Stock Analysis

Why Did Applied Optoelectronics (AAOI) Stock Jump ~11% on July 14, 2026?

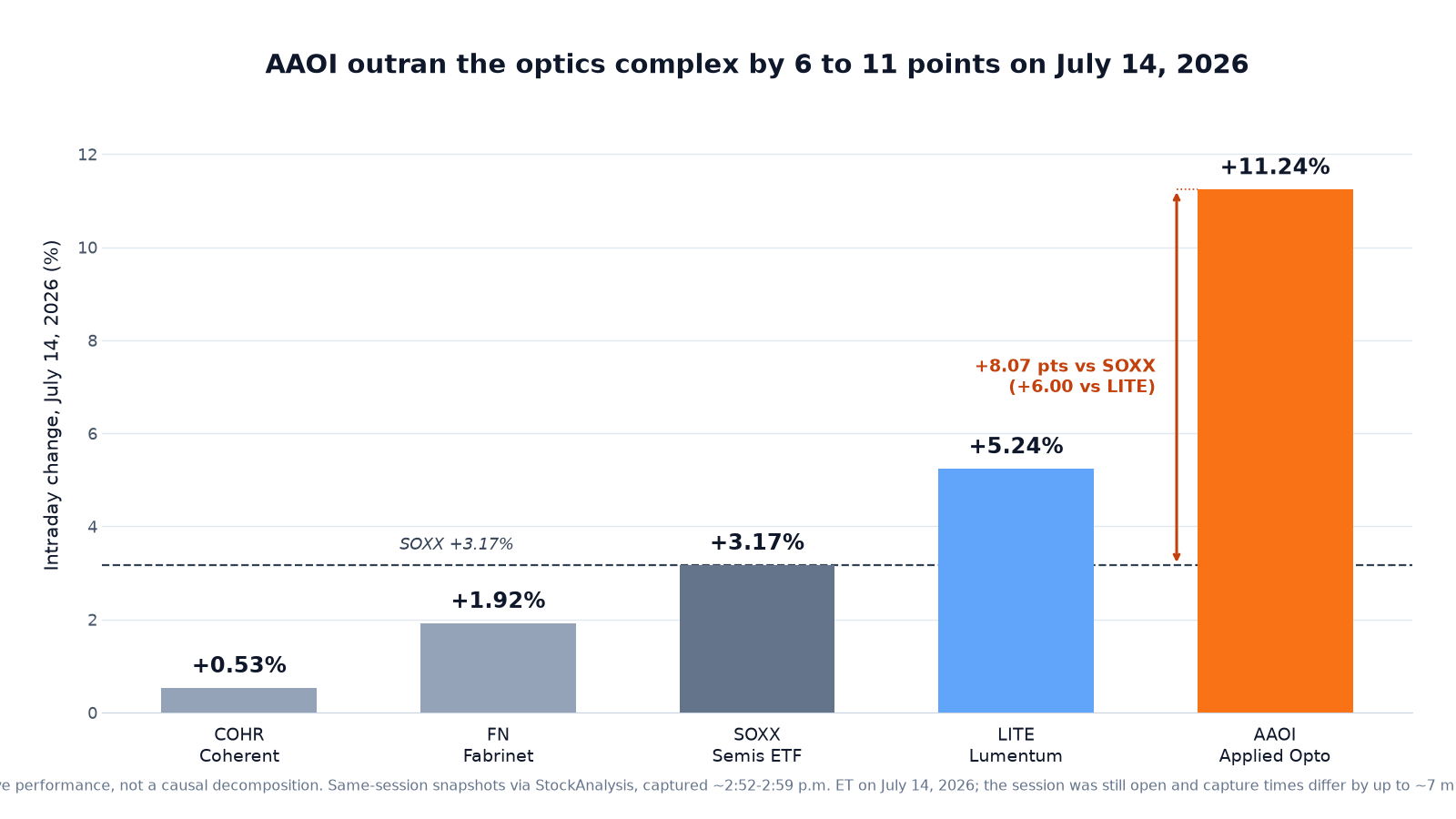

Applied Optoelectronics rose ~11% to about $124 on July 14 after announcing it had begun construction on a nearly 400,000 sq ft Pearland, Texas expansion for 800G and 1.6T transceivers. But AOI announced that expansion on April 17 — same buildings, same products, same AI rationale, plus a 700,000-units-per-month target for end-2027. The principal new fact was that construction had started. AAOI outran a firm optics tape by roughly 6 to 11 points.

Summary

Applied Optoelectronics (NASDAQ: AAOI) rose about 11.24% to roughly $124.46 on Tuesday, July 14, 2026 — up $12.58 from Monday's $111.88 close — as of 2:57 p.m. ET, with the session still open [1][2]. The trigger was a 7:00 a.m. ET release announcing that AOI has begun construction on two adjacent properties in Pearland, Texas, adding nearly 400,000 square feet of capacity for 800G and 1.6T optical transceivers [4]. The detail that reframes the day: AOI announced this expansion in April. On April 17 the company published a release headlined "AOI Expands Its Houston-Area Footprint to 900,000 Square Feet," which named the same buildings, the same 800G and 1.6T products, the same AI-infrastructure rationale, and a target of up to 700,000 units per month by the end of 2027 [6]. Tuesday's release adds one operational fact — construction has started — and no new financial detail [4]. Meanwhile the whole optics complex was higher. In one sentence: this was a construction-start update on a fully pre-announced project, in a name that outran its sector by roughly 6 to 11 points depending on the benchmark. The rest of this piece tests what could account for that gap.

What changed

Three disclosures describe this project. Setting them in sequence shows how little arrived on Tuesday.

| Date | Disclosure | What it established |

|---|---|---|

| Apr 7 agreement; 8-K filed Apr 13 | The transaction [5] | Purchase agreement for 14621 Kirby Drive and 11555 N. Spectrum Boulevard — ~388,133 sq ft for $58,428,612, closing April 17. Intended use given only as "office, warehouse, manufacturing, and assembly purposes" |

| Apr 17, 7:00 a.m. ET | The strategy [6] | The same two buildings, ~388,000 sq ft, lifting the Houston-area footprint to 900,000 sq ft; explicitly for 800G and 1.6T transceivers and AI data centers; capacity target of up to 700,000 units per month by end-2027; laser-fabrication capacity to rise ~350% by end-2027 |

| Jul 14, 7:00 a.m. ET | The milestone [4] | Construction has begun. Same addresses, same "nearly 400,000 square feet," same products, same AI framing. No capital budget, no completion date, no new capacity or revenue figure |

The April 17 release is the one that matters, and it is emphatic about its own lack of novelty. Chief financial officer Stefan Murry said then: "This expansion is aligned with the 2027 capacity targets we outlined on our most recent earnings call" [6]. So the strategy predates even April. Founder and chief executive Thompson Lin added that "the demand for optical connectivity in data centers has exceeded our expectations" [6]. By July 14, the products, the footprint, the unit target, the 2027 deadline and the AI rationale were all on the record. What Tuesday supplied was a groundbreaking — a genuine execution milestone, and the principal fact in the release that was not already public. The second quote in it is from Pearland's mayor, Quentin Wiltz, welcoming the jobs [4], which is a fair signal of the intended audience.

How the move compares

AOI did not move alone. Optical-connectivity names have been trading against an established AI-optics narrative, one reinforced by earlier public comments from Nvidia's Jensen Huang framing optical suppliers as central to the next phase of the buildout [9]. That narrative is context rather than a same-day catalyst: no reporting establishes that Huang said anything on July 14, and none is needed to explain a sector that was broadly bid.

| Stock / ETF | Price | Change | AAOI's margin |

|---|---|---|---|

| AAOI — Applied Optoelectronics | $124.46 | +11.24% | — [2] |

| LITE — Lumentum | $808.43 | +5.24% | +6.00 pts [7] |

| SOXX — iShares Semiconductor ETF | $571.14 | +3.17% | +8.07 pts [8] |

| FN — Fabrinet | $483.73 | +1.92% | +9.32 pts [7] |

| COHR — Coherent | $309.02 | +0.53% | +10.71 pts [7] |

Those are relative-performance facts, and the obvious next step — apportioning the move between "sector" and "stock-specific" — is where the available data runs out. Beta cannot do that job here. Scaling AOI's 3.69 five-year beta against SOXX's +3.17% yields about 11.7%, which is roughly the entire move, implying nothing stock-specific happened at all [3][8]. That number is a demonstration of the method's limits, not a finding: beta is a historical sensitivity estimate, and SOXX is neither the benchmark used in that regression nor a pure optics index. The defensible statement is the narrow one — AAOI outperformed the selected sector and peer references by roughly 6 to 11 percentage points at the stated snapshots, and no same-day data apportions that gap between the sector, the news and order flow.

Why it matters

The question worth asking is not whether a groundbreaking deserves 11%. It is what the reaction says about how this market prices AI infrastructure. Every fact about the project's scope, products, capacity and rationale was three months old — the milestone itself was new — and the market moved roughly a tenth of the company's value on it [4][6]. Two of the aggregators that covered the announcement made no reference to the April release at all [11][12]. Whatever else that is, it is not a market efficiently pricing new information.

The bear reading still has to contend with AOI's fundamentals, which are not the empty vessel a narrative-only story would need. AOI's broader capacity ramp is supported by substantial contracted demand: in March 2026 the company disclosed a 1.6T data-center transceiver order worth more than $200 million from a major hyperscale customer, and by April 2 it said 800G orders from a major hyperscale customer had reached $124 million since mid-March — together more than 70% of AOI's entire 2025 revenue of $456 million [10]. Those releases do not allocate the orders to the Pearland buildings specifically, so they establish demand for AOI's products rather than a return on this particular buildout. Trailing revenue is $507 million against a $43.34 million net loss, and operating cash flow is negative $208.87 million over the trailing twelve months [3]. But AOI is not cornered: it holds $439.71 million of cash against $280.42 million of debt — net cash of $159.28 million — with a current ratio of 3.83 [3]. The company has not said how the Pearland buildout will be financed. Share count is up 49.96% year over year, which establishes dilution as a live risk rather than a prediction about this project [3] — the dynamic we traced in Fermi's convertible-notes dilution, where financing rather than growth set the price. The valuation carries the same two-sidedness: 19.77x trailing sales looks extreme, but against analyst consensus revenue of $1.03 billion for 2026 and $2.57 billion for 2027 it is roughly 9.7x and 3.9x forward [3]. The trailing multiple and the forward multiple tell opposite stories, and which one is right is what August decides.

Why did Applied Optoelectronics (AAOI) stock jump on July 14, 2026?

AAOI rose about 11.24% to roughly $124.46 after announcing at 7:00 a.m. ET that it had begun construction on two adjacent Pearland, Texas properties, adding nearly 400,000 square feet of capacity for the 800G and 1.6T optical transceivers used in AI data centers [2][4]. The context most coverage omitted: AOI had announced this expansion on April 17, in a release naming the same buildings, the same products, the same AI rationale and a target of up to 700,000 units per month by the end of 2027 [6]. The principal new fact on July 14 was that construction had started; the release added no capital budget, completion date or revenue figure [4]. The wider optics complex was also higher, with the SOXX semiconductor ETF up 3.17% and Lumentum up 5.24%, so AAOI outperformed its sector and peers by roughly 6 to 11 points rather than moving in isolation [7][8].

AAOI analyst price targets: where the Street stands

Every rating action below predates the July 14 release; none is a response to it. Gaps are measured against the ~$124.46 afternoon snapshot.

| Firm | Action date / data accessed | Rating | Target | Gap to ~$124.46 |

|---|---|---|---|---|

| Rosenblatt Securities | Action: Jun 22, 2026 | Buy (reiterated) | $220 [13] | +76.8% |

| Raymond James | Action: Jun 10, 2026 | Outperform (maintained) | No target verified [13] | — |

| Weiss Ratings (quantitative rater) | Action: Jul 7, 2026 | Sell (D−, reiterated) | No target [13] | — |

| Wall Street Zen (quantitative rater) | Action: Apr 13, 2026 | Hold → Sell | No target [13] | — |

| Consensus — StockAnalysis (6 analysts) | Data as of Jun 21; accessed Jul 14 | Buy | $151.30; range $57.50–$220 [3] | +21.6% |

| Consensus — MarketBeat (6 analysts) | Accessed Jul 14 | Hold | $113.80; range $54–$220 [13] | −8.6% |

That last pair is the most useful fact in this section: the two major aggregators disagree on whether the Street rates AAOI a Buy or a Hold. Their averages are $37.50 apart — StockAnalysis's $151.30 is 33.0% higher than MarketBeat's $113.80 — with one implying 22% upside and the other 9% downside from the same price [3][13]. The gap reflects different contributor panels and refresh cadences rather than a market view, so any single "analyst price target" for AAOI deserves suspicion. Note also that StockAnalysis's forecast page carries data as of June 21, so reading it on July 14 does not make it a July 14 opinion. Both panels agree on a $220 high mark and both carry lows in the $54–$57.50 range — a spread of roughly 4x between the most and least optimistic contributors, which is itself the story.

The July 14 move in numbers

| Measure | Value | As of / source |

|---|---|---|

| AAOI price (afternoon) | ~$124.46 | +$12.58, ≈+11.24%; Jul 14, 2026, 2:57 p.m. ET — StockAnalysis [2] |

| Cross-check | $123.95 | ≈+10.79%; Jul 14, 2026 — Benzinga [12] |

| Cross-check | $124.87 | ≈+11.61%; Jul 14, 2026, ~2:30 p.m. ET — BestStocks change feed (FMP) [1] |

| Prior close, Mon Jul 13 | $111.88 | All three sources agree [1][2][12] |

| Intraday range | $117.70 – $128.35 | Session ongoing; Jul 14, 2:57 p.m. ET [2] |

| Volume (provisional) | 7,647,642 shares | ≈0.69x the ~11.02M 20-day average, with ~1 hour left to trade [2][3] |

| 52-week range | $18.50 – $233.67 | ~47% below the high; ~573% above the low [2] |

| 50-day moving average | $164.28 | Price sits ~24% below it [3] |

| Market cap | ~$9.99B | 80.24M shares outstanding × $124.46 [2][3] |

| Short interest | 10.76M shares | 14.11% of float, but a 0.74-day short ratio; latest reported [3] |

| Beta (5-year) | 3.69 | Historical regression statistic, not a same-day predictor [3] |

| Valuation | 19.77x trailing P/S | ≈9.7x 2026E and ≈3.9x 2027E consensus revenue [3][13] |

| Balance sheet | $159.28M net cash | $439.71M cash vs $280.42M debt; current ratio 3.83 [3] |

| TTM operating cash flow | −$208.87M | Net loss −$43.34M; shares +49.96% y/y [3] |

AAOI illustrative valuation scenarios

The scenarios below are the author's hypothetical, illustrative estimates — editorial weights anchored to cited Street targets and simple multiple arithmetic, not a DCF or a consensus model. The probabilities are subjective, and are shown to make the reasoning auditable rather than because they are precise.

| Scenario | Price | Prob. | Valuation basis | Key drivers |

|---|---|---|---|---|

| Bull | ~$200 | 25% | Target-anchored — below the $220 high mark both panels carry [3][13] | The 2026–27 consensus path ($1.03B then $2.57B of revenue) is validated by the August print; the $200M+ 1.6T and $53M+ 800G orders ship on schedule; the 700,000-unit end-2027 target stays credible and margins turn |

| Base | ~$133 | 45% | Consensus-anchored — the $132.55 midpoint of the two disputed aggregator averages, $113.80 and $151.30 [3][13] | Capacity arrives roughly on schedule and revenue compounds, but profitability stays out of reach and the funding mix stays unresolved against a 49.96% year-over-year share count increase |

| Bear | ~$78 | 30% | Multiple-based — ~12.3x trailing sales on $507M revenue and 80.24M shares, versus 19.77x today; still above both panels' $54–$57.50 lows [3][13] | The AI-optics bid fades and the sales multiple compresses toward the market's tolerance for an unprofitable supplier; the 2026–27 revenue ramp slips; the Q1 pattern of missing on both revenue and adjusted EPS repeats |

Probability-weighting those cases (0.25×$200 + 0.45×$132.55 + 0.30×$78) gives a probability-weighted scenario price — an illustrative midpoint, not a valuation-model output — of about $133, roughly 7% above the ~$124.46 snapshot. The blend is not especially sensitive to the weights: moving five percentage points from the bear case to the bull lifts it only to about $139. The width is what should stop the reader. The bull-bear spread runs from $78 to $200 — about 98% of the current price, against the roughly 41% spread we found on IBM the same morning. Two facts explain that width: the Street's own contributors are spread from $54 to $220, and the outcome turns on whether a 126% revenue increase in 2026 and a further 150% in 2027 actually lands [3][13]. Tuesday's release did nothing to narrow either.

Was this an AAOI story or an AI-optics story?

The available data do not permit a reliable causal split. What is observable: the optics complex was broadly higher against an established AI-optics narrative, and AAOI outperformed it by roughly 6 to 11 points depending on the benchmark [7][8]. What is not observable is why. Coherent, AOI's closest listed competitor, added only 0.53% [7] — an asymmetry worth noting, though not evidence against a fundamental reaction, since a market reading AOI's expansion as share gains would have no reason to bid a rival. The pattern does fit a group bouncing after being sold hard: Lumentum was down about 16.6% over the prior month even after Tuesday's gain [9], and AAOI remains ~24% below its own 50-day average [3]. Compare the cleaner sector-wide moves we documented in Ultra Clean's WFE rally and Arista's AI-switching re-rating.

What would prove this reading wrong

Each reading below is falsifiable. These are the observations that would undermine them.

| Interpretation | What would weaken it |

|---|---|

| Little new information — April 17 disclosed the substance | AOI follows up with a capital budget, completion date or contracted capacity materially larger than April implied. The groundbreaking would then have signalled scale that the market read correctly before the details arrived |

| Participation was light — the 0.69x reading | The session closes at or above the ~11.02M average, or the gain extends over the following week on rising turnover. This is explicitly provisional: an hour of trading remained [2] |

| Positioning may have amplified it — 14.11% short float | The 0.74-day short ratio already cuts against a forced squeeze. A material decline in short interest over a reporting period encompassing July 14 would be consistent with covering — though unchanged settlement data would not rule it out, since a snapshot can miss intraperiod covering and re-shorting [3] |

| Funding is a live risk — negative operating cash flow | August shows the cash burn narrowing, or AOI funds Pearland from its $439.71M cash position, customer prepayments or non-dilutive financing without returning to equity markets [3] |

What AAOI investors should watch next

First, the second-quarter report, currently estimated for around August 6 — a date StockAnalysis labels an estimate rather than a company-confirmed one [3]. It is the next hard information, and where the Q1 pattern of missing on both revenue ($151.14M against $156.98M expected) and adjusted (non-GAAP) EPS (−$0.07 against −$0.05) either repeats or breaks [13]. Second, the numbers still missing: a capital budget and completion date for Pearland, and whether the end-2027 target of 700,000 units per month remains on track [4][6]. Third, the funding mix — AOI has $159.28 million of net cash and has not said how it will pay for the buildout, so the financing decision may matter more to the share price than the capacity itself [3]. Fourth, whether the $200M+ 1.6T order ships on its expected second-half schedule, which is the cleanest test of whether the capacity has demand behind it [10]. Fifth, the peer complex: if Coherent and Lumentum re-rate in the coming sessions, the sector reading strengthens. Finally, the $164.28 50-day average — a widely watched technical reference about 32% above Tuesday's snapshot; a sustained move above it would improve the technical picture, though no single average settles a trend [3]. For the other side of the AI-infrastructure trade, see our SanDisk memory-selloff analysis; more market-mover breakdowns are in the BestStocks research hub.

Applied Optoelectronics (AAOI) stock-jump FAQ

Why did AAOI stock jump on July 14, 2026?

Applied Optoelectronics rose about 11.24% to roughly $124.46 after announcing before the open that it had begun construction on two adjacent Pearland, Texas properties, adding nearly 400,000 square feet of capacity for the 800G and 1.6T optical transceivers used in AI data centers. The wider optics complex was also higher — the SOXX semiconductor ETF gained 3.17% and Lumentum 5.24% — so AAOI outperformed its sector and peers by roughly 6 to 11 percentage points depending on the benchmark rather than moving in isolation.

Was the Pearland expansion actually new news?

Mostly not. AOI announced this expansion on April 17, 2026, in a release headlined "AOI Expands Its Houston-Area Footprint to 900,000 Square Feet." That release named the same two buildings, the same ~388,000 square feet, the same 800G and 1.6T products, the same AI-data-center rationale, and a target of up to 700,000 units per month by the end of 2027. CFO Stefan Murry said at the time that the expansion was "aligned with the 2027 capacity targets we outlined on our most recent earnings call." The properties themselves had been disclosed even earlier, in an 8-K covering an April 7 purchase agreement. The principal new fact on July 14 was that construction had started — a real execution milestone, but one that added no capital budget, completion date or new capacity figure.

Was the AAOI move driven by short covering?

The data cannot establish that, and one figure argues against it. Short interest is high at 10.76 million shares, or 14.11% of float, which is the sort of number that invites a squeeze narrative. But the short ratio is just 0.74 days to cover, because average daily turnover is large relative to the position, which makes a forced, self-reinforcing squeeze less likely (though days-to-cover uses historical average volume and does not guarantee a position could be closed that fast in stressed trading). Volume was also running at about 0.69x the 20-day average with an hour left to trade, though that is provisional. Elevated short interest may have amplified the move, but no same-day data distinguishes covering from new long buying or other order flow, and covering is itself a form of buying.

Is AAOI in a short-term drawdown or a longer-term rally?

In a drawdown, despite the day's jump. At $124.46 the stock traded about 24% below its own 50-day moving average of $164.28 and roughly 47% below its 52-week high of $233.67. It remains up sharply on longer horizons — StockAnalysis reports a 337.5% 52-week change against a 52-week low of $18.50 — but July 14 was a bounce inside a deep pullback rather than a breakout to new highs. Peer Lumentum showed the same pattern, down about 16.6% over the prior month even after gaining 5.24% that day.

What are the analyst price targets for AAOI?

There is no reliable single figure, which is itself worth knowing. The two major aggregators disagree: StockAnalysis reports a Buy consensus with a $151.30 average target across six analysts, while MarketBeat reports a Hold consensus with a $113.80 average across six — a 33% gap, one implying 22% upside and the other 9% downside from the same price. Both agree on a $220 high mark, from Rosenblatt Securities on June 22, 2026, and both carry lows in the $54 to $57.50 range. Note also that StockAnalysis's forecast data carries an as-of date of June 21, so reading it on July 14 does not make it a July 14 view, and every published action predates the Pearland groundbreaking.

Can AOI afford to build the Pearland expansion?

It has more room than the cash-burn figure alone suggests. Operating cash flow is negative $208.87 million over the trailing twelve months and share count is up 49.96% year over year, so dilution is a live risk. But AOI holds $439.71 million of cash against $280.42 million of debt — net cash of $159.28 million — with a current ratio of 3.83. The company has not disclosed how it will finance the buildout, so the funding mix is an open question rather than a settled problem. There is also real contracted demand behind the capacity: AOI booked a 1.6T order worth more than $200 million from a major hyperscale customer in March 2026, and said 800G orders from a major hyperscale customer had reached $124 million since mid-March.