Stock Analysis

Why Did Moderna (MRNA) Stock Drop 10.8% on July 10, 2026?

MRNA fell 10.83% to $68.27 on July 10 as JPMorgan reiterated Underweight and named it a Q3 short idea — a fresh catalyst on top of a week of below-market analyst targets and a no-minimum EU vaccine deal, after a 48% June rally. No negative clinical news.

Summary

Moderna (NASDAQ: MRNA) fell on Friday, July 10, 2026 for a reason that had nothing to do with a clinical failure: a fresh JPMorgan short call hit a stock that had run up roughly 48% in June and was trading well above most published analyst targets. The shares closed at $68.27, down $8.29 (−10.83%) from Thursday's $76.56 close, on turnover of about 9.2 million shares [1][2]. That JPMorgan note was the clearest new catalyst of the session, but it landed on a market that a week of cautious analyst actions and a no-minimum European vaccine framework had already cooled after a Monday, July 6 close of $81.80 — Moderna's highest finish since August 2024 [3][4]. The move was predominantly company-specific: vaccine peers and the sector barely moved.

What changed

The decline was the endpoint of several days of accumulating caution, capped by a fresh short recommendation on Friday. Only the JPMorgan call was new that session; the other three developments had already been weighing on sentiment.

| Date | Development | Detail |

|---|---|---|

| Mon, Jul 6 | Rally peaks | MRNA closes at $81.80, highest since Aug 2024, after a ~48% June advance [3] |

| Tue, Jul 7 | BofA — Underperform | Alec Stranahan raises target to $38 from $34; says the stock "overshot implied value from upcoming data readouts" [4] |

| Wed, Jul 8 | Morgan Stanley — Equal-weight | Lifts target to $39 from $33 — still ~43% below the eventual Friday close [5] |

| Thu, Jul 9 | EU framework, no minimum | European Commission signs a joint-procurement framework for up to 24M mRESVIA doses over four years, with no minimum purchase [4] |

| Fri, Jul 10 | JPMorgan — Underweight | Jessica Fye reiterates Underweight, names MRNA a Q3 short idea, calls its financial situation "precarious"; stock closes −10.83% at $68.27 [2][3] |

On Friday, JPMorgan's Jessica Fye reiterated an Underweight rating, added Moderna to the firm's third-quarter short-idea list, and described the company's financial situation as "precarious" as it works toward cash-flow breakeven [3]. The European framework, signed a day earlier at the request of six countries — Austria, Denmark, Ireland, Luxembourg, Norway and Portugal — permitted purchases of up to 24 million mRESVIA RSV doses over four years but committed to no minimum volume, and the Commission's announcement disclosed no dose price or aggregate contract value [4].

Why it matters

Moderna's 2026 recovery rests on converting a post-COVID cash drawdown into a diversified pipeline, so the market's willingness to capitalize that pipeline — and the company's ability to fund it — is the whole debate. June's advance was built on real data: five-year Phase 2b KEYNOTE-942 results for intismeran autogene (mRNA-4157/V940) with Merck's (NYSE: MRK) Keytruda, presented at ASCO on June 1. At a median 60.3 months of follow-up, the combination reduced the hazard of recurrence or death by 49% and the hazard of distant metastasis or death by 59% versus Keytruda alone in high-risk melanoma [8]. Later that month, on June 18, an FDA advisory committee voted 9–0 — in each of two age-group votes — that the benefits of the mRNA-1010 flu vaccine outweighed its risks [9]. Those are franchise-defining programs, but they are years from peak revenue, which is why financing matters now. The specifics behind JPMorgan's "precarious" framing are a real cash bridge, not just rhetoric.

How the move compares

Friday's slide was idiosyncratic. On the same session, vaccine peers barely moved: BioNTech (BNTX) fell 1.60% to $91.49 and Pfizer (PFE) slipped 0.33% to $24.17, while the S&P 500 health-care sector was down about 0.7% [2][10]. A 10.83% single-name drop against a sub-1% sector move indicates that company-specific factors — valuation and analyst commentary — were the dominant influence, not a group sell-off in mRNA or vaccine names.

Why did Moderna (MRNA) stock drop on July 10, 2026?

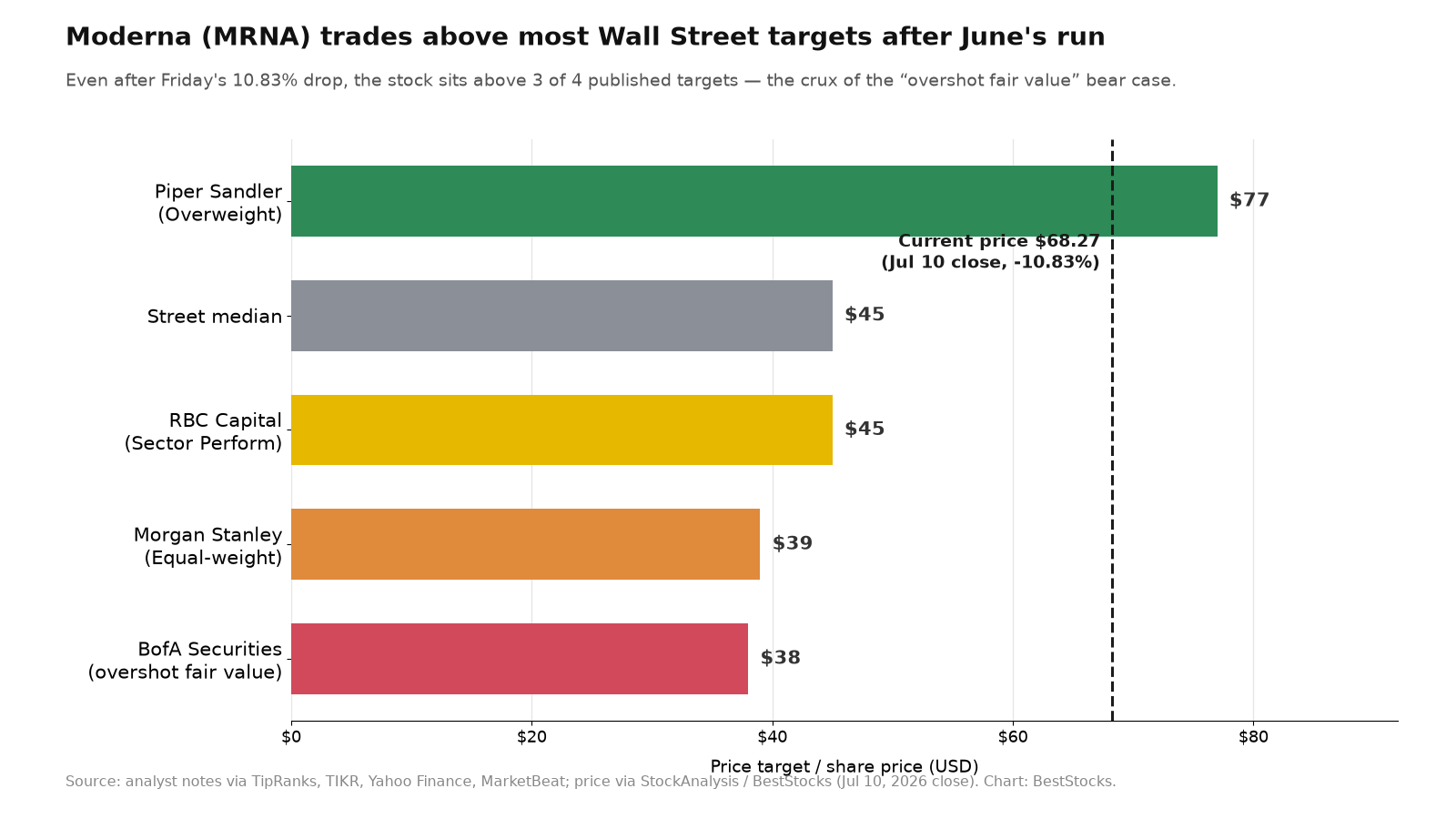

Moderna fell 10.83% to $68.27 because JPMorgan reiterated an Underweight rating, named the stock a third-quarter short idea, and flagged a "precarious" financial position — the fresh catalyst on a day when the shares were already vulnerable after a ~48% June rally [2][3]. There was no negative clinical news. The short call landed on top of a week of below-market analyst targets (BofA Underperform $38 on July 7; Morgan Stanley Equal-weight $39 on July 8) and a European vaccine framework signed without a minimum-purchase commitment (July 9), which together prompted holders to take profits after the run [4][5].

JPMorgan's short call and the week's analyst actions

The recent cluster of targets sits well below where MRNA traded, which is the crux of the valuation debate. Percentage gaps are measured against the $68.27 July 10 close.

| Firm | Date | Rating | Target | Gap to $68.27 |

|---|---|---|---|---|

| JPMorgan (J. Fye) | Jul 10 | Underweight (Q3 short idea) | — | Bearish call; no public target [3] |

| BofA (A. Stranahan) | Jul 7 | Underperform | $38 (from $34) | −44.3% [4] |

| Morgan Stanley | Jul 8 | Equal-weight | $39 (from $33) | −42.9% [5] |

| RBC Capital | Jul 7 | Sector Perform | $45 (from $38) | −34.1% [7] |

| Piper Sandler | Jun 26 | Overweight | $77 (from $69) | +12.8% [6] |

| Consensus (23 analysts) | Jul 8 | Hold-lean | $45 median / $47.89 avg (range $22–$79) | −34.1% (median) [6] |

Underweight is JPMorgan's formal rating; aggregators often translate it as "Sell." The pattern is telling: two firms raised their targets that week (BofA and Morgan Stanley), yet both kept below-market ratings, underscoring that even the more constructive revisions still sat 40%-plus beneath the price.

Why the EU mRESVIA agreement disappointed investors

On July 9, the European Commission signed a joint-procurement framework — at the request of Austria, Denmark, Ireland, Luxembourg, Norway and Portugal — giving those countries access to as many as 24 million doses of Moderna's mRESVIA RSV vaccine over as many as four years [4]. The disappointment was in the structure: it is a framework that sets terms for potential future orders, with no minimum purchase commitment, and the Commission's announcement disclosed no dose price or aggregate contract value. For a company trying to prove that its non-COVID vaccines can generate durable revenue, an agreement that guarantees no volume read as soft demand rather than a firm order.

The pipeline catalysts behind Moderna's June rally

The June advance was not sentiment alone. On June 1 at ASCO, Moderna and Merck presented five-year Phase 2b KEYNOTE-942 data for intismeran autogene (mRNA-4157/V940) plus Keytruda: at a median 60.3 months of follow-up, the combination cut the hazard of recurrence or death by 49% and the hazard of distant metastasis or death by 59% versus Keytruda alone in high-risk melanoma, with the results simultaneously published in the Journal of Clinical Oncology [8]. The confirmatory Phase 3 melanoma study, INTerpath-001, is already fully enrolled, so its readout — not the already-public Phase 2b data — is the next swing factor for the program. Separately, on June 18 an FDA advisory committee voted 9–0, in each of two age-group votes, that the mRNA-1010 flu vaccine's benefits outweighed its risks [9].

Moderna's cash position and patent-settlement exposure

JPMorgan's "precarious" label points to a specific cash bridge. Moderna reported roughly $7.5 billion of cash and investments at March 31, 2026 and guided to $4.5–$5.0 billion at year-end — but that decline includes a one-time legal outflow, so it should not be read entirely as recurring operating burn [4].

| Item | Amount | Note |

|---|---|---|

| Cash & investments, Mar 31 2026 | ~$7.5B | Starting balance [4] |

| Patent settlement (non-contingent) | −$950M | Payment due July 2026 [4] |

| Additional patent exposure (contingent) | up to −$1.3B | Depends on the appeal outcome [4] |

| Guided year-end 2026 cash | $4.5–$5.0B | Includes the one-time settlement, not just operating use [4] |

The point is not that Moderna is out of money — $4.5–$5.0 billion is a substantial cushion — but that a shrinking balance against a heavy pipeline-spend calendar leaves less margin for error, which is exactly the sensitivity a short-seller presses on after a large run.

How MRNA compared with BNTX, PFE and health-care stocks

| Stock / sector | Jul 10 move | Note |

|---|---|---|

| MRNA — Moderna | −10.83% ($68.27) | JPMorgan short call after a 48% June rally [2][3] |

| BNTX — BioNTech | −1.60% ($91.49) | mRNA vaccine peer; muted [10] |

| PFE — Pfizer | −0.33% ($24.17) | Vaccine/pharma peer; roughly flat [10] |

| S&P 500 health care | ~−0.7% | Broad sector barely lower [2] |

The divergence is the point: a 10.83% single-name drop against a sub-1% sector move shows the market was reacting to Moderna's own valuation and analyst commentary, not a sector-wide sell-off.

The July 10 move in numbers

| Measure | Value | Note |

|---|---|---|

| MRNA close, Fri Jul 10 | $68.27 | −$8.29 / −10.83%; 4:00 p.m. ET [2] |

| Prior close, Thu Jul 9 | $76.56 | Reference close [2] |

| Intraday range | $67.31 – $76.72 | StockAnalysis [2] |

| Volume | ~9.2M shares | Ordinary-to-slightly-elevated session [1][2] |

| 52-week range | $22.28 – $85.60 | StockAnalysis [2] |

| Market cap | ~$27.1B | Jul 10, 2026 [2] |

| Consensus target | $45 median / $47.89 avg | 23 analysts; range $22–$79 [6] |

MRNA analyst targets and fair-value scenarios

The scenarios below are the author's hypothetical, illustrative estimates — editorial scenario weights based on regulatory success, launch timing, cash depletion and settlement exposure, not a DCF or an analyst-consensus model. Each price is anchored to the cited inputs; the probabilities are judgment calls meant to frame the risk, not to price it precisely.

| Scenario | Price | Prob. | Key drivers |

|---|---|---|---|

| Bull | ~$80 | 25% | INTerpath-001 Phase 3 confirms a statistically significant, clinically meaningful recurrence-free-survival benefit consistent with Phase 2b; mRNA-1010 approval and launch; RSV orders convert. Anchor: Piper Sandler $77 OW; $79 Street high [6] |

| Base | ~$46 | 45% | Pipeline partly credited, but COVID/RSV revenue stays soft and cash use continues. Anchor: Street median $45 / $47.89 average; RBC $45 Sector Perform [6][7] |

| Bear | ~$35 | 30% | Data slips or financing/settlement pressure bites; the no-minimum EU framework signals soft demand. Anchor: BofA $38 Underperform; JPMorgan Underweight [3][4] |

Probability-weighting those cases (0.25×$80 + 0.45×$46 + 0.30×$35) gives a blended fair value near $51 — about 25% below the $68.27 close, or equivalently, the shares trade roughly 33% above that blended value. The result is sensitive to the weights: shifting five percentage points from the bear case to the bull case moves the blend by only about $2.25 per share, which is a reminder that these are subjective judgments, not a model output. Even after an 11% drop, the market is still paying up for optionality relative to where the Street models the business — the gap that defines the bear case, and one that narrows only if the melanoma and flu programs convert data into approvals and revenue.

What Moderna investors should watch next

First, INTerpath-001: the confirmatory Phase 3 melanoma readout for intismeran (V940) is the single biggest swing factor now that the five-year Phase 2b data are public [8]. Second, mRNA-1010: FDA action following the 9–0 advisory votes, and any label or recommendation detail [9]. Third, the cash trajectory: confirmation of the $4.5–$5.0B year-end guide and the patent-settlement appeal outcome [4]. Fourth, RSV traction: whether the EU framework converts into actual dose orders and disclosed pricing [4]. Finally, financing needs — any change in expected capital requirements as pipeline spend continues against a declining cash balance. For context on how a single analyst or clinical catalyst can swing a biotech, see our Ionis (IONS) trial-failure analysis and more market-mover explainers in the BestStocks research hub.

Moderna (MRNA) stock-drop FAQ

Why did Moderna stock drop on July 10, 2026?

Moderna fell 10.83% to $68.27 after JPMorgan reiterated an Underweight rating, named MRNA a third-quarter short idea, and called its financial situation 'precarious.' It was the clearest new catalyst of the session, landing on a stock that had run up about 48% in June and was already trading well above most published analyst targets. There was no negative clinical news.

Was there negative clinical or trial news behind the drop?

No. The decline was driven by valuation and financing concerns, not a clinical setback. Moderna's June rally was built on genuinely strong data — five-year Phase 2b KEYNOTE-942 melanoma results with Merck's Keytruda and a unanimous FDA advisory-committee vote for the mRNA-1010 flu vaccine — and none of that was reversed on July 10.

How did the move compare with vaccine peers and the sector?

It was stock-specific. On the same day, BioNTech fell 1.60%, Pfizer slipped 0.33%, and the S&P 500 health-care sector was down about 0.7%. A 10.83% single-name drop against a sub-1% sector move points to Moderna-specific factors — analyst caution and valuation — rather than a group sell-off.

What is the analyst price target for MRNA?

Consensus across 23 analysts was a $45 median and a $47.89 average, with a $22 low and a $79 high. The most recent marks were cautious and below the July 10 close: BofA $38 (Underperform), Morgan Stanley $39 (Equal-weight) and RBC $45 (Sector Perform), with Piper Sandler's $77 Overweight the notable bull.

What is Moderna's next major catalyst?

The confirmatory Phase 3 melanoma study, INTerpath-001, for intismeran (mRNA-4157/V940) is fully enrolled, and its readout is the biggest near-term swing factor now that the Phase 2b data are public. Investors are also watching FDA action on the mRNA-1010 flu vaccine after its 9-0 advisory votes, plus the year-end cash guide and the patent-settlement appeal.