Stock Analysis

Why Did PayPal (PYPL) Stock Jump ~17% on July 15, 2026?

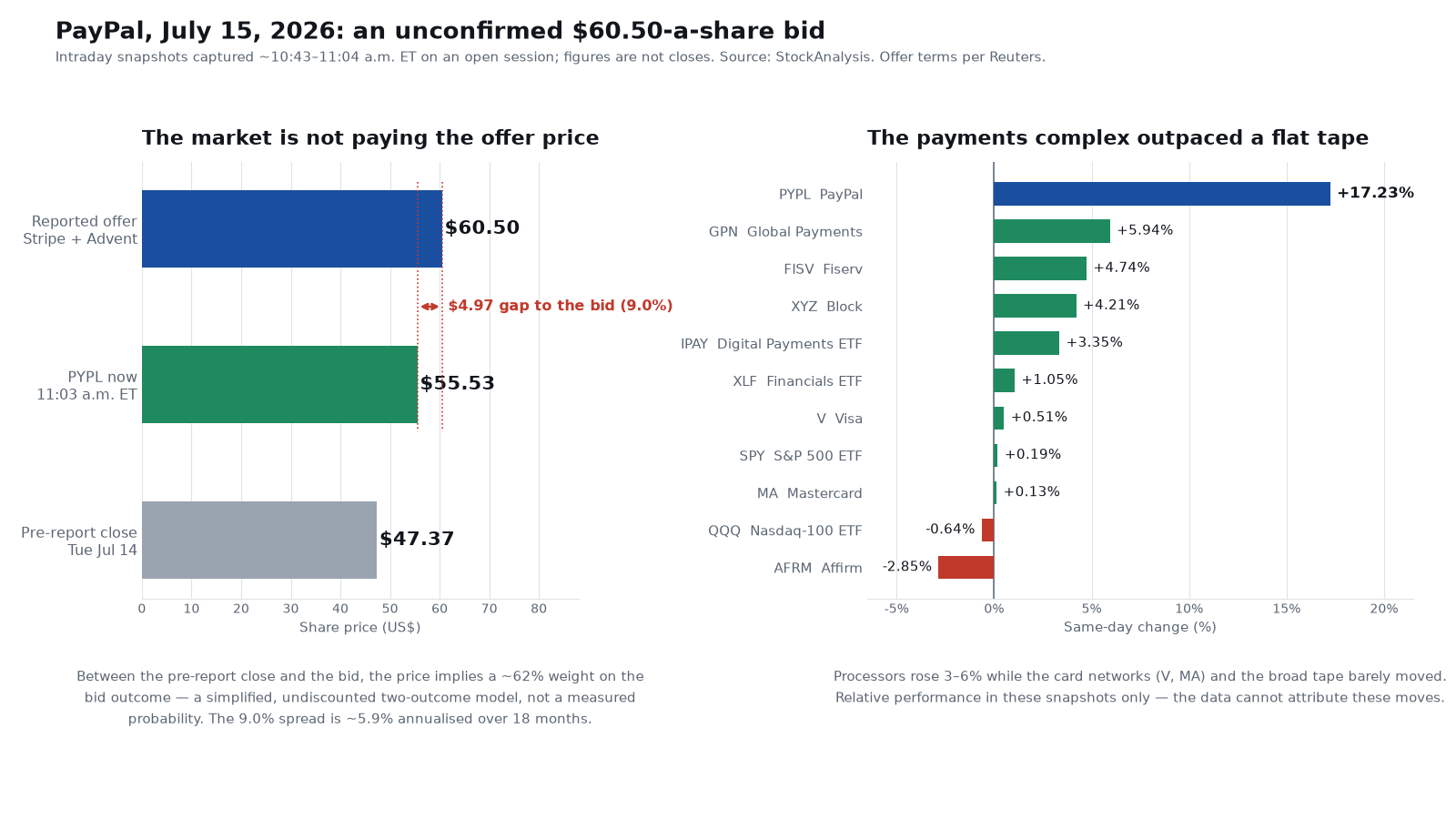

PayPal rose about 17% to roughly $55.53 on July 15 after Reuters reported that Stripe and Advent International had jointly offered $60.50 a share — more than $53 billion — to take it private. Nothing is confirmed: all three parties declined to comment and the board has not responded. The stock still traded 8.95% below the reported bid, worth only about 5.9% annualised over an 18-month close — and every consensus target average sits below the offer.

Summary

PayPal (NASDAQ: PYPL) rose about 17.23% to roughly $55.53 on Wednesday, July 15, 2026 — up $8.16 from Tuesday's $47.37 close — as of 11:03 a.m. ET, with the session still open [2]. The trigger was a Reuters exclusive, published after Tuesday's close, reporting that Stripe and the private-equity firm Advent International have jointly offered $60.50 a share — more than $53 billion — to acquire PayPal outright, backed by roughly $50 billion of committed bank financing, with the two splitting ownership evenly [4][5]. Here is the detail that should govern how the day is read: none of it is confirmed. PayPal, Stripe and Advent all declined to comment; PayPal has issued no statement and its board has not responded [4][5]. A seventeen-percent move in a $49 billion company is resting entirely on reporting attributed to unnamed sources.

And the market plainly knows it. At $55.53 the stock sits $4.97, or about 9%, below the $60.50 bid [2]. Investors are not paying the offer price, because the offer might never become one. In one sentence: this was not a takeover, it was a report of one — and the gap between the price and the bid is where the market's doubt is stored. The rest of this piece measures that doubt.

What changed

Separating what is reported from what is established matters more here than in an ordinary mover, so the table below sorts the day's claims by how well they are evidenced.

| Claim | Status | Detail |

|---|---|---|

| Price and volume | Observed | $55.53, +17.23%, on 50.2M shares by 11:03 a.m. ET — verified across two independent feeds [2][14] |

| The offer terms | Reported, not confirmed | $60.50 a share, more than $53bn, ~$50bn of committed bank financing, Stripe and Advent owning the company 50-50, no plan to break it up — Reuters, citing sources [4][5] |

| The approach's history | Reported, not confirmed | The July offer reportedly followed an initial approach in early April; the bidders are said to want to advance talks over the next several weeks [4][5] |

| PayPal's response | None | PayPal has not responded to the offer. All three parties declined to comment [4][5] |

| A board meeting | Weakly sourced | Search summaries report CNBC saying the board could meet as soon as July 20. We could not retrieve the underlying text, and the Reuters wire we did read does not carry that date. Treat it as unverified [5] |

| Regulatory outcome | Unknown | No filing has been made and no review has begun, because there is no agreed deal to review |

| Our own change-detection page | Not used | BestStocks' PYPL page rendered Tuesday's $47.37 close as though it were a live price, beside Wednesday's real $54.92 intraday high. No figure in this article is taken from it; the prices here come from independent feeds [1] |

The reported terms are at least internally consistent with the tape. PayPal's market capitalisation of $48.98 billion at $55.53 implies about 882 million shares — close to the 882.11 million StockAnalysis lists as outstanding — and at $60.50 those shares are worth roughly $53.4 billion, matching the reported "more than $53 billion" [2]. The premium reconciles too: $60.50 against Tuesday's $47.37 close is +27.7%, the "roughly 28%" the reporting describes [2][4]. Be careful what that establishes. It shows only that the reported per-share price and the reported equity value are mutually consistent — a mistaken or invented figure could multiply correctly too. It authenticates neither the sources nor the offer.

One number frames why a bid exists at all, and it needs stating precisely. PayPal's trailing earnings per share are about $5.34, so at Tuesday's $47.37 close — the price the bidders were looking at — the company traded at roughly 8.9x earnings [2][15]. That is the multiple that invites a bid. After Wednesday's jump the stock trades at about 10.4x, and at $60.50 the bidders would be paying roughly 11.3x trailing earnings [2][15]. Even at the bid this is a profitable company on a modest multiple, about 24% below its own 52-week high of $79.50, after years of share loss to Apple Pay, Google Pay and rival checkout providers — including Stripe itself [2][4][11]. That is the logic of the approach: not a growth story, a value one.

How the move compares

PayPal did not move alone, and what moved with it is the most analytically useful fact of the session.

| Stock / ETF | Price | Change | As of |

|---|---|---|---|

| PYPL — PayPal | $55.53 | +17.23% | 11:03 a.m. [2] |

| GPN — Global Payments | $80.40 | +5.94% | 11:00 a.m. [10] |

| FISV — Fiserv | $51.89 | +4.74% | 11:02 a.m. [10] |

| XYZ — Block | $83.36 | +4.21% | 11:02 a.m. [10] |

| IPAY — Amplify Digital Payments ETF | $50.00 | +3.35% | 10:43 a.m. [12] |

| XLF — Financial Select Sector SPDR | $56.77 | +1.05% | 11:04 a.m. [12] |

| V — Visa | $357.82 | +0.51% | 11:02 a.m. [10] |

| SPY — S&P 500 ETF | $753.27 | +0.19% | 11:03 a.m. [12] |

| MA — Mastercard | $538.73 | +0.13% | 11:03 a.m. [10] |

| QQQ — Invesco Nasdaq-100 ETF | $715.11 | −0.64% | 11:04 a.m. [12] |

| AFRM — Affirm | $82.05 | −2.85% | 11:02 a.m. [10] |

Read the middle of that table rather than the top. The broad tape was flat — the S&P 500 proxy up 0.19%, the Nasdaq-100 proxy actually down 0.64% [12]. Yet Global Payments rose 5.94%, Fiserv 4.74% and Block 4.21%, and the digital-payments ETF gained 3.35% [10][12]. Meanwhile Visa added 0.51% and Mastercard 0.13% — close to the broad-market move in this snapshot [10].

One explanation fits that split, and it is worth being clear about how weakly it is established. The candidate reading: a $53 billion bid for a processor trading at roughly 8.9x earnings prompts the market to mark up the takeout option in comparable names, while the card networks — far larger, and on a different business model — are not obvious candidates for the same treatment. But a single morning's cross-section cannot separate that from at least four other explanations: each company's own newsflow, factor or short-covering flows, general payments-sector positioning, and ordinary intraday volatility. Fiserv is the clearest warning here, carrying substantial independent news of its own [13]. So the defensible statement is only the descriptive one: the payments complex outperformed a flat tape by three to six points in these snapshots while the networks did not. Whether that is takeout probability being re-priced is a hypothesis the day's data cannot test. Affirm's −2.85% is at least a check on the enthusiasm: buy-now-pay-later did not participate [10].

Why it matters

The most striking fact in this story is not the premium. It is that every consensus average we checked sits below the bid — and two of the three sit below the current price. Consensus is $51.38 across 44 analysts on one aggregator, $53.91 across 45 on another, and $47.14 on a third [3][9][14]. Goldman Sachs raised its target to $48 on July 9 while keeping a Sell rating [9]. On Wednesday, responding to the report itself, TD Cowen reiterated Hold with a $48 target and Mizuho reiterated Neutral at $50 [7][8]. None of those reaches $60.50.

That is a claim about averages and about the recent, dated actions — not about every analyst. The panels carry high marks well above the bid: MarketBeat shows a $100 top target and StockAnalysis a $147.39 top against a $32 low, so the individual range is enormous and some of those marks are likely stale or drawn from different contributor sets [3][9]. The useful version is narrower and still striking: the central Street estimate of standalone PayPal clusters in the high-$40s to low-$50s, while a private-equity firm and a private competitor with $50 billion of committed debt have reportedly put $60.50 on it [3][9]. Both can be true — a buyer with control can do things a public-market minority holder cannot, from cutting costs without quarterly scrutiny to merging Stripe's merchant checkout with PayPal's consumer wallet franchise [11]. And the $55.53 price is not a verdict on one or the other: it embeds the standalone business, the odds of rejection or a bump, financing and regulatory risk, and time value, all at once.

That is what makes the antitrust question the whole investment case rather than a footnote. Commentary cited in the reporting holds that a combined Stripe-PayPal would process on the order of $4 trillion in annual payment volume, with BTIG noting PayPal alone touches roughly a quarter of global e-commerce transactions — figures that are analyst characterisations rather than verified disclosures, and should be read as such [6][13]. Reviewers in Washington and Brussels would be asked to approve a combination of the largest online checkout button and one of the largest payment processors, and the remedies floated in early commentary — divesting Venmo or Braintree — would strip out exactly the assets that make the target attractive [13]. We saw a milder version of this dynamic when Circle's national trust-bank approval re-rated the stock on a regulator's signature alone, and the reverse in Roku's reaction to the Fox acquisition, where the market had to price a deal's strategic logic before any of it was certain. For scale, the reporting notes the closest recent comparable is Global Payments' 2025 purchase of Worldpay at $24.25 billion — less than half this size [4].

Why did PayPal (PYPL) stock jump on July 15, 2026?

PayPal rose about 17.23% to roughly $55.53 by 11:03 a.m. ET after Reuters reported, citing unnamed sources, that Stripe and Advent International had jointly offered $60.50 a share — more than $53 billion — to take the company private, supported by about $50 billion of committed bank financing [2][4]. The offer represents roughly a 28% premium to Tuesday's $47.37 close [2][4]. Crucially, nothing has been confirmed: PayPal, Stripe and Advent all declined to comment, PayPal's board has not responded, and no filing or company statement exists [4][5]. The stock traded about 9% below the reported bid, indicating the market prices meaningful doubt that the deal completes [2]. The wider payments complex rose with it — Global Payments +5.94%, Fiserv +4.74%, Block +4.21% — against a flat market, while Visa and Mastercard barely moved [10][12].

PayPal analyst price targets: the Street is below the bid

The two July 15 entries are direct responses to the takeover report; the rest predate it. Gaps are measured against the ~$55.53 snapshot.

| Firm | Action date | Rating | Target | Gap to ~$55.53 |

|---|---|---|---|---|

| Mizuho | Jul 15, 2026 — on the report | Neutral (reiterated) | $50 [7] | −10.0% |

| TD Cowen | Jul 15, 2026 — on the report | Hold (reiterated) | $48 [8] | −13.6% |

| Goldman Sachs | Jul 9, 2026 | Sell | $41 → $48 [9] | −13.6% |

| Bank of America | May 6, 2026 | Neutral | $55 → $53 [9] | −4.6% |

| BTIG | Undated July commentary | Neutral | No target [6] | — |

| Freedom Broker | Undated July commentary | Buy | $60 [6] | +8.1% |

| Consensus — StockAnalysis (44 analysts) | Accessed Jul 15 | Hold | $51.38 [3] | −7.5% |

| Consensus — MarketBeat (45 analysts) | Accessed Jul 15 | Hold | $53.91; 6 Sell / 32 Hold / 7 Buy [9] | −2.9% |

Three observations. First, every target listed above is below the $60.50 offer, and all but one is below the current price — the highest, Freedom Broker's $60, still does not reach the bid [3][6][9]. Second — and this is the necessary caveat — that is not true of every target in existence. The panels carry high marks far above the bid: $100 on MarketBeat and $147.39 on StockAnalysis, against a $32 low [3][9]. Some are plausibly stale or from a different contributor universe, but they exist, so the defensible claim is about the averages and the recent dated actions, not the whole Street. Third, the aggregators disagree by $2.53 on the average ($51.38 against $53.91) while agreeing on the Hold rating — a much narrower conflict than we found on AAOI, where the same two panels disagreed by 33% and on the rating itself [3][9]. Note too that a target published before a takeover report is not an opinion about the takeover: Goldman's $48 Sell is a view on the business, not a prediction that the bid fails.

The July 15 move in numbers

| Measure | Value | As of / source |

|---|---|---|

| PYPL price (late morning) | ~$55.53 | +$8.16, ≈+17.23%; Jul 15, 2026, 11:03 a.m. EDT — StockAnalysis [2] |

| Cross-check | $55.47 | ≈+17.10%; Jul 15, 2026, ~11:05 a.m. ET — Finviz [14] |

| Cross-check | $55.22 | Jul 15, 2026 — Investing.com [6] |

| Prior close, Tue Jul 14 | $47.37 | The pre-report close — the Reuters story broke after it. Not necessarily a clean no-deal price: an approach was reportedly made in early April [2][4] |

| Reported offer | $60.50 | >$53bn; ~28% premium to the $47.37 close; ~$50bn committed financing — Reuters [4] |

| Gap to the offer | −$4.97 (−8.95%) | The market is not paying the bid. Worth ~5.9% annualised over an 18-month close, ~4.4% over 24 months, before dividends [2][4] |

| Binary-model weight on the bid outcome | ~62% | Derived: $8.16 ÷ $13.13. NOT a probability of completion — an undiscounted two-outcome weight that assumes a break returns the stock to $47.37 and ignores time value [2][4] |

| Open / day's range | $54.85 / $53.44 – $55.54 | Session ongoing; Jul 15, 11:03 a.m. ET [2] |

| Volume | 50,205,991 shares | ≈2.87x the ~17.46M 20-day average, with ~76% of the session still to run — a floor, not a final figure [2][3] |

| 52-week range | $38.46 – $79.50 | ~30% below the high even after the jump [2] |

| Market cap | ~$48.98B | ≈882M shares × $55.53; at $60.50 ≈ $53.4B, matching the reported figure [2] |

| Valuation | ~10.4x trailing earnings | $55.53 ÷ ~$5.34 TTM EPS. ≈8.9x at Tuesday's $47.37 close and ≈11.3x at the $60.50 bid. NOTE: the vendor's displayed 8.87 P/E was computed off the prior close, not the live price [2][15] |

| Company confirmation | None | PayPal, Stripe and Advent all declined to comment; no board response [4][5] |

PayPal illustrative valuation scenarios

The scenarios below are the author's hypothetical, illustrative estimates — editorial weights anchored to the reported bid, cited Street targets and the verified pre-report close, not a DCF or a consensus model. The probabilities are subjective, and are shown to make the reasoning auditable rather than because they are precise.

| Scenario | Price | Prob. | Valuation basis | Key drivers |

|---|---|---|---|---|

| Bull | ~$64 | 15% | Above the reported bid — assumes competitive tension [4] | The board rejects $60.50 as opportunistic given the stock traded near $79.50 within the year; Stripe and Advent raise, or a third party (a large processor or another sponsor) is drawn in by a public price tag. The $50bn financing commitment signals the bidders' seriousness [2][4] |

| Base | ~$60.50 | 50% | The reported offer price [4] | The board engages, the deal is agreed at or near $60.50, and it survives an 18–24 month review — possibly with remedies. Shareholders receive the bid; the wait is the cost [13] |

| Bear | ~$48 | 35% | The pre-report close ($47.37), which is also where Goldman's and TD Cowen's targets independently land [2][8][9] | The talks fail, the board refuses to engage, or antitrust reviewers block it or demand Venmo/Braintree divestitures that break the economics. The stock returns to its standalone valuation, which the Street marks at $48–54 [3][13] |

Probability-weighting those cases (0.15×$64 + 0.50×$60.50 + 0.35×$48) gives a probability-weighted scenario price — an illustrative midpoint, not a valuation-model output — of about $56.65, roughly 2% above the ~$55.53 snapshot. Two caveats belong with it. First, shifting five percentage points from the base case to the bear case moves the blend only to about $56.03. That is a narrow test, not a general result: a lower bear price, a longer close, or dropping the $64 case would move the answer materially, so it shows these particular outcomes are bunched, not that the weights are unimportant. Second, these weights imply a 65% chance of a completed deal against the 62% weight implied by the spread — but the two are not measuring the same thing and should not be reconciled. The 65% is a subjective view across two success outcomes including a $64 bump; the 62% comes from an undiscounted equation permitting only $60.50 or $47.37. Neither carries time value or dividends. The three-point difference is a difference of construction, not a precise disagreement [2][4].

The width is the other story. The bull-bear spread runs $48 to $64 — about 29% of the current price, against the roughly 98% spread we found on AAOI the previous day. A reported price to anchor to compresses the distribution in a way a growth story never does — though "anchor" is the right word, not "strike": with no definitive agreement, the bid can still be rejected, raised, negotiated down or displaced, which is exactly what the $64 case represents.

Was this a PayPal story or a payments story?

Overwhelmingly PayPal's — but not exclusively. The stock's 17.23% dwarfed everything around it, and the catalyst names the company explicitly, so no sector explanation is needed for the bulk of the move [2][4]. The interesting residue is the 3-to-6-point gain across Global Payments, Fiserv and Block against a flat tape [10][12]. The natural reading is a takeout-probability re-rating: if a $53 billion bid can land on a processor that closed Tuesday at roughly 8.9x earnings, the market marks up the option value in every comparable name. The available data cannot confirm that — this is one morning's relative performance, and each of those companies has its own newsflow, Fiserv conspicuously so after a year of executive turnover and reported interest in its debit-network assets [13]. But the pattern's shape is informative: the names that re-rated are the plausible targets, and the names that did not — Visa, Mastercard — are far larger and much less obvious candidates for the same treatment [10]. Contrast the cleaner, genuinely sector-wide moves we documented in SanDisk's memory selloff, where a supplier's warning dragged an entire complex down together.

What would prove this reading wrong

Each reading below is falsifiable. These are the observations that would undermine them.

| Interpretation | What would weaken it |

|---|---|

| Nothing is confirmed — the move rests on sourced reporting | PayPal files an 8-K, issues a statement, or the board publicly responds. Confirmation would not change the terms, but it would remove the reporting risk that part of the 9% spread compensates for |

| The spread implies a ~62% weight on the bid outcome | The arithmetic assumes a break returns the stock to $47.37 and ignores time value. If a failed bid leaves PayPal in play, the downside is higher and the implied probability lower; if a failure marks it as unwanted, the reverse. The estimate is a range, not a reading |

| Conviction was real — 2.87x average volume | Little would: the ratio can only rise from here, and it was measured with three-quarters of the session left [2][3]. But heavy volume identifies neither the buyers nor their reasons, and a contested arbitrage generates exactly this pattern |

| Peers re-rated on takeout odds — the 3–6% cluster | The gains fade within days as the read-across is faded, or company-specific news accounts for them. A single morning cannot separate a takeout-option re-rating from coincident newsflow [10] |

| The Street values PayPal at $48–54 | A wave of post-report target increases on the standalone business — as opposed to deal-driven ones — would show analysts had been too bearish rather than that the bid is rich [3][9] |

What PayPal investors should watch next

First, any confirmation at all — a company statement, an 8-K, or a board response. This is the single most important unknown, and as of this snapshot none of it existed [4][5]. Second, the spread itself, which is now a live probability gauge: if PayPal converges toward $60.50 the market is growing confident, and if it drifts back toward $47.37 the bid is being faded — a cleaner real-time signal than any commentary [2][4]. Third, whether a rival bidder emerges, the only realistic route above $60.50. Fourth, antitrust signalling from Washington and Brussels, and specifically whether remedies touch Venmo or Braintree — the assets whose divestiture would most change the arithmetic [13]. Fifth, PayPal's next earnings report, which matters more than usual: it sets the standalone value that the bear case reverts to, and a strong print strengthens the board's hand to say no. Sixth, the peer complex — if Global Payments and Block hold their gains, the takeout-re-rating reading strengthens; if they round-trip, it was noise [10]. For a comparable corporate-action reaction, see our analysis of Roku and the Fox acquisition and of Middleby's Midera spin-off; more market-mover breakdowns are in the BestStocks research hub.

PayPal (PYPL) takeover-offer FAQ

Why did PayPal stock jump on July 15, 2026?

PayPal rose about 17.23% to roughly $55.53 by 11:03 a.m. ET after Reuters reported, citing unnamed sources, that Stripe and the private-equity firm Advent International had jointly offered $60.50 a share — more than $53 billion — to take PayPal private, backed by about $50 billion of committed bank financing, with the two firms splitting ownership evenly. That is roughly a 28% premium to Tuesday's $47.37 close. The report broke after Tuesday's close, which is why the stock gapped up on Wednesday morning.

Has PayPal confirmed the Stripe and Advent takeover offer?

No. This is the most important qualification in the story. PayPal, Stripe and Advent International all declined to comment, PayPal's board has not responded to the offer, and there is no company statement or filing confirming any of it. Every term — the $60.50 price, the $53 billion value, the $50 billion of financing, the 50-50 ownership split — comes from reporting attributed to unnamed sources. Search summaries reported CNBC saying the board could meet as soon as July 20, but we could not retrieve the underlying text and the Reuters wire we did read does not carry that date, so we do not present it as established.

Why is PayPal stock trading below the $60.50 offer price?

Because the market is not certain the deal will happen. At $55.53 the stock sits $4.97, or about 9%, below the reported bid. The plainest way to read that gap is as a return: it is worth roughly 5.9% annualised if the deal closes in 18 months, or 4.4% over 24 months, before dividends — thin compensation for antitrust risk. You can also invert it into a weight: if you assume a failed deal returns the stock to its $47.37 pre-report close, then paying $55.53 for a shot at $60.50 implies a ~62% weight on the bid outcome. That is the weight that balances a simplified, undiscounted two-outcome equation, not a measured probability of completion — it ignores the present value of $60.50, dividends, the risk premium on tied-up capital, a negotiated or rival price, and the chance that a failed bid leaves PayPal in play rather than back at $47.37. The doubt it reflects is real: nothing is confirmed, the board has not engaged, and cited commentary puts a multi-jurisdiction antitrust review at 18 to 24 months.

What do analysts think PayPal is worth?

Less than the bid — which is the striking part. Consensus is a Hold at $51.38 across 44 analysts on StockAnalysis and $53.91 across 45 on MarketBeat, while Finviz carries $47.14. Every one of those averages sits below the $60.50 offer and at or below the current price. Goldman Sachs raised its target to $48 on July 9 but kept a Sell rating. Responding to the takeover report itself on July 15, TD Cowen reiterated Hold at $48 and Mizuho reiterated Neutral at $50. So the central Street estimate of standalone PayPal clusters in the high-$40s to low-$50s. Note this is a claim about the averages and the recent dated actions, not about every analyst: the panels carry high marks of $100 and $147.39 against a $32 low, some of which are likely stale. And the $55.53 price is not a verdict on the business or the deal alone — it embeds both at once, along with financing risk, regulatory risk and time value.

Did other payment stocks move on the PayPal news?

Yes, and the pattern is informative. Against a flat tape — the S&P 500 proxy up 0.19% and the Nasdaq-100 proxy down 0.64% — Global Payments rose 5.94%, Fiserv 4.74% and Block 4.21%, and the IPAY digital-payments ETF gained 3.35%. But Visa added just 0.51% and Mastercard 0.13%. The natural reading is that a $53 billion bid for a processor that closed Tuesday at roughly 8.9x earnings lifted the perceived takeout option across comparable processors, while the card networks are neither plausible buyout targets nor obviously affected. That is an inference from one morning's relative performance, though, not a demonstrated causal link — each of those companies has its own newsflow, Fiserv especially.

Was the PayPal move driven by real buying or a thin squeeze?

The volume was unambiguously real. By 11:03 a.m. ET PayPal had traded 50,205,991 shares against a 20-day average of 17,463,448 — about 2.87 times a normal full day's turnover with roughly three-quarters of the session still to run, so that ratio can only rise. What that establishes is narrow: the move was not thinly traded. It does not establish who was responsible — market makers, options hedgers, merger-arbitrage funds, retail and high-frequency firms all leave the same footprint — and it certainly does not make the move something other than headline-driven, since the Reuters report is plainly what caused it.

What is the biggest risk to the PayPal deal?

Antitrust, by some distance. Stripe and PayPal are two of the largest players in online payments, and commentary cited in the reporting suggests a combined entity would process on the order of $4 trillion a year, with PayPal alone touching roughly a quarter of global e-commerce transactions — analyst characterisations rather than audited figures. Reviewers in the United States and the European Union would be asked to approve a combination of the largest online checkout button with one of the largest processors, and the remedies floated in early commentary, such as divesting Venmo or Braintree, would remove exactly the assets that make PayPal attractive. Beyond that sits the simpler risk that PayPal's board declines to engage at $60.50 — a price still about 24% below the stock's own 52-week high of $79.50.