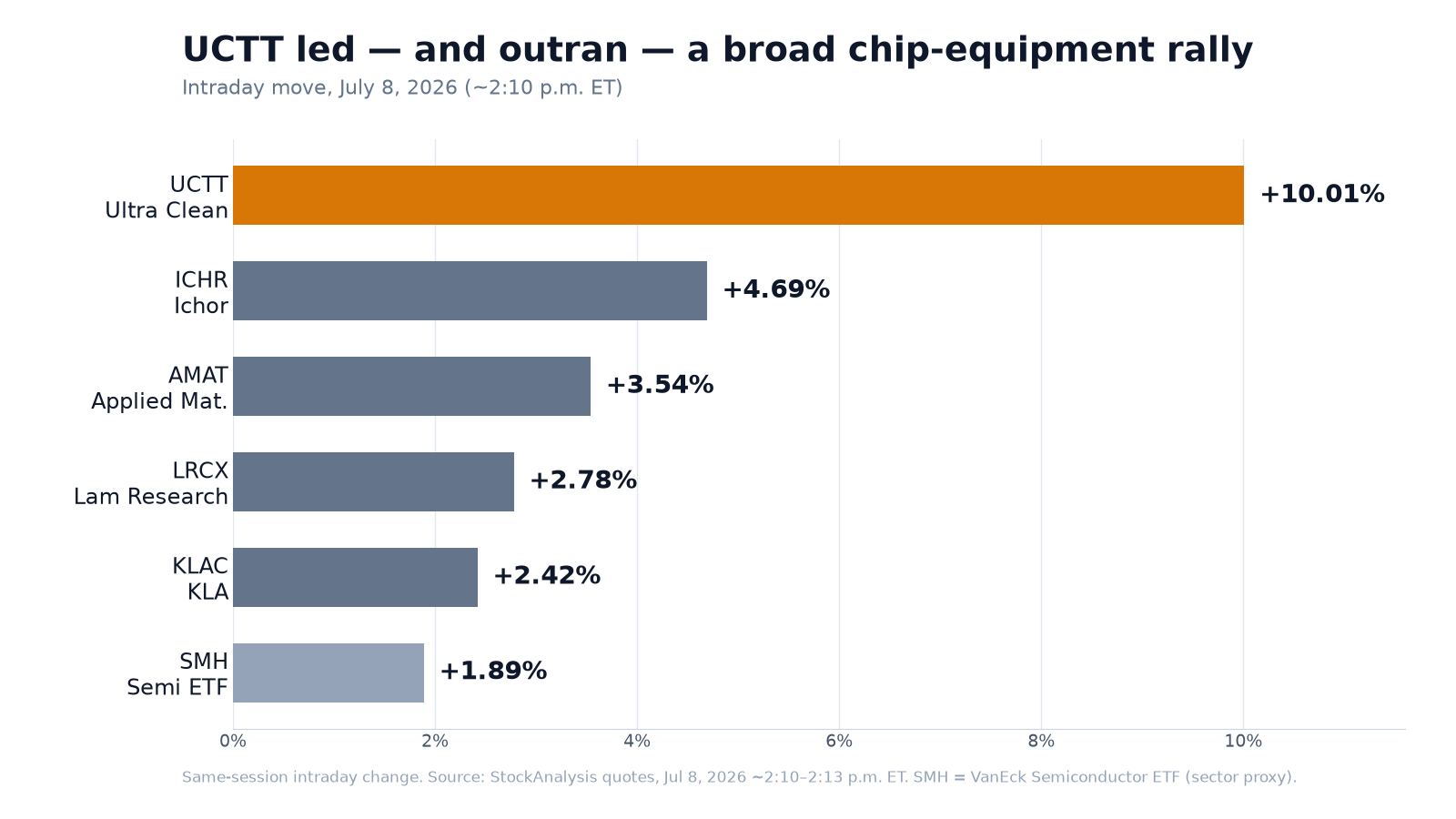

Ultra Clean's role explains the amplification. It builds the critical subsystems, components, and modules — gas and fluid delivery, precision robotics, frames — that go inside the tools sold by Applied Materials (AMAT), Lam Research, and KLA (KLAC). That makes it a second-derivative play on WFE spending, and it trades like one: its five-year beta is about 1.83 [3]. On July 8, that leverage showed. Against UCTT's roughly 10%, closest subsystem peer Ichor (ICHR) rose about 4.7%, Applied Materials 3.5%, Lam Research 2.8%, and KLA 2.4%, while the VanEck Semiconductor ETF (SMH) added just 1.9% [8]. The move also has to be read against the stock's recent path: UCTT is up more than 300% over the past year and touched a 52-week high of $144.22, then gave much of it back in the early-July semiconductor selloff — so Wednesday's pop is a bounce off that pullback, with the shares still about 31% below their high [2][3].

Why it matters

Ultra Clean's outsized day is a clean illustration of how the market prices the “supplier to the suppliers” layer of the AI build-out. When forecasts for wafer-fab-equipment spending rise, the capital flows first to the tool makers — Applied Materials, Lam Research, KLA — and then, with a multiplier, to the subsystem vendors that populate those tools. That multiplier cuts both ways: UCTT's beta near 1.8 means it tends to lead the group up on optimistic days and fall hardest when the cycle wobbles, as it did in early July [3]. For investors, the takeaway is that a move like Wednesday's says more about sentiment toward the WFE cycle — and about positioning in a heavily shorted, high-beta name — than about anything specific to Ultra Clean.

It also matters because the demand signals behind the rally are real and improving. Tight advanced-node and packaging capacity, high-bandwidth-memory expansion tied to AI accelerators from NVIDIA (NVDA) and Broadcom (AVGO), and multi-hundred-billion-dollar fab commitments in Korea and Taiwan all point to a multi-year equipment upcycle that Ultra Clean is positioned to serve [5][7]. The question for the stock is not whether that spending is coming, but how much of it is already in a share price that has tripled in a year.

What to watch

First, second-quarter earnings, estimated for on or around July 27, 2026 — the next hard test of whether order momentum matches the WFE optimism, and the moment a stock trading at its consensus target has to justify the run [1]. Second, TSMC's July 16 report and analyst meeting: Citi's whole catalyst-watch thesis rests on a guidance raise there, so a disappointment would remove the prop under the entire equipment complex, including UCTT [6]. Third, analyst actions on Ultra Clean specifically — whether any firm follows the sector optimism with an upgrade, or whether the Weiss “Sell” and the recent downgrade prove more prescient [4]. Finally, watch the tape: a 10% gain on roughly 1.2x volume needs follow-through on rising participation to confirm; if the short-covering fades, a high-beta name can round-trip a bounce as quickly as it delivered it [2][3].

Why did UCTT stock jump on July 8, 2026?

Ultra Clean Holdings (UCTT) jumped about 10% intraday, from a $90.78 prior close to roughly $99.87, as part of a broad wafer-fab-equipment rally — not on company news [1][2]. Semiconductor-equipment stocks rose after Citi put an “upside catalyst watch” on TSMC ahead of its July 16 report and after Susquehanna and Bank of America raised WFE-spending forecasts [5][6][7]. As a high-beta subsystem supplier, UCTT amplified the move, rising two-to-four times as much as customers like Applied Materials, Lam Research, and KLA, on volume only about 1.2x its recent average [8].

Was there any company-specific news for Ultra Clean on July 8?

No. There was no earnings report, contract, or analyst rating change on Ultra Clean that day. The most recent analyst action was a “Sell” reiteration from Weiss Ratings on June 26, 2026, and a note that week counted one downgrade and no upgrades over the prior month [4][10]. The move was a sector-driven, high-beta rebound after the early-July semiconductor selloff.

The July 8 move in numbers

| Measure | Value | Note |

|---|---|---|

| UCTT prior close, Tue Jul 7 | $90.78 | Bounce baseline [1][2] |

| UCTT intraday, Wed Jul 8 (StockAnalysis) | $99.87 | +10.01%, +$9.09; ~2:10 p.m. ET [2] |

| UCTT intraday, Wed Jul 8 (site feed) | $99.79 | +9.93%, +$9.01; last update 1:32 p.m. ET [1] |

| Day's range | $88.55 – $100.74 | StockAnalysis, Jul 8 [2] |

| Volume vs. average | ~1.37M by ~2:10 p.m. ET vs. 1.59M 20-day avg | ~1.2x full-session pace [2][3] |

| 52-week range | $21.28 – $144.22 | ~31% below the high [2] |

| Market capitalization | ~$4.48 billion | Jul 8, 2026 [2] |

| 5-year beta / short interest | ~1.83 / ~7.8% of shares | High-beta, heavily shorted [3] |

| Consensus price target | ~$107 (Buy) | Near Wednesday's price [4] |

How did UCTT move versus its semiconductor-equipment peers?

| Stock | Jul 8 intraday move | Role |

|---|---|---|

| UCTT — Ultra Clean | +10.0% | Subsystem supplier (high beta) [2] |

| ICHR — Ichor | +4.7% | Closest subsystem peer [8] |

| AMAT — Applied Materials | +3.5% | WFE OEM / customer [8] |

| LRCX — Lam Research | +2.8% | WFE OEM / customer [8] |

| KLAC — KLA | +2.4% | Process-control OEM [8] |

| SMH — VanEck Semiconductor ETF | +1.9% | Sector proxy [8] |

| TSM — Taiwan Semiconductor | +5.3% | Catalyst (Citi watch) [6] |

What is the analyst price target for UCTT?

The consensus rating is “Buy” with a price target around $107, close to where the stock traded on July 8 [4]. Recent actions include Oppenheimer's Edward Yang raising his target to $115 from $100 (Outperform, June 9), UBS's Timothy Arcuri initiating at Buy with a $130 target (May 5), and spring hikes from TD Cowen (to $100) and Needham (to $92) [4][9]. The lone bear is Weiss Ratings, which reiterated a “Sell” on June 26 [4].

Is Ultra Clean a good AI / WFE play?

Ultra Clean is genuinely levered to the wafer-fab-equipment upcycle: it supplies the subsystems inside tools from Applied Materials, Lam Research, and KLA, so rising WFE spending flows through to its orders with a multiplier [5][7]. That leverage — a beta near 1.8 — makes it a high-torque way to express the AI-capex theme, but it also means sharper drawdowns when the cycle wobbles, and after a more-than-300% one-year run the shares already trade near their consensus target [3][4]. It is a momentum-sensitive, cyclically-timed name rather than a low-risk one.

What could move UCTT next?

The next scheduled catalyst is Ultra Clean's second-quarter earnings, estimated on or around July 27, 2026, followed closely by TSMC's July 16 report — the guidance event underpinning the sector's rally [1][6]. Between now and then, watch for any analyst action on UCTT itself, further WFE-forecast revisions, and whether Wednesday's gain holds on rising volume or fades as short-covering runs its course [2][4].

Ultra Clean Holdings (UCTT) stock FAQ

Why did Ultra Clean Holdings (UCTT) stock jump on July 8, 2026?

UCTT rose about 10% intraday, from a $90.78 prior close to roughly $99.87, as part of a broad wafer-fab-equipment rally rather than on company news. Semiconductor-equipment stocks rallied after Citi placed an 'upside catalyst watch' on TSMC ahead of its July 16 report and after Susquehanna and Bank of America raised WFE-spending forecasts. As a high-beta subsystem supplier, UCTT amplified the move.

Was there company-specific news for Ultra Clean on July 8?

No. There was no earnings report, contract, or analyst rating change on Ultra Clean that day. The most recent analyst action was a 'Sell' reiteration from Weiss Ratings on June 26, 2026. The jump was a sector-driven, high-beta rebound after the early-July semiconductor selloff.

How much did UCTT move versus its peers?

About two-to-four times as much. Against UCTT's roughly 10%, subsystem peer Ichor (ICHR) rose about 4.7%, Applied Materials 3.5%, Lam Research 2.8%, and KLA 2.4%, while the VanEck Semiconductor ETF (SMH) added just 1.9% — consistent with UCTT's high beta near 1.8.

What is driving the semiconductor-equipment rally?

Rising forecasts for wafer-fab-equipment (WFE) spending tied to AI. Susquehanna lifted its WFE market forecast to about $250 billion by 2028, Bank of America models roughly 10–14% equipment growth in 2026–2027, and Citi flagged a likely guidance raise at TSMC's July 16 meeting — all supported by high-bandwidth-memory expansion and multi-hundred-billion-dollar fab plans in Korea and Taiwan.

Was the UCTT jump driven by a short squeeze?

Short-covering likely amplified it. Short interest is near 7.8% of shares outstanding, and the 10% gain came on volume running only about 1.2x the recent average with no company news — a setup that tends to force high-beta shorts to cover rather than one that signals fresh institutional accumulation.

What is the analyst price target for UCTT?

The consensus rating is 'Buy' with a price target around $107, close to where the stock traded on July 8. Oppenheimer is at $115 (Outperform), UBS initiated at $130 in May, and Weiss Ratings is the lone 'Sell.' With the stock near consensus after a more-than-300% one-year run, the sell-side sees limited modeled upside before earnings.

When does Ultra Clean Holdings report earnings?

Second-quarter earnings are estimated for on or around July 27, 2026. TSMC's July 16 report and analyst meeting — the guidance event underpinning the sector's rally — comes first and is a key read-through for the whole equipment complex, including UCTT.