Stock Analysis

Why Did SanDisk (SNDK) Stock Drop ~12% on July 13, 2026?

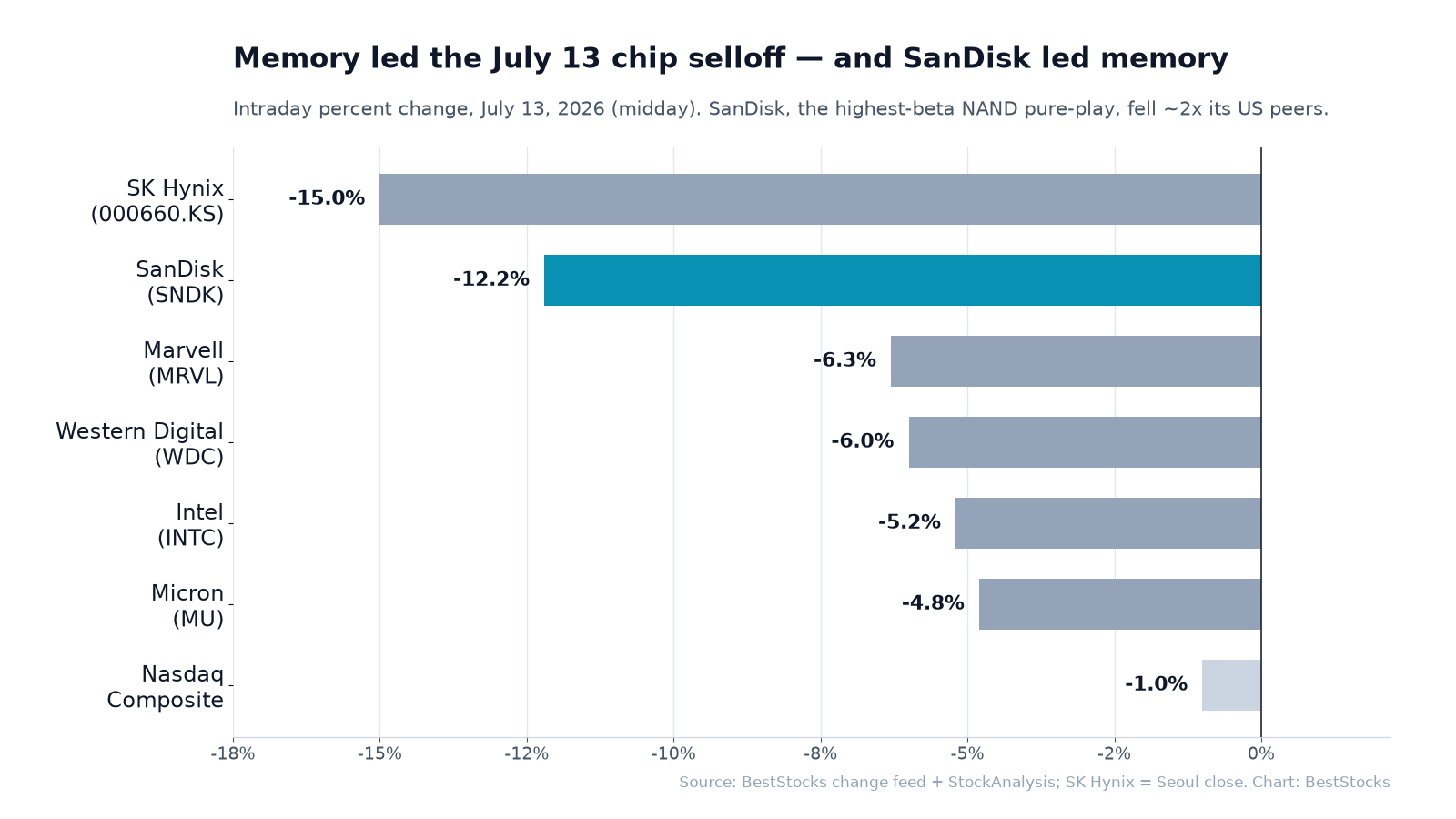

SNDK fell ~12% intraday to about $1,682 on July 13 in a two-part memory selloff — a US-Iran risk-off that hit all chips plus a record ~15% SK Hynix plunge on HBM4 worries. As the highest-beta NAND pure-play (up more than 30-fold since its 2025 WDC spin-off), SanDisk fell about twice its peers. No company-specific news.

Summary

SanDisk (NASDAQ: SNDK) tumbled on Monday, July 13, 2026, falling roughly 12% intraday to about $1,682 — down close to $234 from Friday's $1,915.92 close — as of 12:20 p.m. ET, with the session still open [1][2]. The drop had almost nothing to do with SanDisk's own fundamentals. It was a two-part memory-chip selloff: a broad, geopolitics-driven risk-off that produced a broad semiconductor decline, layered on top of a memory-specific shock after SK Hynix plunged a record ~15% in Seoul [4][5]. SanDisk — the highest-beta NAND pure-play, up more than 30-fold since its February 2025 spin-off from Western Digital (NASDAQ: WDC) — fell about twice as much as its memory peers, the classic behavior of one of the highest-beta, most-extended names on a de-risking day [6].

What changed

Two distinct catalysts hit the same session, and it helps to separate the macro leg from the memory-specific leg.

| Catalyst | What happened | Market effect |

|---|---|---|

| US-Iran escalation (macro) | US Central Command struck ~140 Iranian military sites over the weekend; Iran retaliated and declared the Strait of Hormuz closed, unwinding last month's interim agreement [5] | Oil about +4.5% (~$74.60 WTI); S&P 500 −0.4%, Nasdaq −1%; chips among the biggest losers on risk-off and supply-chain fears [5] |

| SK Hynix record −15% (memory-specific) | A Korea Investment & Securities (KIS) note pegged SK Hynix's Q2 operating profit near ₩6.04 trillion, ~8% below the ~₩6.5 trillion consensus, citing slower HBM4 shipment scaling and mix; profit-taking hit after a blistering pre-Nasdaq-debut rally [4] | SK Hynix's worst day on record; Korea's Kospi fell ~9% and briefly halted; Samsung and US memory names followed [4] |

The sequence inside the day matters. In pre-market trading, SanDisk was down about 6.5% — roughly in line with the broad chip move as memory peers Micron (NASDAQ: MU) and Western Digital slipped ~5% on the Iran headlines [5]. By midday the loss had roughly doubled to ~12%; the most likely read is that the memory-specific SK Hynix shock, more than the geopolitics, became the dominant driver — an inference from SanDisk's divergence from the broader chip tape, not a directly observed cause [1][4]. Either way, SanDisk detached from the broader semiconductor tape and fell far more than the sector's ~1-6% declines.

Why it matters

SanDisk is the purest way to play NAND flash on the US market, which is exactly why it moves like this. Western Digital's separation became effective on February 21, 2025 — distributing 80.1% of SanDisk to WDC holders and retaining 19.9% — with regular-way SNDK trading beginning February 24; the result was a stand-alone NAND company (SSDs, embedded storage, memory cards and USB drives, built on the long-running Kioxia joint venture) with no HDD ballast to dampen the memory cycle [6]. That focus is the whole bull case in an AI-storage supercycle, and it has worked spectacularly: the stock ranged from a 52-week low of $40.10 to a high of $2,354.39 — a roughly 59-fold span — on surging NAND pricing and AI-driven enterprise-SSD demand [2]. But the same purity cuts both ways. Worth noting: SK Hynix's problem was HBM/DRAM-specific, and SanDisk makes NAND — so the read-through is not direct product exposure but shared memory-sector sentiment, positioning and capital-cycle and valuation expectations. With no diversification, SanDisk amplifies every twist in that sentiment — and a record one-day drop at one of the world's largest memory makers is exactly the kind of twist that snaps a richly valued pure-play back hardest.

How the move compares

The peer tape is consistent with the memory-specific read. On the same session, the broad market fell about 1% while memory names led the semiconductor decline, and SanDisk led them.

| Stock / index | Jul 13 move (midday) | Note |

|---|---|---|

| SNDK — SanDisk | ~−12.2% | Highest-beta NAND pure-play; fell ~2x peers [1] |

| SK Hynix (000660.KS) | ~−15% | Seoul; the trigger — record one-day drop, Q2 estimate cut [4] |

| MRVL — Marvell | ~−6.3% | AI-chip peer; sector risk-off [9] |

| WDC — Western Digital | ~−6.0% | SanDisk's former parent (HDD) [9] |

| INTC — Intel | ~−5.2% | Broad AI/chip pullback [9] |

| MU — Micron | ~−4.8% | DRAM/HBM + NAND peer [9] |

| Nasdaq Composite | ~−1.0% | Broad market; risk-off on Iran [5] |

Seagate (STX) fell about 4.3% pre-market on the same headlines — a pre-market read, not directly comparable to the midday figures above [5]. The pattern — a ~1% index, ~5-6% for diversified chipmakers, and ~12% for the memory pure-play — is a textbook risk-off gradient: the more concentrated the exposure and the bigger the prior run, the harder the pullback.

What drove the SanDisk (SNDK) selloff on July 13, 2026?

SanDisk fell about 12% intraday to roughly $1,682 in a sector-wide memory-chip selloff, not because of any negative company-specific news [1]. Two forces hit at once: a geopolitical risk-off after the US struck ~140 Iranian sites and Iran moved to close the Strait of Hormuz, which sent oil up ~4-5% and drove a broad semiconductor decline; and a memory-specific shock as SK Hynix plunged a record ~15% in Seoul following a brokerage note that its Q2 operating profit would land ~8% below consensus on slower HBM4 shipment scaling [4][5]. As the highest-beta NAND-flash pure-play — one of the best-performing memory stocks of the past year, up more than 30-fold since its 2025 spin-off — SanDisk's intraday decline ran about twice as deep as peers like Micron and Western Digital, a textbook memory-chip selloff and semiconductor risk-off day.

SanDisk analyst price targets: where the Street stands

SanDisk went into the drop with an unusually bullish and fast-rising set of targets — a cluster of large hikes through late spring and early summer. Percentage gaps are measured against the ~$1,682 midday price on July 13.

| Firm | Date | Rating | Target (old → new) | Gap to ~$1,682 |

|---|---|---|---|---|

| Susquehanna | May 29 | Positive | $2,000 → $3,250 [10] | +93% |

| Sanford C. Bernstein | Jun 29 | Outperform | $1,700 → $3,000 [7] | +78% |

| Cantor Fitzgerald | Jun 8 | Overweight | $1,800 → $2,900 [7] | +72% |

| Bank of America | Jul 1 | Buy | $2,100 → $2,500 [7] | +49% |

| Citigroup | Jun 25 | Buy | $2,025 → $2,500 [7] | +49% |

| Barclays | May 26 | Overweight (upgrade) | → $2,300 [7] | +37% |

| Mizuho | Jun 8 | Outperform | $1,825 → $2,200 [7] | +31% |

| Morgan Stanley | Jun 3 | Overweight | $1,100 → $1,750 [7] | +4% |

| Consensus (~22 analysts) | Jul | Buy / Moderate Buy | ~$2,035 average [8] | +21% |

The takeaway: even after a ~12% drop, SanDisk trades below all eight recent targets shown here, and the most aggressive marks — Susquehanna's $3,250, Bernstein's $3,000 and Cantor's $2,900 — reflect analysts underwriting a NAND up-cycle that extends well into 2027 (and other firms hiked again in early-to-mid July, so this table is not exhaustive). The risk is that those targets were struck near the top of a euphoric memory rally, the same euphoria SK Hynix's estimate cut just called into question. Aggregators also carry far lower outliers (a $1,000 low at StockAnalysis, and MarketBeat's dataset reaches down to $235), so "below every target" would overstate it.

Was this a SanDisk-specific problem or a sector move?

It was a sector move, amplified by SanDisk's own beta. No negative SanDisk filing, earnings warning or company announcement was identified by 12:20 p.m. ET. The trigger came from a rival's numbers (SK Hynix's Q2 profit estimate) and a macro shock (US-Iran), and it propagated through the entire memory complex — SK Hynix and Samsung in Asia, then Micron, Western Digital, Seagate and SanDisk in the US [4][9]. One nuance matters: SK Hynix's shortfall was about HBM4/DRAM, not NAND, and SanDisk is a NAND maker — so the mechanism was not direct product read-through but a shared memory-sector repricing (sentiment, positioning, capital-cycle and valuation expectations). That SanDisk fell roughly twice as far as Micron or Western Digital is a function of its concentration and prior run, not new information about SanDisk's business.

The July 13 move in numbers

| Measure | Value | Note |

|---|---|---|

| SNDK price (midday) | ~$1,682 | ≈−12.2% (−$234); ~12:20 p.m. ET, Jul 13 [1][2] |

| Prior close, Fri Jul 10 | $1,915.92 | Reference close [2] |

| Intraday range | ~$1,676 – $1,800 | Session high $1,800; ongoing [2] |

| Volume (midday) | ~6-7M shares | vs ~16.4M average daily (MarketBeat) — not unusually heavy [3] |

| 52-week range | $40.10 – $2,354.39 | ≈59x low-to-high [2] |

| Market cap | ~$249B | 148.1M shares out [2][3] |

| P/E (trailing) | ~56.5x | Cyclical peak earnings [2] |

| Consensus target | ~$2,035 | ~22 analysts, Buy lean [8] |

SanDisk fair-value scenarios after the drop

The scenarios below are the author's hypothetical, illustrative estimates — editorial weights based on the NAND pricing cycle, AI-storage demand and where the Street's targets sit, not a DCF or a consensus model. Read the table as a target-anchored sentiment range rather than a bottom-up valuation: each price maps to cited Street inputs (the bear case to a pre-hike reference level), and the probabilities are judgment calls meant to frame the risk, not to price it precisely.

| Scenario | Price | Prob. | Key drivers |

|---|---|---|---|

| Bull | ~$2,900 | 30% | NAND up-cycle extends into 2027; AI enterprise-SSD demand and firm pricing hold; SK Hynix's HBM4 wobble proves a blip. Anchor: Susquehanna $3,250, Bernstein $3,000, Cantor $2,900 [10][7] |

| Base | ~$2,050 | 45% | Pricing stays firm but decelerates as the cycle normalizes; earnings power is real but no longer accelerating. Anchor: ~$2,035 Street consensus [8] |

| Bear | ~$1,150 | 25% | Memory cycle rolls over in the classic NAND boom-bust; pricing corrects and the ~56x multiple compresses. Anchor: Morgan Stanley's pre-hike $1,100 area [7] |

Probability-weighting those cases (0.30×$2,900 + 0.45×$2,050 + 0.25×$1,150) gives a probability-weighted scenario price — an illustrative midpoint, not a valuation-model output — near $2,080, roughly 24% above the ~$1,682 midday price, or equivalently, the stock trades about 19% below that midpoint after the drop. It is sensitive to the weights: shifting five percentage points from the bear case to the bull case moves the midpoint by only about $88 per share. The wide spread between the bull and bear anchors — $1,150 to $2,900 — is the real message: this is a deeply cyclical name at a peak-cycle multiple, so the discount the selloff opened is best read as compensation for NAND-cycle risk, not as a clean mispricing.

What SanDisk investors should watch next

First, NAND pricing: contract and spot price trends are the single biggest driver of SanDisk's earnings power; the SK Hynix estimate cut is best read as a memory-sector sentiment and valuation signal — it concerned HBM4 timing and mix, not direct evidence that SanDisk's NAND end-demand has weakened [4]. Second, SanDisk's own results and guidance: the company reports fiscal fourth-quarter and full-year 2026 results on August 5, 2026 and holds an Investor Day on August 13, 2026 — the next hard catalysts, which will show whether the double-digit NAND price increases analysts modeled are still intact [11]. Third, the SK Hynix and Samsung read-through: as the two largest memory makers, their HBM and NAND commentary sets the tone for the whole complex. Fourth, the US-Iran situation and oil: a prolonged Strait of Hormuz disruption raises input and freight costs across semiconductors [5]. Finally, volume and volatility: whether the selling broadens into higher-volume, multi-day distribution or stabilizes will show if this was a one-day beta unwind or the start of a cycle re-rating. For related sector context, see our Ultra Clean (UCTT) semiconductor-rally analysis, our SiTime (SITM) semiconductor-selloff explainer, and more market-mover breakdowns in the BestStocks research hub.

SanDisk (SNDK) stock-drop FAQ

Why did SanDisk stock drop on July 13, 2026?

SanDisk fell about 12% intraday to roughly $1,682 in a memory-chip sector selloff, not because of any negative company-specific news. SK Hynix plunged a record ~15% in Seoul after a brokerage note flagged Q2 operating profit about 8% below consensus on slower HBM4 shipment scaling, and a separate US-Iran escalation sent oil up ~4-5% and drove a broad semiconductor decline. As the highest-beta NAND pure-play, SanDisk fell about twice as much as peers like Micron and Western Digital.

Was there bad news from SanDisk itself?

No. SanDisk issued no earnings warning, guidance change, or announcement on July 13. The catalysts were external: a rival's earnings-estimate cut (SK Hynix) and a geopolitical shock (US-Iran). The move was a sector-wide de-risking amplified by SanDisk's concentration in NAND and its very large prior run.

Why did SanDisk fall so much more than Micron or Western Digital?

SanDisk is the purest NAND flash play on the US market and had risen more than 30-fold since its 2025 spin-off from Western Digital, making it the highest-beta, most-extended memory name. On a risk-off day the most concentrated and most-extended stock tends to fall hardest — hence ~12% for SanDisk versus ~5-6% for the more diversified chipmakers.

What is the analyst price target for SNDK?

Consensus was around $2,035 across roughly 22 analysts (S&P Global/StockAnalysis) with a Buy lean, and the most aggressive targets were far higher — Susquehanna $3,250, Bernstein $3,000, Cantor $2,900, and BofA and Citigroup at $2,500. Even after the drop, SanDisk traded below all eight recent targets in our table, though aggregators also carry lower outliers and those bullish marks were set during a euphoric memory rally.

Is SanDisk a memory pure-play?

Yes. When Western Digital split in February 2025, SanDisk became a stand-alone NAND flash company — SSDs, embedded storage, memory cards and USB drives, built on its Kioxia joint venture — with no hard-drive business to offset the memory cycle. That focus magnifies both the upside in an AI-storage boom and the downside on days like July 13.