Stock Analysis

Why did Bloom Energy (BE) stock plunge ~14% on July 16, 2026 — despite a $1.7B AI-power deal?

Bloom Energy dropped about 14% intraday on the same day IDF and Oaktree announced a $1.7 billion project financing to power Nebius's AI build-out. The move reads as 'sell the news' — profit-taking on a stock priced north of 250x EV/EBITDA, a fuel-cell-complex derating (FCEL −16%), and a broad AI-capex risk-off — with a thinly-detailed deal and the prior week's short-seller overhang in the background.

Summary

Bloom Energy (NYSE: BE) was trading around $205.89 mid-afternoon Thursday, July 16, 2026, down about $33.49, or 13.99%, from Wednesday's $239.38 close, with the session still open [1][2]. The oddity is the timing: the fall came on a day Bloom announced good news. Before the open, Industrial Development Funding (IDF) and Oaktree announced a $1.7 billion project investment to deploy Bloom's fuel cells as behind-the-meter power for Nebius's AI cloud build-out [4][5]. The stock dropped anyway [6].

The price action reads as a "sell the news" reaction rather than a response to bad news — though public data cannot isolate what motivated sellers. Several forces plausibly overlapped: profit-taking in a stock that had run from a 52-week low near $24 to above $351 before this pullback; a broad, AI-capex-skepticism risk-off tape that pressured the whole momentum-growth cohort; and a fuel-cell-sector derating in which every name fell, the biggest winners hardest. The financing itself may not have helped much, because it disclosed little in the way of hard economics — more on that below. A short-seller episode from the prior week left sentiment fragile, but that was a week earlier, not the day's trigger. The tell is that shares never traded green: even the session's intraday high of $229.98 sat below Wednesday's $239.38 close [2].

| Evidence level | What can be said |

|---|---|

| Documented | Bloom announced a $1.7bn IDF/Oaktree-led project financing for Nebius AI power on Jul 16; the stock fell ~14% the same session and never traded above the prior close [2][4]. |

| Mechanically plausible | A high-beta name that had run up many-fold off its lows sold off on profit-taking, inside a broad AI-capex risk-off day, alongside its entire fuel-cell peer group. |

| Not measurable from public data | How much of the ~14% came from sell-the-news, the sector risk-off, or the lingering short-seller overhang — the split cannot be quantified. |

The sequence — why a good headline produced a red day

- Wed–Thu, Jul 8–9 (the prior week): short-sellers Hunterbrook (Jul 8) and Crossroads Capital (Jul 9) published reports questioning Bloom's scandium supply chain; the stock fell ~12% at its intraday trough, then pared the loss after Bloom rebutted the claims in a July 9 8-K, closing only marginally higher [13]. Context, not the July 16 catalyst.

- Thu, Jul 16 (pre-open): IDF and Oaktree announce a $1.7 billion project investment to deploy Bloom fuel cells for Nebius's AI infrastructure [4].

- Thu, Jul 16 (session): the stock opens at $228.30 — already down 4.6% — then falls a further ~10% intraday to about $205.89; the decline builds through the session, and the day's high ($229.98) never regains the $239.38 prior close [2].

What changed

| Metric | Value | As of / source |

|---|---|---|

| Intraday price | ~$205.89 | Jul 16 2026, ~2:01 p.m. ET — StockAnalysis [2] |

| Prior close (Jul 15) | $239.38 | StockAnalysis [2] |

| Intraday change | −$33.49 / −13.99% | Vs prior close; session ongoing [2] |

| Open / intraday range | $228.30 · $204.93–$229.98 | Opened −4.6%; the high never regained the prior close [2] |

| 52-week range | $24.04 – $351.28 | ~41% below the 52-week high [2] |

| Volume by ~2:01 p.m. | ~10.96M sh | ~75% of the 20-day average (~14.55M) with ~two-thirds of the session elapsed — a broadly normal pace [2][3] |

| Short interest | 19.35M sh | 6.93% of float — moderate [3] |

| Market cap | ~$58.6bn | Vs ~$68.1bn at the prior close; 284.44M shares [2][3] |

Two things frame the move. First, volume: by mid-afternoon Bloom had traded about 10.96 million shares — roughly 75% of its full 20-day average with about two-thirds of the session elapsed, i.e. a broadly normal daily pace [2][3]. That is telling in itself: this was neither the light turnover of quiet profit-taking nor a multiples-of-average capitulation. Second, positioning: short interest is a moderate 6.93% of the float — not the crowded-short setup that can amplify a move, so a squeeze or a short-driven cascade is not the story here [3].

The deal that did not save the day

The structure is concrete. Industrial Development Funding (IDF) and Oaktree announced a $1.7 billion project investment to deploy Bloom Energy fuel cells as behind-the-meter power for Nebius's AI cloud infrastructure — a figure supported by several parties, not funded by the two of them alone. IDF is the lead developer with primary equity and Oaktree holds minority equity; Morgan Stanley was the sole tax-equity investor and placement agent, and MUFG Bank provided the senior debt [4]. The announcement frames it as extending an IDF–Bloom collaboration to more than $2.6 billion of Bloom projects, and Chief Commercial Officer Aman Joshi tied it to the bottleneck of the moment: AI customers "need a path to finance and deploy power rapidly" [4][5].

On its face that is a supportive data point — third-party capital and a named AI customer attached to Bloom's fuel-cell thesis. But what the announcement did not disclose is as notable as what it did. It put no number on the project's power capacity, no locations, no deployment timetable, and no figures for Bloom's own revenue, margin, cash-flow impact, or how it affects the reported backlog [4]. Without those economics, a $1.7 billion project-finance headline cannot be translated directly into equity value for Bloom — which is a large part of why a seemingly positive release did little to support the shares.

The market had, in any case, already priced much of the AI-power thesis in. Bloom entered the day near a $68 billion market value (about $58.6 billion after the fall) on roughly breakeven earnings, at a multiple north of 250× EV/EBITDA and a forward price/sales in the mid-teens [2][3]. When expectations are that high, an underspecified financing is an easy occasion to take profits — the pattern the tape called "sell the news", and the same dynamic that hit AST SpaceMobile the same morning, where a $1 billion capital raise structured to reduce dilution was still sold hard [7].

It was not just Bloom — the whole complex derated

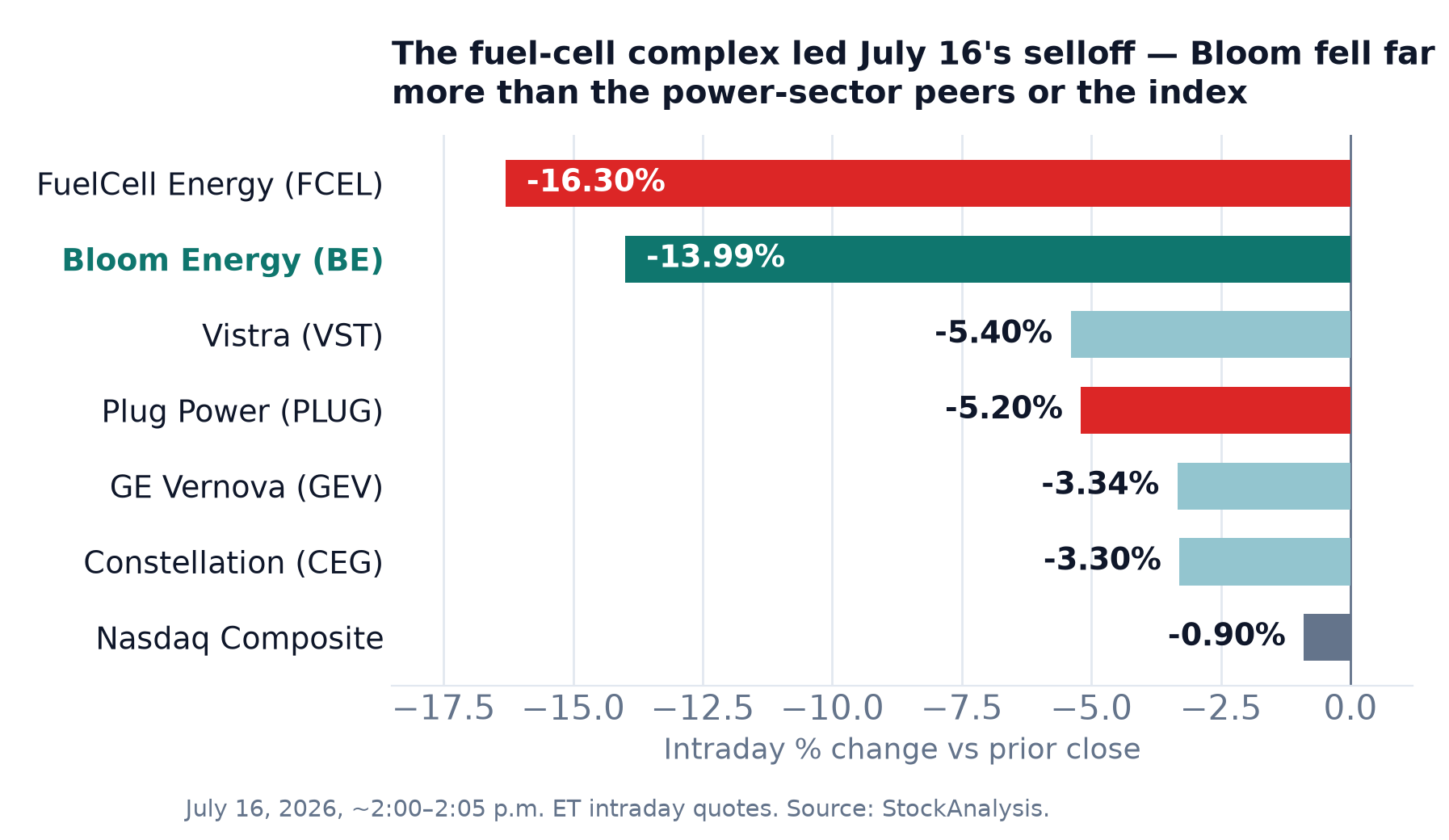

The single most useful context is the peer tape. This was a poor day to own anything in the AI-power momentum trade, and a worse one to own fuel cells specifically. FuelCell Energy (FCEL) fell 16.30% and Plug Power (PLUG) 5.20% — Bloom's closest listed fuel-cell peers, with no obvious fresh company-specific catalyst in the sources reviewed [14][15]. The power producers and grid/equipment names fell less: Vistra −5.40%, GE Vernova −3.34%, Constellation Energy −3.30% [16][17][18]. And the index barely moved — the Nasdaq Composite was down about 0.9% — on a second day of chip-sector weakness and AI-capex-slowdown skepticism, with money reported to be rotating out of high-beta growth [8].

That dispersion is the argument. A one-day cross-section cannot prove which factor dominated, but Bloom moving with FuelCell Energy — which had no financing of its own — while the power producers fell far less is consistent with a sector-wide derating of the most speculative, highest-multiple end of the AI-power trade as the major contributor, with a Bloom-specific reaction layered on top.

The short-seller overhang — a week old, not today's story

One thing this drop is not: a fresh reaction to the scandium short reports. Those landed the prior week. On July 8, Hunterbrook argued Bloom understates its reliance on Chinese-sourced scandium — a key material in its solid-oxide fuel cells — and questioned its supply-chain and backlog claims; Crossroads Capital followed on July 9. The stock sold off sharply (down roughly 12% at the intraday trough) before Bloom rebutted the allegations in a July 9 8-K, affirming it is "not dependent on China" and has visibility to support up to 25 GW of annual production. Shares bounced intraday on the rebuttal but closed only marginally higher, so the episode left a scar rather than a clean recovery [13]. It matters here only as an overhang — fragile sentiment that gave profit-takers a quick reason to act — not as the July 16 catalyst, which was a financing announcement into a risk-off tape.

Analyst view

The most defensible reading is that several forces overlapped rather than one clean cause. A broad AI-capex risk-off pressured the whole momentum cohort; the fuel-cell complex derated as a group; and the price action is consistent with a "sell the news" reaction to a financing that added little the market did not already expect — but their relative contributions cannot be separated from public intraday data. Two observations are on firmer ground. First, participation was roughly normal — about three-quarters of a full day's average with two-thirds of the session gone — neither the light turnover of quiet profit-taking nor a multiples-of-average capitulation. Second, the peer tape: Bloom fell far more than the power producers and grid names (Vistra, GE Vernova, Constellation, all down 3–5%) and roughly in line with its fuel-cell peer FuelCell Energy — which suggests sector-wide pressure was a major contributor, layered with a Bloom-specific reaction, rather than a company-specific rupture [2][14].

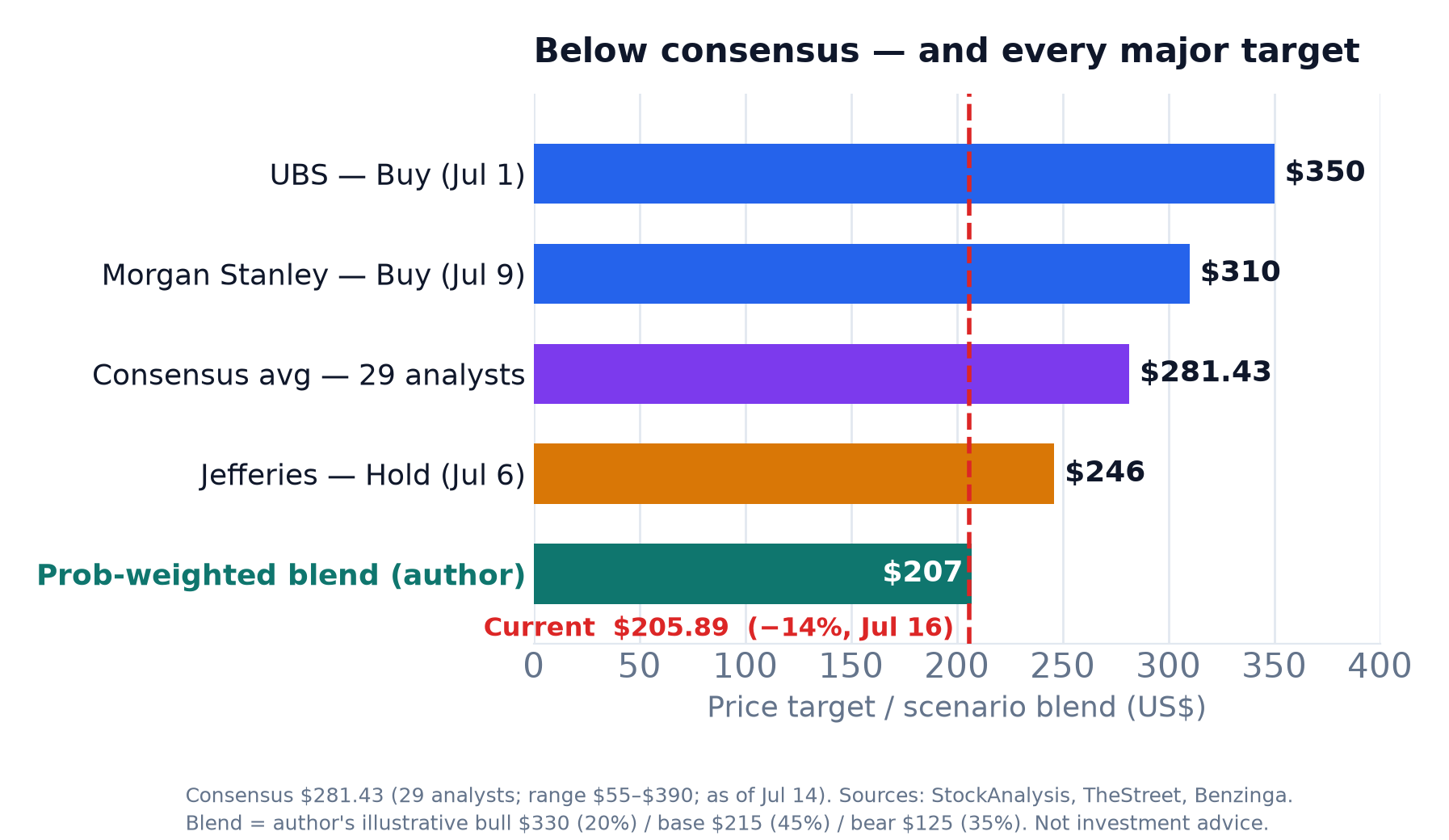

What this means for value: after the drop, Bloom trades around $206 — roughly 27% below the Street's $281 average target, and below every major published target (UBS $350, Morgan Stanley $310, Jefferies $246) [9][10][12]. On the sell-side's numbers, that looks like upside; on the author's more cautious probability-weighted blend (~$207, below), the stock sits about in line with fair value. The gap between price and target is the debate in one number: the market is pricing the short-seller overhang, execution risk and a rich multiple more heavily than analysts are. Which side is right turns on demand durability and clean-supply-chain disclosure — questions the coming quarters, not this financing, will answer.

What this means for value

Bloom is only marginally profitable on a trailing basis (EPS ~$0.02), so a P/E frame is close to meaningless; the scenario prices below are the author's own illustrative estimates, anchored to the published analyst target distribution and to how durable the AI-power demand narrative proves — not derived from an earnings or cash-flow model [3]. As of mid-July the consensus rating is Buy, with an average target of $281.43 across 29 analysts and a very wide range of $55 to $390 (StockAnalysis, as of July 14) [12]. Individual notes span that gap: UBS reiterated Buy at $350 and told clients to "buy the dip"; Morgan Stanley reiterated Buy at $310; Jefferies lifted its target to $246 from $207 but kept a Hold on the improved EBITDA outlook [9][10][11]. At ~$206, the stock trades below all of them. The probabilities below are the author's illustrative estimates, deliberately more cautious than the Street, and sum to 100%.

| Scenario | Price | Probability | Key driver |

|---|---|---|---|

| Bull | ~$330 | 20% | AI-power demand keeps compounding, behind-the-meter deals like Nebius scale and convert the backlog, and the scandium/supply concerns prove overblown; toward the Morgan Stanley $310 and UBS $350 targets [9][10] |

| Base | ~$215 | 45% | The financing model works and projects close, but margins and execution stay uncertain and the rich multiple only partly holds — deliberately below the $281 Street consensus [11][12] |

| Bear | ~$125 | 35% | AI-capex enthusiasm cools, the short-sellers' supply-chain/margin concerns partly bite, and a multiple north of 250× EV/EBITDA compresses on a barely-profitable name; roughly a 40% de-rate from here, still above the Street's $55 low [3][12][13] |

| Probability-weighted value ≈ $207 — essentially in line with the ~$205.89 price, but about 27% below the Street's $281.43 average target. | |||

Under these illustrative assumptions the blended value sits almost exactly on the price — read that as the sell-off having removed the froth from a stock that had run up many-fold off its lows, not as a bargain being created. It also sits about 27% below the Street's average target, so the sell-side is markedly more optimistic than this scenario mix. The blend is dominated by two binary questions the next few quarters will answer: whether AI-power demand keeps converting into signed, financed projects like Nebius, and whether the scandium/supply-chain critique proves noise or signal. Treat the ~$207 figure as an illustrative probability-weighted value — the midpoint of a wide $125–$330 distribution driven by those outcomes — not a target or a model-derived fair value.

What to watch

- Q2 earnings on July 28, 2026 (after the close) — the first read on whether the AI-power order book and margins are tracking the valuation; the single biggest swing factor between the scenarios [3].

- Follow-through on behind-the-meter financings — whether more Nebius-style, third-party-funded deals get signed, and whether future ones disclose capacity, margins and backlog impact; each converts the thesis from narrative into contracted, quantified revenue [4].

- The scandium / supply-chain question — any independent corroboration or refutation of the short-sellers' claims, and Bloom's own sourcing disclosures; this is the overhang that turns the bear case on or off [13].

- The fuel-cell and AI-power complex — whether GE Vernova, Constellation and the broader AI-capex tape stabilise or keep derating; Bloom is a high-beta bet on that whole trade, not an idiosyncratic story [8][16].

Frequently asked questions

Why did Bloom Energy (BE) stock fall on July 16, 2026?

Bloom fell about 14% to roughly $205.89 intraday even though, before the open, IDF and Oaktree announced a $1.7 billion project financing to deploy Bloom fuel cells for Nebius's AI infrastructure. The price action reads as 'sell the news': profit-taking in a stock priced north of 250x EV/EBITDA that had run up many-fold off its lows, a broad AI-capex risk-off day that hit the whole momentum-growth cohort, and a fuel-cell-sector derating in which FuelCell Energy fell 16% and Plug Power 5% with no news of their own. The stock never traded green — it opened down 4.6% and its intraday high stayed below the prior close.

Didn't Bloom just announce good news? Why did that make the stock drop?

The $1.7 billion IDF/Oaktree project financing is a genuine positive, with third-party capital and a named AI customer. But the announcement disclosed no hard economics — no capacity, locations, timetable, or Bloom revenue, margin or backlog impact — so a project-finance headline cannot translate directly into equity value. And the market had already priced much of the thesis in: at a multiple north of 250x EV/EBITDA on roughly breakeven earnings, an underspecified deal is an easy occasion to take profits.

Was the July 16 drop caused by the scandium short-seller reports?

No — those reports (from Hunterbrook on July 8 and Crossroads Capital on July 9) came the prior week, when the stock fell about 12% at its trough before Bloom rebutted them in a July 9 8-K; shares bounced intraday but closed only marginally higher. That episode left an overhang that made sentiment fragile, but the July 16 catalyst was the financing announcement and a broad risk-off tape, not a fresh short report. Conflating the two would be a timing error.

Was the sell-off specific to Bloom or a whole-sector move?

Mostly a sector move with a Bloom-specific layer. On July 16 the entire fuel-cell and AI-power complex derated: FuelCell Energy −16.3%, Plug Power −5.2%, Vistra −5.4%, GE Vernova −3.3%, Constellation −3.3%, while the Nasdaq Composite fell only ~0.9%. Bloom fell hardest among the large names because it combined the sector derating with its own sell-the-news reaction to the deal.

What are analysts saying about Bloom Energy, and is it cheap after the drop?

The consensus rating is Buy with an average target of $281.43 across 29 analysts (a wide $55–$390 range, StockAnalysis as of July 14) — so at ~$206 the stock trades about 27% below the Street's average target, with bulls far higher (UBS $350, Morgan Stanley $310) and Jefferies at a $246 Hold. Under the author's deliberately cautious scenarios (bull $330 / base $215 / bear $125), the probability-weighted value is about $207 — roughly in line with the price. So the drop removed the froth without making the stock obviously cheap on a cautious view, even as the sell-side still sees upside. These figures are descriptive analysis, not investment advice.