Stock Analysis

Why did Alcoa (AA) stock fall ~6% on July 17, 2026 — a record Q2 that still missed, and an alumina guidance cut

Alcoa closed down 6.1% on July 17, 2026 — far more than its aluminum peers or the metal itself. Its Q2 set a revenue record and grew adjusted EPS more than fivefold, but it missed an elevated Street bar and cut full-year alumina guidance after cyclone-related outages at its Pinjarra refinery. The drop confirmed an aluminum-surplus bear case analysts had already been pricing in, and it layers dilution and integration questions from the pending South32 acquisition on top.

Summary

Alcoa (NYSE: AA) closed Friday, July 17, 2026 at $43.98, down $2.87, or 6.13%, from Thursday's $46.85 [1][2]. The BestStocks feed flagged the move but could not attribute it, reading it as "technical" with "no company-specific catalyst confirmed" [1]. There was a catalyst, and a clear one: after Thursday's close Alcoa reported second-quarter results that missed on both the top and bottom line and, more importantly, cut its full-year alumina guidance [4][5].

The nuance is that this was not a weak quarter in absolute terms. Revenue of $3.97 billion was a company record, up 31% year over year, and adjusted earnings of $2.12 a share were more than five times the year-ago $0.39 [4]. But it landed below an elevated bar — depending on the provider, the Street wanted roughly $2.25–$2.31 in adjusted EPS on just under $4 billion in revenue — and the guidance cut reinforced a bear case that analysts had already been pricing in for two weeks [5][7]. This was a "grow strongly year on year, miss the quarter, lower the outlook" print into a stock that had already fallen sharply from the low-$60s a month earlier [2].

| Evidence level | What can be said |

|---|---|

| Documented | AA closed −6.13% at $43.98 on Jul 17; Q2 revenue $3.97B (record) and adjusted EPS $2.12 both missed consensus (just under $4B revenue / roughly $2.25–$2.31 EPS, varying by provider); FY-2026 alumina production and shipment guidance was cut; the metal and aluminum peers barely moved that day [2][4][5]. |

| Reported interpretation | The selloff reflects a miss-plus-guidance-cut confirming an aluminum-surplus thesis that had already driven a wave of pre-earnings downgrades, layered on dilution and integration questions from the pending South32 acquisition [6][7]. |

| Author inference / not measurable | How much of the −6% is the earnings miss, how much the guidance cut, and how much continuation of the prior month's de-rating cannot be separated from a single day's tape. The probability-weighted value below is an illustrative estimate, not a forecast. |

What changed

| Metric | Value | As of / source |

|---|---|---|

| Closing price | $43.98 | Jul 17 2026, 4:00 p.m. ET — StockAnalysis [2] |

| Prior close (Jul 16) | $46.85 | StockAnalysis [2]; corroborated by BestStocks feed [1] |

| Day's change | −$2.87 / −6.13% | Vs prior close [1][2] |

| Day's range | $43.75 – $46.85 | Closed near the low [2] |

| 52-week range | $28.11 – $84.38 | Closed ~48% below the high [2] |

| Volume | ~11.7M sh | Vs a ~6.9M 20-day average — about 1.7× normal (StockAnalysis) [2][3] |

| Market cap | ~$11.6bn | 263.9M shares out; beta 1.63 [2][3] |

| Analyst targets | ~$51–$80 | Six most recent targets average ~$60 (median ~$54); broader consensus runs somewhat higher and lags [7][10][12] |

Participation was elevated but not a capitulation. Alcoa traded about 11.7 million shares against a ~6.9-million 20-day average — roughly 1.7× normal — elevated turnover rather than a thin drift, though not the multiples-of-average spike sometimes seen at a capitulation low (that read is interpretation, not a measured signal) [2][3]. (The BestStocks feed cited an even higher multiple, ~2.2×, against a shorter-window average; either way, turnover was well above trend [1].) The move also did not happen in a vacuum: AA had already de-rated from the low-$60s in mid-June, so Friday was the latest leg of a month-long decline, not a first crack [2].

The catalyst: a record quarter that still missed — and a guidance cut

Alcoa's Q2 was strong on almost every backward-looking line and disappointing on the two that the market cared about. Revenue of $3,966 million set a company record and rose from $3,193 million in Q1 and $3,018 million a year earlier; adjusted EBITDA jumped to $901 million from $595 million in Q1; and adjusted EPS of $2.12 compared with $1.40 in Q1 and just $0.39 a year ago [4]. Yet consensus had crept up into the low-$2.20s to low-$2.30s in adjusted EPS on just under $4 billion of revenue (the precise figures varied by provider — MarketBeat carried about $2.25 and ~$3.99B, other feeds nearer $2.31 and ~$4.06B), so the print was a modest miss on both — several cents on earnings and a low-single-digit percentage on the top line [5]. A record that undershoots an elevated bar is exactly the setup that produces a "sell the news" reaction — the same dynamic that met Intuitive Surgical's Q2 beat-but-soft-guidance print a day earlier, and the mirror image of the guidance-driven drop when IBM pre-warned on its quarter.

The forward-looking cut mattered more. Alcoa lowered its full-year 2026 alumina guidance — production to 9.5–9.6 million metric tons (down 0.2–0.3M) and shipments to 11.5–11.6 million tons (down 0.3–0.4M) — after instability at its Pinjarra, Australia refinery that began in late March was "further exacerbated by gas supply disruptions associated with Cyclone Narelle." The refinery has since stabilised, but the company said the second-quarter volume it lost will not be fully recovered [4]. Aluminum-segment guidance (2.4–2.6M tons of production, 2.6–2.8M of shipments) was left unchanged, but a downgrade to the alumina outlook feeds straight through Alcoa's high operating leverage [4]. It is worth noting the gap between adjusted EPS ($2.12) and GAAP EPS ($1.53): roughly $155 million of special items separated the two, a reminder to read the headline number with the adjustments in view [4].

Mostly a company-specific move, not an aluminum-price selloff

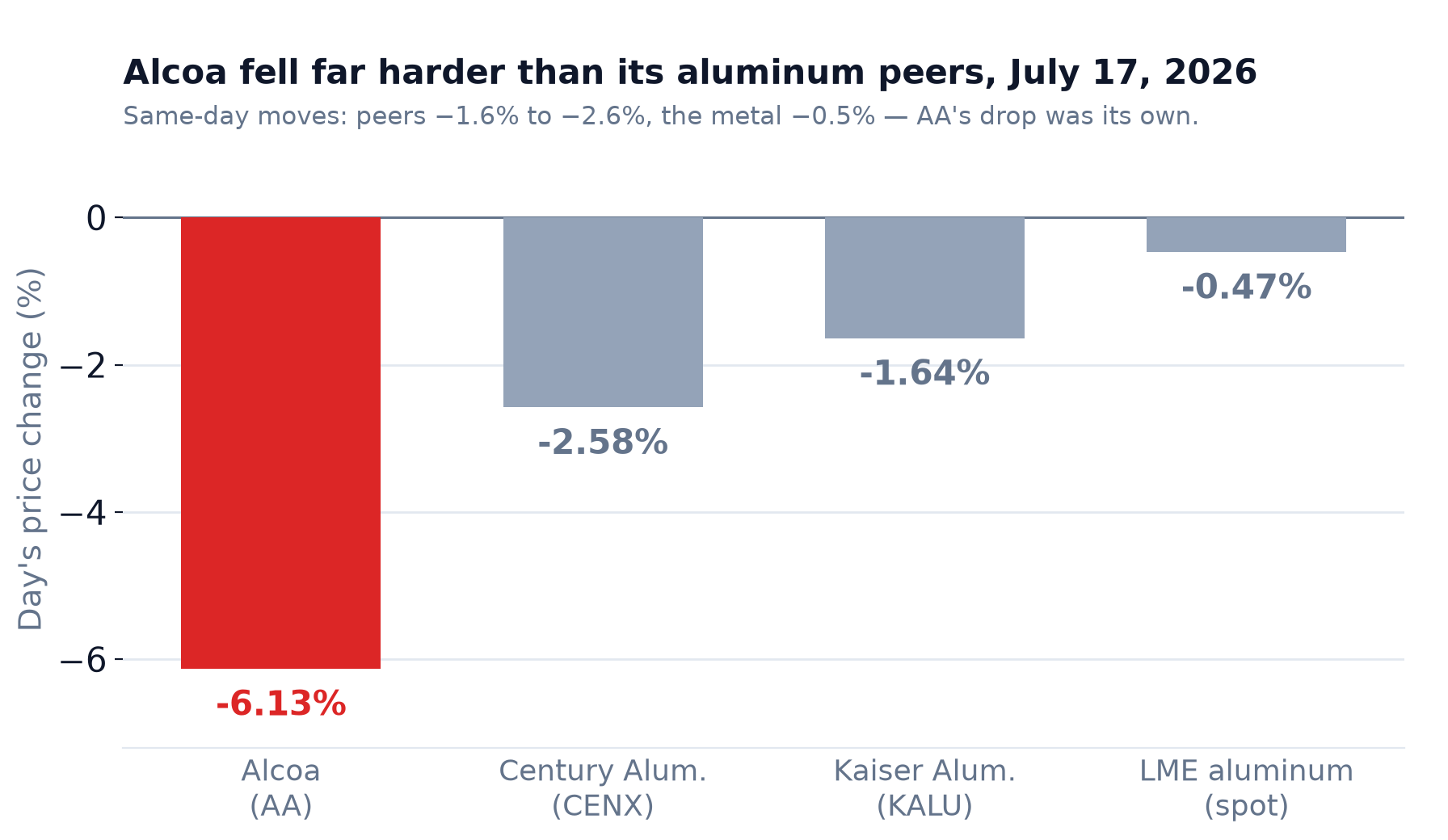

The cleanest way to see that Friday was about Alcoa, not the metal, is a same-day peer tape. If July 17 had been an aluminum-price event, Alcoa's smaller pure-play peers would have moved with it. They did not. Century Aluminum (CENX) fell 2.58% to $41.50 and Kaiser Aluminum (KALU) fell 1.64% to $157.78, while the LME aluminum price itself was down just 0.47% on the day [13][14][15]. Alcoa's 6.1% drop was roughly three to five percentage points deeper than any of them — the signature of a company-specific catalyst (the earnings miss and guidance cut) layered on a mildly negative sector day.

That said, the sector backdrop is not benign, and it is the reason the guidance cut stung. LME aluminum, though only fractionally lower on Friday, is down about 6.9% over the prior month, and Morgan Stanley's surplus call captures a real fear that new supply will cap prices into 2027–28 [6][15]. Alcoa is a commodity cyclical, so — much like the memory-price selloff that hit SanDisk — its shares ultimately live and die on a price deck outside management's control. Complicating the picture, the June 30 South32 acquisition — $4.1 billion of upfront cash-and-stock consideration ($3.1 billion cash plus about 17 million newly issued Alcoa shares worth ~$1 billion — roughly 6% of the enlarged share count), with a separate contingent payment of up to $750 million on top — is still pending and expected to close in the first half of 2027, so those shares have not yet been issued [16]. When it closes it would dilute existing holders — the kind of share-issuance overhang that has pressured names like AST SpaceMobile — and adds more exposure to the very market the bears are worried about. Strategically sensible in a tight market, the deal reads differently if surplus arrives, and at least one broker has already trimmed its target on the acquisition's valuation [17].

The analyst scorecard, one firm at a time

Because so much of the story is the pre-earnings de-rating, the individual calls matter. Each is a distinct action, not a lumped "analysts turned cautious":

| Firm (analyst) | Action | Rating | Date |

|---|---|---|---|

| B. Riley (Nick Giles) | $92 → $80 | Buy (kept) | Jul 7 [11] |

| Morgan Stanley (Carlos De Alba) | $79 → $53 | Overweight → Equal-Weight | Jul 8 [6] |

| Bank of America (Lawson Winder) | $57 → $51 | Underperform (kept) | Jul 9 [8] |

| JPMorgan (Bill Peterson) | $55 → $52 | Neutral (kept) | ~Jul 9 [9] |

| Wells Fargo (Timna Tanners) | $72 → $71 | Overweight (kept) | Jul 17, post-print [10] |

| BMO Capital (Katja Jancic) | $60 → $55 | Market Perform (kept) | Jul 17, post-print [12] |

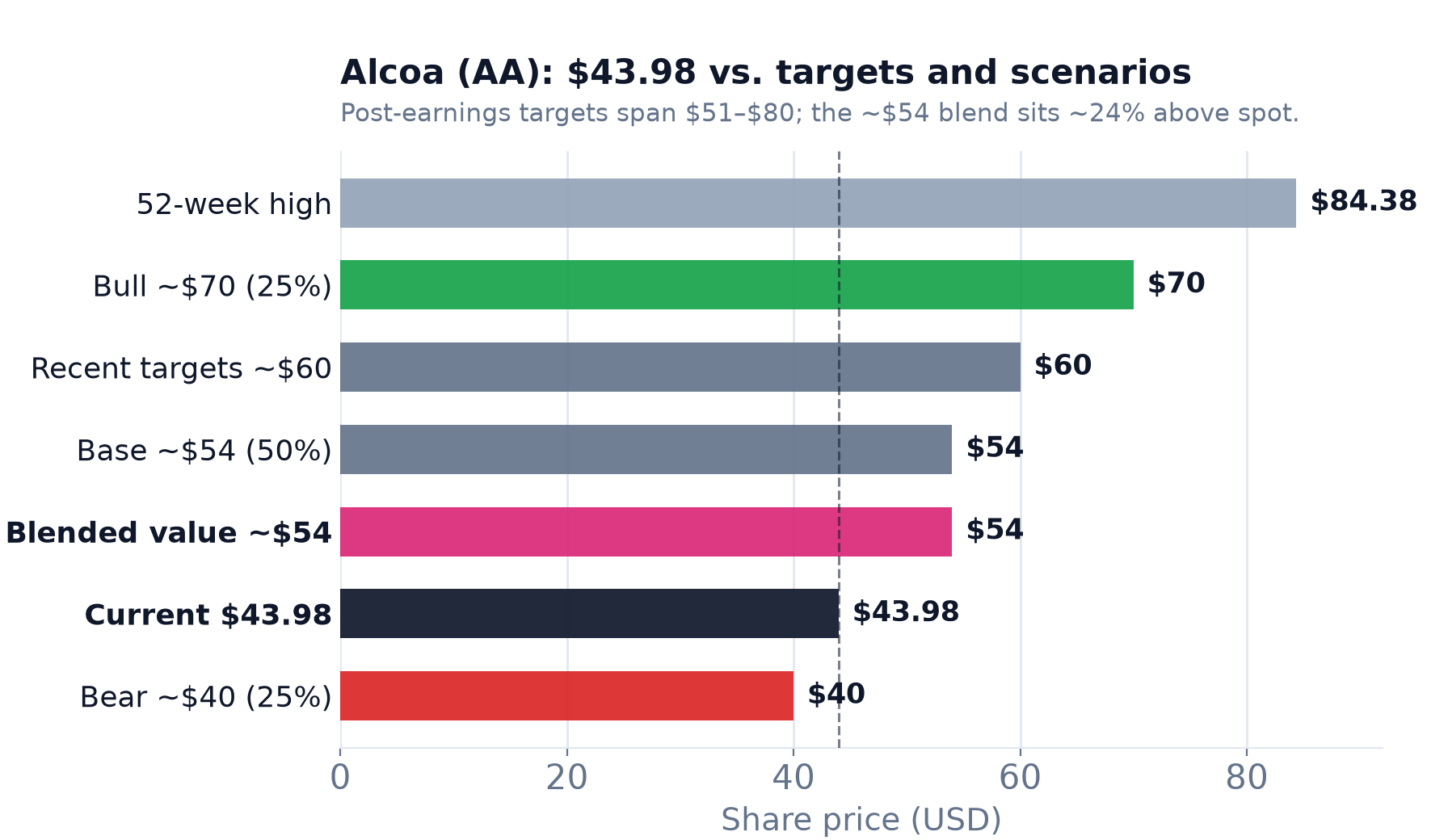

The spread is instructive. The bulls (B. Riley $80, Wells Fargo $71) still see substantial upside and view the selloff as an overreaction to a cyclical wobble; the bears (BofA $51, Morgan Stanley $53) frame it as the front edge of an aluminum-surplus down-cycle amplified by Alcoa's operating leverage. What none of these six recent calls does is put its target at or below Friday's $43.98 close — even BofA's $51, the lowest of them, is ~16% above spot [7][8]. That gap between price and even the most cautious targets is the crux of the setup.

What this means for value

Alcoa is a high-operating-leverage, commodity-cyclical producer, so its value swings on the aluminum and alumina price decks more than on any single quarter. The scenarios below are the author's own illustrative estimates, anchored to the recent analyst target distribution (a low of ~$51 to a high of ~$80 among the six most recent targets, average ~$60) and to whether the surplus thesis or the tight-market thesis wins — not the output of a formal model. They sum to 100%.

| Scenario | Price | Probability | Key driver |

|---|---|---|---|

| Bull | ~$70 | 25% | The tight-market camp is right: LME inventories stay low and a forecast global deficit keeps prices firm, Pinjarra normalizes, and South32's low-cost tonnes add accretive volume — a re-rate toward the Wells Fargo $71 / B. Riley $80 targets [11][15] |

| Base | ~$54 | 50% | Strong current earnings power persists, but the alumina guidance haircut, ~17M-share dilution and integration risk cap the multiple — converging on the post-earnings target cluster (BMO $55, Morgan Stanley $53, JPMorgan $52) [6][9][12] |

| Bear | ~$40 | 25% | Morgan Stanley's surplus arrives: new smelter supply pushes aluminum prices ~20% below consensus into 2027–28, Alcoa's leverage bites, and the stock drifts back toward the high-$30s and its 52-week-low zone [6] |

| Probability-weighted scenario value ≈ $54 (the inputs sum to ~$54.5, rounded to ~$54; an illustrative estimate, not an objective fair value) — the $43.98 close sits about 19% below it and ~27% below the ~$60 recent-target average, i.e. roughly +23% and +36% of implied upside, with the $40 bear only ~9% lower. | |||

Read the blend cautiously and mind the convention: "19% below the blend" describes the gap, which is not the same as expected upside (~23% from the current price to a ~$54 blend). At ~$54 the blend sits above the price, so on these assumptions Friday's selloff has pushed Alcoa below the author's illustrative scenario value — the reaction looks overdone if aluminum holds. But the bear case is only ~$4 below spot, which is the market's way of saying it is no longer treating a firm aluminum price as a given. The distance between the numbers — ~$44 today, ~$54 on a cautious blend, ~$60 on the recent-target average (with the broader, slower-moving consensus somewhat higher) — is the debate, and it resolves on the aluminum price deck and South32 integration, not on any single quarter. Treat the ~$54 figure as an illustrative probability-weighted scenario value, not a target or a model output.

What to watch

- The aluminum and alumina price decks — the single biggest swing factor between the scenarios. Watch LME aluminum (down ~6.9% over the prior month) and whether Morgan Stanley's surplus or the bulls' deficit view proves right into 2027 [6][15].

- Pinjarra's recovery — management says the lost Q2 volume can't be fully recovered; watch whether the refinery holds its restored run-rate and whether alumina guidance stabilizes or slips further [4].

- The South32 acquisition — the ~17M-share dilution, the cash outlay and the closing timeline; whether the added low-cost tonnage looks accretive or simply adds exposure to a softening market [16].

- Whether the multiple stabilizes — after a month-long slide from the low-$60s, watch whether AA holds the low-$40s or keeps de-rating toward the $28–$40 lower half of its 52-week range [2].

- Analyst dispersion — the six recent targets run from $51 to $80, an unusually wide spread; convergence in either direction after the print will signal which thesis is winning [7].

Frequently asked questions

Why did Alcoa (AA) stock fall on July 17, 2026?

Alcoa closed down 6.13% at $43.98 after reporting second-quarter results the prior evening. Although revenue of $3.97 billion was a company record and adjusted EPS of $2.12 was more than five times the year-ago figure, both missed consensus (just under $4 billion of revenue and roughly $2.25–$2.31 of adjusted EPS, depending on the provider), and Alcoa cut its full-year alumina guidance after cyclone-related outages at its Pinjarra refinery. The miss-plus-guidance-cut reinforced an aluminum-surplus bear case that analysts had already been pricing in, and the stock had been falling from the low-$60s for a month.

Did Alcoa beat or miss earnings in Q2 2026?

It missed on both lines relative to consensus, even though the absolute numbers grew sharply. Adjusted EPS of $2.12 came in below consensus estimates that ranged from about $2.25 (MarketBeat) to $2.31 (other feeds) — a miss of roughly $0.13–$0.19 — and revenue of $3.966 billion, while a company record, landed modestly below the Street's just-under-$4-billion estimate. GAAP diluted EPS was $1.53; the gap to the $2.12 adjusted figure reflects about $155 million of special items.

What was the alumina guidance cut about?

Alcoa lowered its full-year 2026 alumina production guidance to 9.5–9.6 million metric tons (down 0.2–0.3 million) and alumina shipments to 11.5–11.6 million tons (down 0.3–0.4 million). The reduction stems from instability at its Pinjarra, Australia refinery that began in late March and was worsened by gas-supply disruptions from Cyclone Narelle. Management said that although the refinery has since stabilised, the second-quarter volume it lost will not be fully recovered. Aluminum-segment guidance was left unchanged.

Did aluminum prices cause Alcoa's stock to fall?

No — the move was company-specific. On the same day, Century Aluminum fell 2.58% and Kaiser Aluminum fell 1.64%, while the LME aluminum price itself was down only 0.47%. Alcoa's 6.1% decline was three to five percentage points deeper than any of them, which points to the earnings miss and guidance cut rather than the metal price as the driver.

What did analysts do to their Alcoa price targets?

The de-rating started before earnings. On July 7 B. Riley cut its target to $80 from $92 (Buy); on July 8 Morgan Stanley downgraded AA to Equal-Weight from Overweight and slashed its target to $53 from $79 on an aluminum-surplus thesis; BofA cut to $51 (Underperform) and JPMorgan to $52 (Neutral) around July 9. After the print, Wells Fargo trimmed to $71 (Overweight) and BMO to $55 (Market Perform) on July 17. Even the lowest of these six, BofA's $51, sits above the $43.98 close, and the six most recent targets average about $60 (median ~$54); the broader, slower-moving consensus runs somewhat higher.

How does the South32 acquisition factor in?

On June 30, 2026, Alcoa agreed to buy South32's bauxite, alumina and aluminum assets in Australia, South Africa and Brazil for $4.1 billion of upfront consideration — $3.1 billion in cash plus roughly 17 million newly issued Alcoa shares worth about $1 billion — with a separate contingent payment of up to $750 million on top. The deal is still pending (expected to close in the first half of 2027), so the shares — about 6% of the enlarged share count — have not yet been issued; when it closes it would dilute existing shareholders and add more exposure to the aluminum market just as some analysts warn of a coming surplus, so while it strengthens Alcoa's low-cost asset base, it also amplifies the price-cycle risk the market is worried about — one broker has already trimmed its target citing the deal's valuation.

Is Alcoa stock cheap after the July 2026 drop?

It depends on your view of the aluminum price cycle. At $43.98 the stock trades about 27% below the ~$60 average of its six most recent analyst targets — and below even the lowest of them, BofA's $51. On the author's illustrative probability-weighted scenario value (bull ~$70 at 25%, base ~$54 at 50%, bear ~$40 at 25%, blended ~$54), the price sits roughly 19% below that blend — implying the selloff may be overdone if aluminum prices hold — but only about 9% above the bear case, which assumes the surplus arrives. These figures are illustrative descriptive analysis, not investment advice.